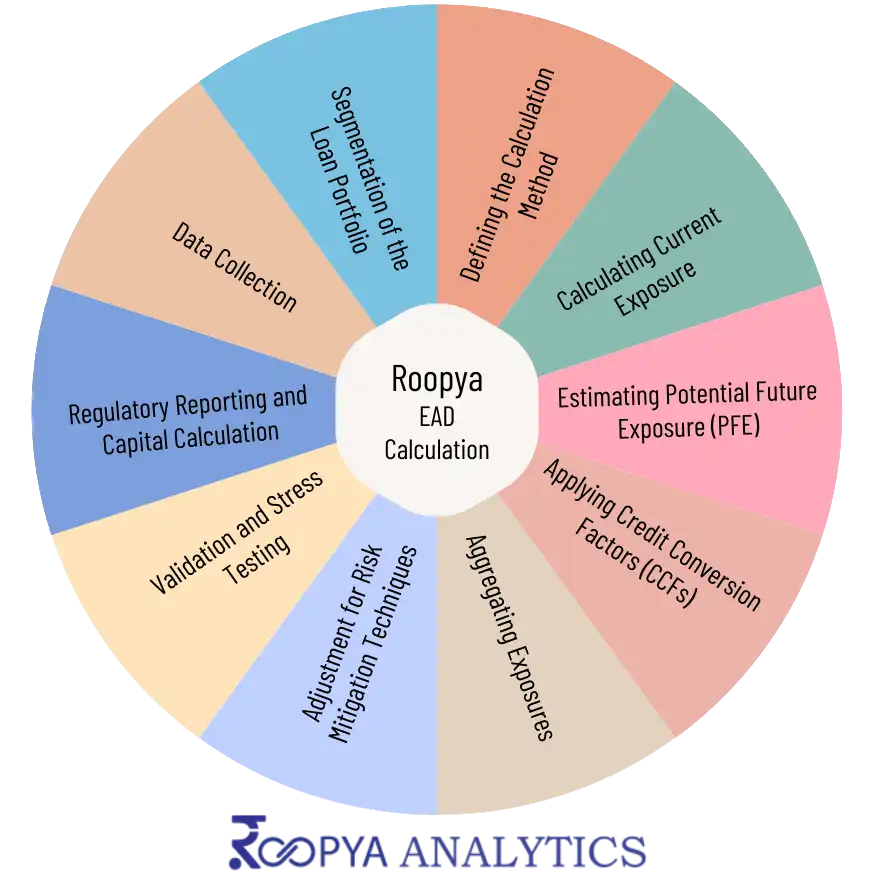

Roopya classifies the portfolio (retail, corporate, etc.) and the types of loans included. The steps and methodologies employed are:

1. Data Collection

The first step involves gathering detailed information on each loan within the portfolio, including:

- Bureau data for historical repayment and drawdown patterns Outstanding balances

- Outstanding balances

- Undrawn credit lines or commitments

- Loan terms and conditions (e.g., interest rates, maturity dates)

- Borrower information (e.g., credit ratings, financial health)

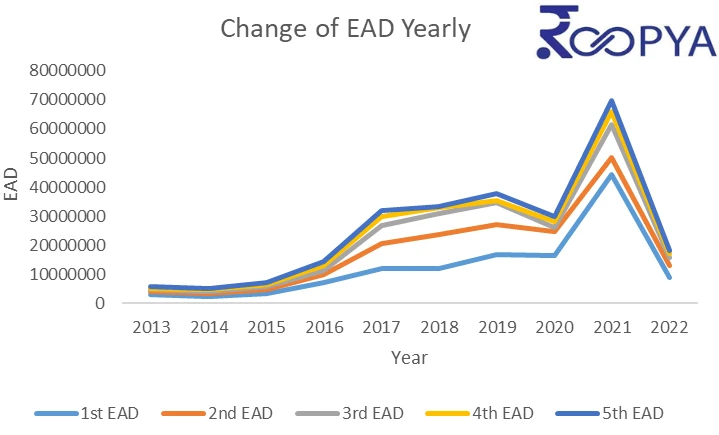

How the EAD values change over time for a portfolio. This can be particularly useful for monitoring trends, seasonal patterns, or the impact of external factors on exposure levels.

2. Segmentation of the Loan Portfolio

Loan portfolios is then segmented based on certain characteristics to refine the EAD measurement process. These characteristics can include:

- Loan type (e.g., mortgages, corporate loans, credit cards)

- Borrower type (e.g., retail, SME, corporate)

- Risk characteristics (e.g., credit rating, collateralization)

3. Defining the Calculation Method

- Current Exposure Method (CEM): Mainly used for derivative exposures, calculating the current mark-to-market value plus an add-on for potential future exposure.

- Standardized Method (SM): Applies predefined credit conversion factors (CCFs) to undrawn commitments to estimate EAD.

- Internal Model Method (IMM): Uses the institution's internal models to estimate EAD based on historical data and predictive analytics.

4. Calculating Current Exposure

For each loan or credit exposure in the portfolio, calculate the current amount exposed. This includes the outstanding balance and any accrued interest.

5. Estimating Potential Future Exposure (PFE)

This involves estimating the additional amount that might be drawn or exposed between the current date and the time of default. The estimation is based on historical drawdown patterns, borrower behavior, and macroeconomic factors. For certain types of loans, especially revolving credits or lines of credit, this step is crucial.

6. Applying Credit Conversion Factors (CCFs)

For commitments that have not been fully drawn, apply CCFs to estimate the likely amount to be drawn at the time of default. These factors are either provided by regulatory authorities or developed internally based on historical data.

7. Aggregating Exposures

Sum of the calculated EADs across all loans or credit exposures is computed in the portfolio to determine the total EAD for the portfolio.

Segmenting EAD by the credit rating of borrowers or other relevant segments (e.g., industry, geographical location). This helps assessing the risk profile of the portfolio.

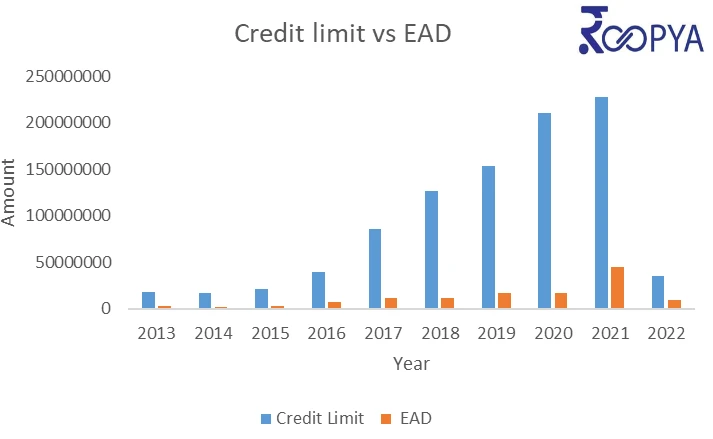

Comparing the EAD values with the respective credit limits assigned to each borrower. This can highlight instances where exposure might exceed the limits set by the risk management policy.

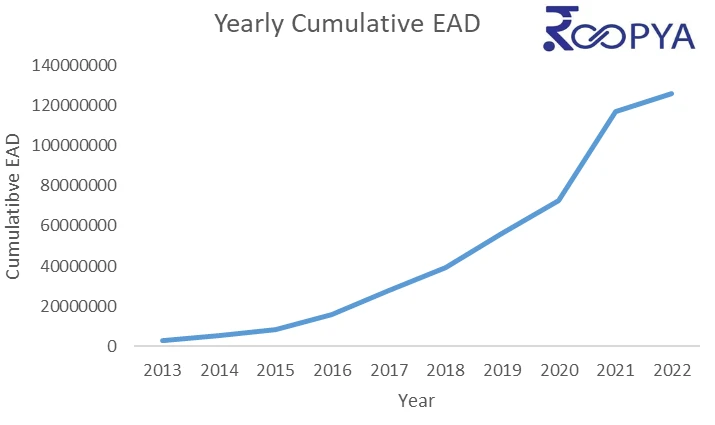

A line chart showing the cumulative EAD across the portfolio, ranked by risk or exposure size. This can be useful for stress testing and for understanding the potential impact of large defaults.

8. Adjustment for Risk Mitigation Techniques

If there are risk mitigation measures in place, such as collateral, guarantees, or credit derivatives, adjust the EAD calculation accordingly. These adjustments reflect the reduced exposure due to the risk mitigation.

9. Validation and Stress Testing

Regularly validate the EAD measurement models against actual outcomes and perform stress testing under various scenarios to ensure the robustness of the EAD estimates.

10. Regulatory Reporting and Capital Calculation

Use the EAD measurements, along with Probability of Default (PD) and Loss Given Default (LGD) estimates, for regulatory reporting purposes and to calculate the capital reserves required to cover potential credit losses.