What Is a Loan Origination System (LOS)? Complete Guide for Indian NBFCs & Banks

What Is a Loan Origination System (LOS)?

A Loan Origination System (LOS) is software that automates and manages the pre-disbursement stages of lending.

It handles:

- Loan applications

- Customer onboarding

- eKYC verification

- Credit bureau checks

- Underwriting

- Risk assessment

- Approval workflows

- Document verification

- Loan sanctioning

- Disbursement processing

In simple terms, LOS acts as the digital engine that helps lenders approve loans quickly and efficiently.

Traditional lending methods relied heavily on manual processes, spreadsheets, physical documentation, and branch visits. Modern LOS platforms eliminate these inefficiencies by enabling fully digital lending journeys.

Start Free Trial

Why Loan Origination Systems Are Important in India

India’s lending ecosystem is expanding rapidly due to:

- Growth in fintech startups

- Rising digital adoption

- UPI ecosystem expansion

- Account Aggregator framework

- Demand for instant credit

- RBI digital lending guidelines

Today’s borrowers expect:

- Instant approvals

- Paperless onboarding

- Mobile-based applications

- Fast disbursement

- Transparent processes

Without a modern LOS, lenders struggle with:

- Slow approvals

- Manual errors

- High operational costs

- Compliance risks

- Poor customer experience

Modern LOS platforms solve these challenges through automation and AI-driven decision-making. According to Roopya’s lending platform insights, advanced LOS systems can automate up to 95% of the loan lifecycle and significantly reduce approval times.

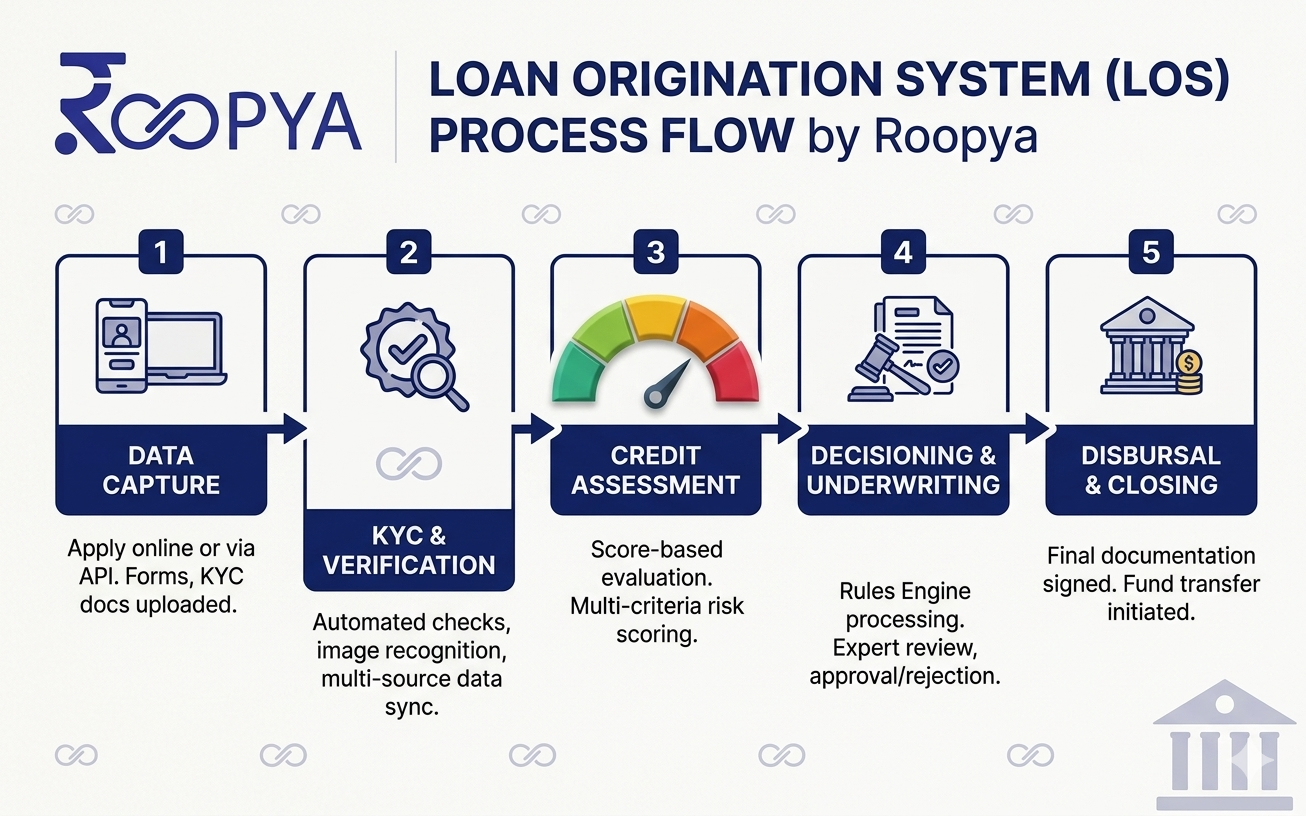

How a Loan Origination System Works

A Loan Origination System follows a structured workflow.

Step 1: Loan Application

The borrower submits an online application through:

- Website

- Mobile app

- DSA portal

- Branch system

- API integration

The LOS captures customer details digitally.

Step 2: eKYC Verification

The system verifies identity using:

- Aadhaar verification

- PAN validation

- Video KYC

- CKYC

- OCR document extraction

Modern LOS platforms integrate directly with KYC APIs for instant verification.

Step 3: Credit Bureau Check

The LOS pulls credit data from:

- CIBIL

- Experian

- Equifax

- CRIF High Mark

The platform analyzes:

- Credit score

- Existing liabilities

- Repayment history

- Delinquencies

Step 4: Bank Statement Analysis

Advanced LOS platforms analyze bank statements using AI.

This helps lenders evaluate:

- Monthly income

- Cash flow patterns

- EMI obligations

- Spending behavior

- Fraud indicators

Step 5: Underwriting & Risk Assessment

The underwriting engine evaluates borrower eligibility using:

- Rule-based decisioning

- AI models

- Risk scoring

- Fraud detection algorithms

The LOS can automatically:

- Approve

- Reject

- Send for manual review

Step 6: Loan Approval

Once approved, the LOS generates:

- Sanction letters

- Loan agreements

- Digital contracts

- Repayment schedules

Step 7: Loan Disbursement

Funds are disbursed digitally through:

- IMPS

- NEFT

- RTGS

- UPI

- Bank APIs

Some platforms enable instant disbursement within seconds.

Core Features of a Modern Loan Origination System

1. Digital Loan Application Portal

Borrowers can apply online without branch visits.

Features include:

- Mobile-friendly forms

- Dynamic application workflows

- Multi-language support

- Document upload

- Auto-save functionality

2. Automated eKYC

Digital KYC reduces fraud and onboarding time.

Key capabilities:

- Aadhaar eKYC

- PAN verification

- Face match

- OCR extraction

- Video KYC

- CKYC integration

3. AI-Based Credit Decisioning

AI-powered LOS systems analyze multiple data points to make faster and smarter lending decisions.

Benefits include:

- Better approval accuracy

- Reduced NPAs

- Faster processing

- Lower manual dependency

Roopya’s platform highlights AI-based decisioning and fraud prevention as major components of its lending infrastructure.

4. Rule Engine & Workflow Automation

Lenders can configure:

- Eligibility rules

- Approval matrices

- Product logic

- Risk policies

- Workflow routing

No-code systems allow business teams to modify workflows without developers.

5. API Integrations

A strong LOS integrates with:

- Credit bureaus

- KYC providers

- Banking APIs

- GST APIs

- Account Aggregators

- Payment gateways

- SMS/WhatsApp providers

Roopya mentions 300+ API integrations across lending workflows.

6. Fraud Detection

Advanced LOS platforms include:

- Device fingerprinting

- Behavioral analytics

- Duplicate detection

- Document authenticity checks

- Geo-verification

Fraud prevention is critical in India’s digital lending market.

7. Real-Time Analytics Dashboard

Modern systems provide dashboards for:

- Approval rates

- Loan funnel tracking

- Portfolio insights

- Risk analytics

- Branch performance

- Collection trends

8. Document Management System

An LOS should securely manage:

- Loan agreements

- KYC documents

- Bank statements

- Income proofs

- Audit trails

9. Compliance & Audit Tracking

RBI compliance requires lenders to maintain:

- Consent logs

- Data security

- Audit records

- Fair practice disclosures

- Digital lending compliance

Modern LOS platforms automate compliance workflows.

Types of Loan Origination Systems

Cloud-Based LOS

Hosted on cloud infrastructure.

Benefits:

- Faster deployment

- Lower cost

- Scalability

- Remote access

On-Premise LOS

Installed within the lender’s infrastructure.

Used mainly by:

- Large banks

- Traditional institutions

- Organizations with strict internal policies

SaaS-Based LOS

Subscription-based systems with regular updates.

Most fintech startups and NBFCs prefer SaaS LOS platforms.

Benefits of Loan Origination Systems for NBFCs & Banks

Faster Loan Approvals

Automation reduces approval times from days to minutes.

Some digital lenders approve loans in under 30 seconds.

Lower Operational Costs

Automation reduces manual processing and staffing requirements.

LOS platforms help lenders process more loans with fewer resources.

Better Customer Experience

Borrowers receive:

- Faster onboarding

- Instant status updates

- Paperless processing

- Mobile accessibility

Improved Compliance

LOS systems help institutions comply with:

- RBI digital lending guidelines

- KYC regulations

- AML requirements

- Data privacy rules

Scalability

Lenders can process thousands of applications daily without operational bottlenecks.

Reduced Fraud Risk

AI and automation improve fraud detection and risk management.

Loan Origination System vs Loan Management System (LMS)

Many lenders confuse LOS and LMS.

Loan Origination System (LOS)

Handles pre-disbursement activities:

- Application

- KYC

- Underwriting

- Approval

- Disbursement

Loan Management System (LMS)

Handles post-disbursement operations:

- EMI tracking

- Repayments

- Collections

- NPA monitoring

- Customer servicing

Modern lending platforms combine both LOS and LMS capabilities.

Industries Using Loan Origination Systems in India

NBFCs

NBFCs use LOS platforms for:

- Personal loans

- Business loans

- Gold loans

- Consumer finance

- Vehicle loans

Fintech Startups

Digital lenders depend heavily on automated LOS platforms for scaling operations.

Cooperative Societies

Cooperative lenders use LOS systems to digitize member lending.

Banks

Banks integrate LOS systems with core banking platforms.

Microfinance Institutions (MFIs)

MFIs use LOS solutions for field-based lending and rural onboarding.

RBI Compliance Requirements for LOS Platforms

Indian lenders must comply with RBI digital lending regulations.

A compliant LOS should support:

- Borrower consent tracking

- Data privacy

- Secure APIs

- Audit trails

- Fair lending disclosures

- Grievance redressal workflows

- KYC compliance

Roopya emphasizes RBI-ready workflows within its lending platform infrastructure.

AI in Modern Loan Origination Systems

Artificial Intelligence is transforming lending operations.

AI Use Cases in LOS

Credit Scoring

AI evaluates borrower behavior beyond traditional bureau scores.

Fraud Detection

Machine learning identifies suspicious activity in real time.

Automated Underwriting

AI speeds up eligibility assessment and approval decisions.

Bank Statement Analysis

AI extracts and categorizes financial data instantly.

Predictive Analytics

Lenders can forecast default risks and portfolio performance.

Challenges Without an LOS

Lenders using manual processes face:

- Slow turnaround times

- Data entry errors

- High operational costs

- Poor borrower experience

- Compliance risks

- Scalability limitations

This is why Indian lenders are rapidly adopting digital lending platforms.

How to Choose the Best LOS Platform in India

Evaluate Automation Capabilities

Look for:

- AI underwriting

- Workflow automation

- Auto decisioning

Check Integration Support

The platform should integrate with:

- KYC APIs

- Credit bureaus

- Banking systems

- Payment gateways

Verify Compliance Readiness

Ensure the LOS complies with RBI guidelines.

Assess Scalability

Choose a system capable of supporting future growth.

Prioritize User Experience

A clean interface improves both customer and employee efficiency.

Consider Deployment Speed

Modern cloud LOS platforms can go live within days instead of months.

Why Indian NBFCs Are Moving Toward Digital LOS Platforms

Several trends are accelerating LOS adoption:

- Rising fintech competition

- Consumer demand for instant credit

- RBI compliance pressure

- Mobile-first lending

- Embedded finance growth

- AI adoption in underwriting

Digital-first lenders are outperforming traditional lenders in approval speed and operational efficiency.

Why Roopya Is Emerging as a Leading LOS Platform in India

Roopya Money provides an AI-powered lending infrastructure platform designed for Indian NBFCs, fintech startups, and lenders.

Key capabilities highlighted across Roopya’s LOS ecosystem include:

- AI-driven underwriting

- 95% automation

- Digital KYC

- 300+ API integrations

- No-code workflows

- Real-time analytics

- Fraud detection

- Instant disbursement

- RBI-ready compliance workflows

According to Roopya’s platform pages, lenders can deploy the system in as little as 5–7 days.

Useful Internal Links

- Loan Origination System (LOS) Software India

- All-in-One Loan Management Software

- Best LOS & LMS for NBFCs

- Loan Management Software Platform

Future of Loan Origination Systems in India

The future of LOS platforms will be shaped by:

- AI underwriting

- Embedded lending

- Open banking

- Account Aggregator integrations

- Real-time analytics

- Hyperautomation

- Voice & vernacular onboarding

As India’s digital lending market grows, LOS platforms will become even more critical for lenders aiming to scale profitably.

A Loan Origination System is the foundation of modern digital lending.

For Indian NBFCs, banks, fintech companies, and lenders, an LOS enables:

- Faster approvals

- Better risk management

- Improved compliance

- Reduced costs

- Seamless borrower experience

The lending industry is shifting rapidly toward automation and AI-driven workflows. Institutions that continue relying on manual operations risk falling behind more agile digital competitors.

Platforms like Roopya’s LOS & Lending Infrastructure are helping Indian lenders modernize their lending operations with end-to-end automation, intelligent underwriting, and scalable digital lending infrastructure.