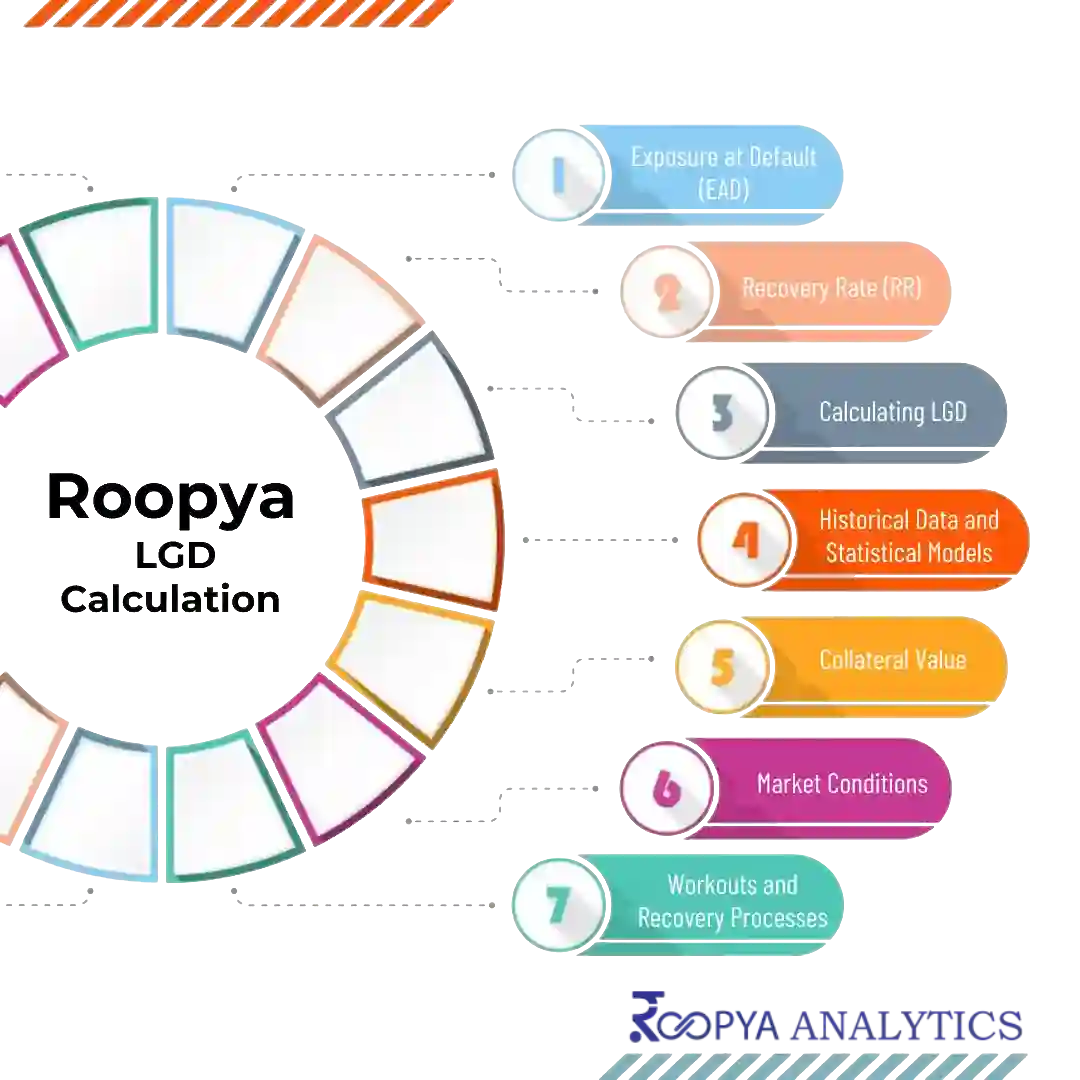

LGD is measured through a combination of historical data analysis, recovery rates, and market conditions, among other factors. The process involves several steps:

-

Exposure at Default (EAD): This is the total value that is at risk when a default occurs. It includes the outstanding balance of the loan plus any committed but undrawn amounts.

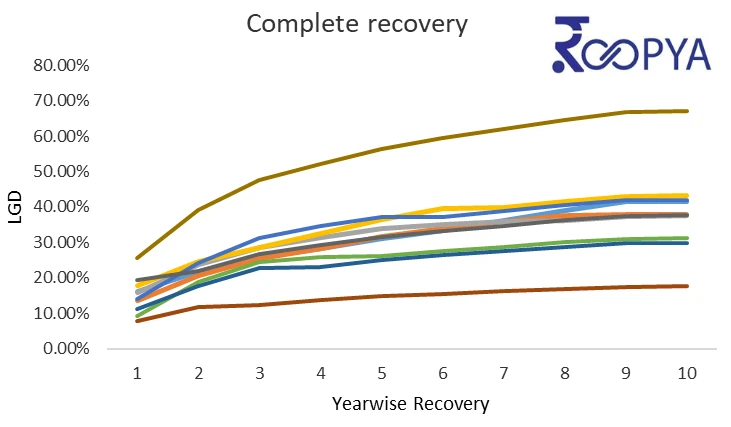

We use the following histogram or density plot showing the distribution of LGD rates observed in the past. This can help in understanding the variability of LGD and setting appropriate LGD estimates for different types of exposures.

-

Recovery Rate (RR): This is the proportion of the EAD that is recovered after the default has occurred. Recoveries can come from collateral, selling of the defaulted loans, or other methods of recuperation.

-

Calculating LGD: LGD is calculated as 1 minus the recovery rate, often expressed as a percentage. If the recovery rate is 40%, then LGD would be 60%. LGD is 1 - Recovery rate or 1 - Recovered Amount / EAD.

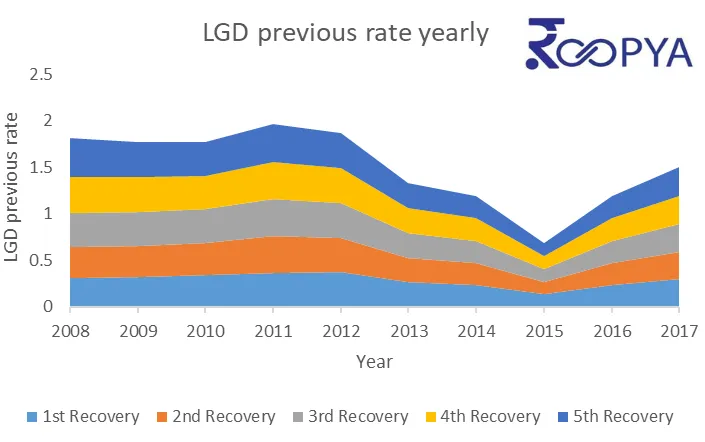

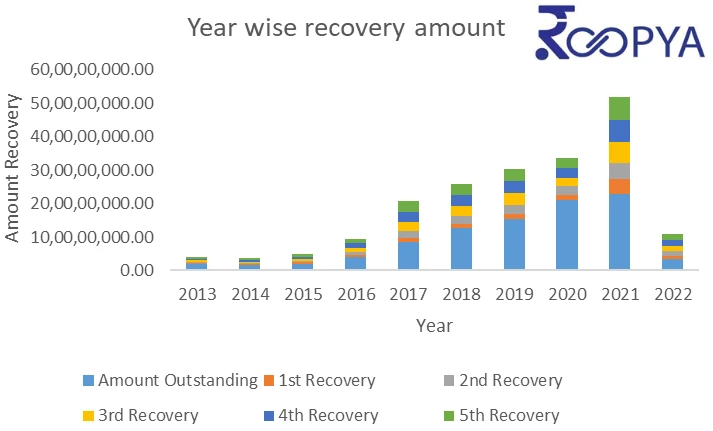

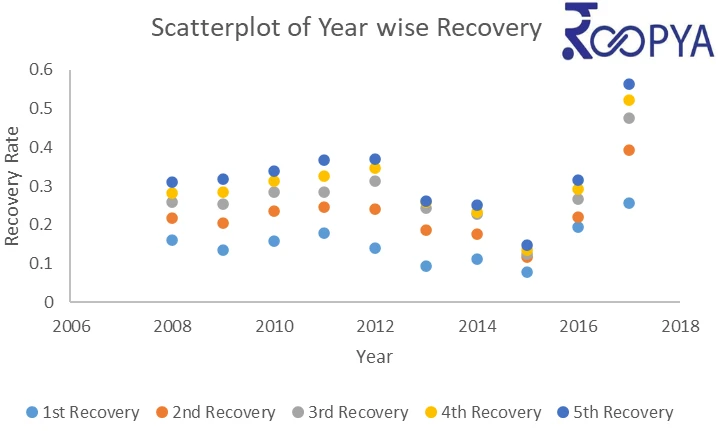

This chart will show the distribution of LGD on defaulted exposures with year wise recovery.

-

Historical Data and Statistical Models: Financial institutions use historical default and recovery data to model and predict LGD. This can involve statistical techniques, regression analysis, or machine learning models to estimate LGD based on various risk factors such as loan characteristics, borrower creditworthiness, and economic conditions.

-

Collateral Value: The value and type of collateral securing a loan significantly affect LGD. Loans secured by tangible assets like real estate typically have lower LGDs due to the potential to recover losses through the sale of the collateral.

Then we show how the value of collateral held against loans affects the LGD. It is useful for secured loans where the recovery process involves selling the collateral.

We will also show a scatter plot showing the relationship between the time taken to recover from a default and the resulting LGD. Longer recovery times can be associated with higher LGD due to the costs and depreciation of collateral value over time.

-

Market Conditions: Economic and market conditions at the time of default affect the recoverable value of collateral and, subsequently, the LGD. For instance, real estate values in a market downturn can lead to higher LGDs for mortgages.

-

Workouts and Recovery Processes: The effectiveness of a lender’s processes for managing defaulted loans, including negotiations, restructuring, and legal actions, can also impact recovery rates and LGD.

LGD is a dynamic measure that can vary significantly across different loan types, industries, and economic cycles. Financial institutions continually refine their LGD models to better predict potential losses and manage their risk exposure.