End-to-End Digital Lending Solutions: LOS, LMS & KYC API Explained

The digital lending revolution in India is transforming how NBFCs, fintech companies, and financial institutions operate. Traditional lending processes that once took days or even weeks are now being completed in minutes—thanks to end-to-end digital lending solutions.

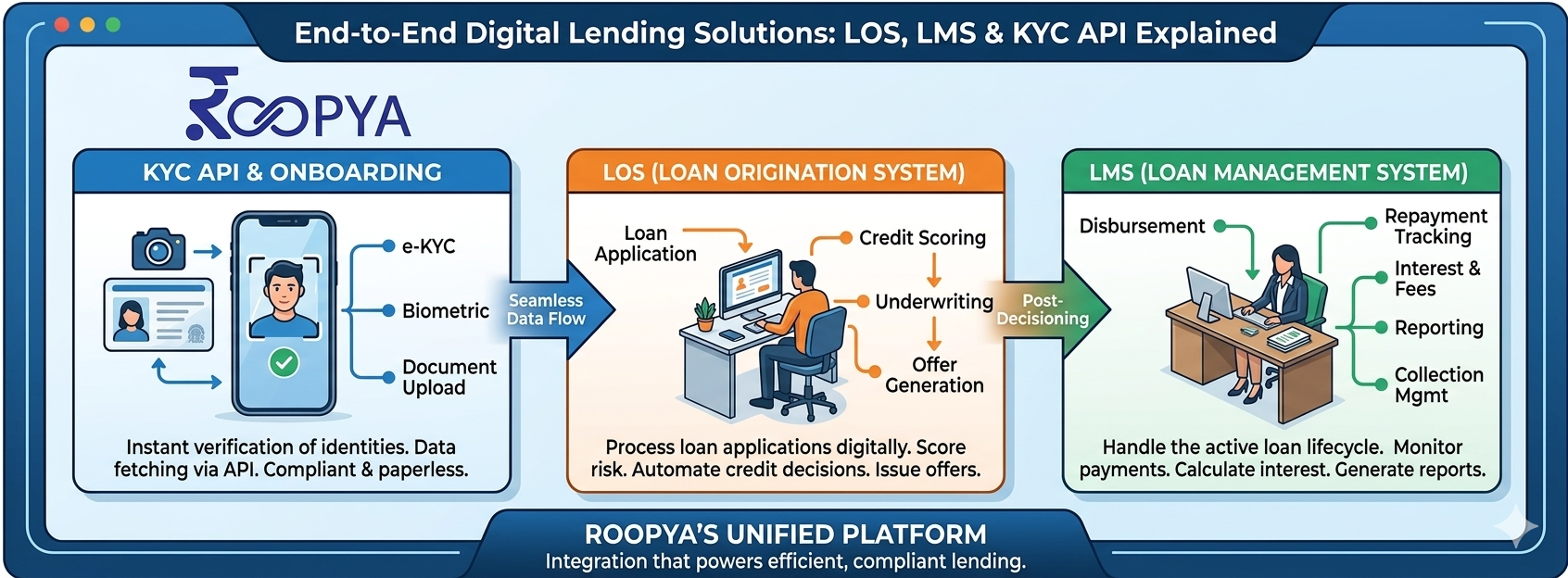

These modern systems combine three powerful components:

- Loan Origination System (LOS)

- Loan Management System (LMS)

- KYC API & Verification Infrastructure

Together, they create a fully automated lending ecosystem—from borrower onboarding to loan closure.

In this guide, we’ll break down how these systems work, why they matter, and how platforms like Roopya are helping lenders scale faster.

Start Free Trial

What is End-to-End Digital Lending Software?

End-to-end digital lending software is a complete technology platform that automates the entire loan lifecycle—from application and verification to disbursement and repayment.

Instead of relying on manual paperwork and disconnected systems, modern lending platforms integrate:

- Customer onboarding

- Digital KYC

- Credit assessment

- Loan approval & disbursement

- EMI tracking & collections

This unified approach helps lenders:

✅ Reduce turnaround time (TAT)

✅ Improve approval accuracy

✅ Ensure RBI compliance

✅ Scale operations efficiently

Key Components of Digital Lending Solutions

1. Loan Origination System (LOS) – The Entry Point

A Loan Origination System (LOS) is the first step in the lending journey. It handles everything from application submission to loan approval and disbursement.

Core Functions of LOS:

- Loan application intake (web/app/API)

- Aadhaar & PAN-based KYC verification

- Credit bureau checks (CIBIL, Experian, etc.)

- Income assessment & risk scoring

- Automated underwriting

- Loan approval workflows

- Digital agreement & eSign

- Loan disbursement

A well-designed LOS can reduce loan approval time from days to under 10 minutes for standard profiles.

Why LOS is Important:

- Faster loan approvals

- Reduced human errors

- Improved customer experience

- Better credit risk management

2. Loan Management System (LMS) – The Backbone

Once a loan is disbursed, the Loan Management System (LMS) takes over. It manages the loan throughout its lifecycle until closure.

Core Functions of LMS:

- EMI schedule generation

- Payment collection (UPI, NACH, NEFT)

- Interest calculation & ledger management

- Overdue tracking & NPA classification

- Loan restructuring & foreclosure

- Collections & recovery management

- Regulatory reporting

The LMS ensures financial accuracy and portfolio health, making it the backbone of any lending business.

Why LMS is Critical:

- Improves collection efficiency

- Reduces default risk

- Provides real-time portfolio insights

- Ensures compliance with RBI norms

3. KYC API – The Compliance Engine

KYC (Know Your Customer) APIs are essential for verifying borrower identity and preventing fraud.

Types of KYC APIs:

- Aadhaar OTP eKYC

- PAN verification

- CKYC lookup

- DigiLocker-based KYC

- Video KYC

- Face match & liveness detection

These APIs ensure that lenders comply with RBI regulations and PMLA guidelines while onboarding customers.

Why KYC API Matters:

- Prevents fraud & identity theft

- Enables instant onboarding

- Reduces manual verification costs

- Ensures regulatory compliance

How LOS, LMS & KYC APIs Work Together

In a modern digital lending platform, these systems are not separate—they are fully integrated.

Step-by-Step Lending Flow:

1. Application Stage (LOS)

- Borrower applies via mobile/web

- Basic details captured

2. KYC & Verification

- Aadhaar & PAN verification via API

- Fraud checks & device intelligence

3. Credit Decisioning (LOS)

- Credit bureau data fetched

- AI-based risk scoring

- Loan approval/rejection

4. Disbursement

- Loan agreement signed digitally

- Funds transferred instantly

5. Loan Servicing (LMS)

- EMI schedule created

- Payments tracked

6. Collections & Closure (LMS)

- Reminders & recovery workflows

- Loan closure & NOC generation

APIs act as the connective layer, ensuring all systems communicate seamlessly and operate in real-time.

Role of APIs in Modern Lending Platforms

APIs are the backbone of digital lending. They connect multiple systems like:

- Credit bureaus

- Banking networks

- Payment gateways

- Identity verification systems

Without APIs, lenders face:

❌ Data silos

❌ Slow approvals

❌ High operational costs

With API-based systems, lenders can:

✅ Automate workflows

✅ Reduce integration complexity

✅ Scale quickly

✅ Improve customer experience

Benefits of End-to-End Lending Solutions

1. Faster Loan Processing

Digital platforms reduce approval time from days to minutes.

2. Higher Approval Rates

AI-based decisioning improves eligibility assessment.

3. Reduced Fraud Risk

Integrated KYC & fraud APIs detect suspicious behavior early.

4. Better Customer Experience

Fully digital journey = no paperwork, no delays.

5. Regulatory Compliance

Built-in compliance ensures adherence to RBI guidelines.

6. Scalability

Cloud-based systems allow NBFCs to grow rapidly without infrastructure issues.

Why NBFCs & Fintechs Need Unified Lending Platforms

Many lenders still use separate systems for LOS, LMS, and KYC, which creates inefficiencies:

- Data duplication

- Manual reconciliation

- Integration challenges

Modern platforms solve this by offering a single unified system that integrates everything.

This approach eliminates:

❌ Multiple vendors

❌ High integration costs

❌ Operational complexity

And replaces it with:

✅ Seamless workflows

✅ Centralized data

✅ Real-time decisioning

How Roopya Provides End-to-End Lending Solutions

Platforms like Roopya offer a fully integrated lending ecosystem designed specifically for Indian NBFCs.

Key Features:

- LOS + LMS in one platform

- 300+ pre-integrated APIs

- AI-based credit decisioning

- 95% automation

- Built-in KYC & fraud detection

- No-code configuration

This means lenders can:

👉 Launch faster (within days)

👉 Reduce operational costs

👉 Improve loan approval speed

👉 Scale without technical complexity

Compliance & RBI Regulations

Digital lending in India is tightly regulated by the RBI. Lenders must ensure:

- Proper KYC verification

- Transparent loan terms

- Secure data handling

- Direct disbursement to borrower accounts

End-to-end lending platforms help automate compliance, reducing legal risks and penalties.

Future of Digital Lending (2026 & Beyond)

The future of digital lending is driven by:

AI & Machine Learning

- Predictive credit scoring

- Fraud detection

- Automated underwriting

API Ecosystem

- Account Aggregator framework

- Embedded finance

- Real-time data sharing

Mobile-First Lending

- Instant loan apps

- Paperless onboarding

Advanced Security

- Biometric verification

- Behavioral analytics

End-to-end digital lending solutions are no longer optional—they are essential for modern NBFCs and fintech companies.

By combining:

- Loan Origination System (LOS) for onboarding & approval

- Loan Management System (LMS) for servicing & collections

- KYC APIs for compliance & fraud prevention

Lenders can create a fully automated, scalable, and compliant lending ecosystem.

Platforms like Roopya take this a step further by offering all-in-one lending infrastructure, enabling businesses to launch, scale, and succeed in the competitive digital lending landscape.