The Importance of Loan Management System & Software (LMS) in the Lending Industry

Lending is a deceptively complex business. From the outside, it looks straightforward — a lender provides funds, a borrower repays with interest, and the institution earns a margin. But anyone who has worked inside a bank, NBFC, or microfinance institution knows the reality is far messier. Thousands of active loan accounts. EMI schedules that need to reconcile perfectly every month. Regulatory reports due at predictable intervals. Collection workflows for borrowers who slip into delinquency. Customer service queries about outstanding balances, prepayment penalties, and foreclosure charges.

All of this — every bit of it — needs to be managed with precision, at scale, every single day.

That is exactly what a Loan Management System (LMS) does. And in today’s lending environment, where competition is fierce, margins are thin, and regulators are watchful, the importance of LMS software cannot be overstated. Whether you are a scheduled commercial bank managing a ₹10,000 crore retail book or a growing NBFC disbursing ₹50 crore a month, the right loan management platform is the difference between a lending business that scales profitably and one that strains under its own operational weight.

This article examines why loan management systems have become indispensable to the lending industry — what they do, what problems they solve, and what the cost of operating without one truly looks like.

Start Free Trial

Understanding What a Loan Management System Actually Is

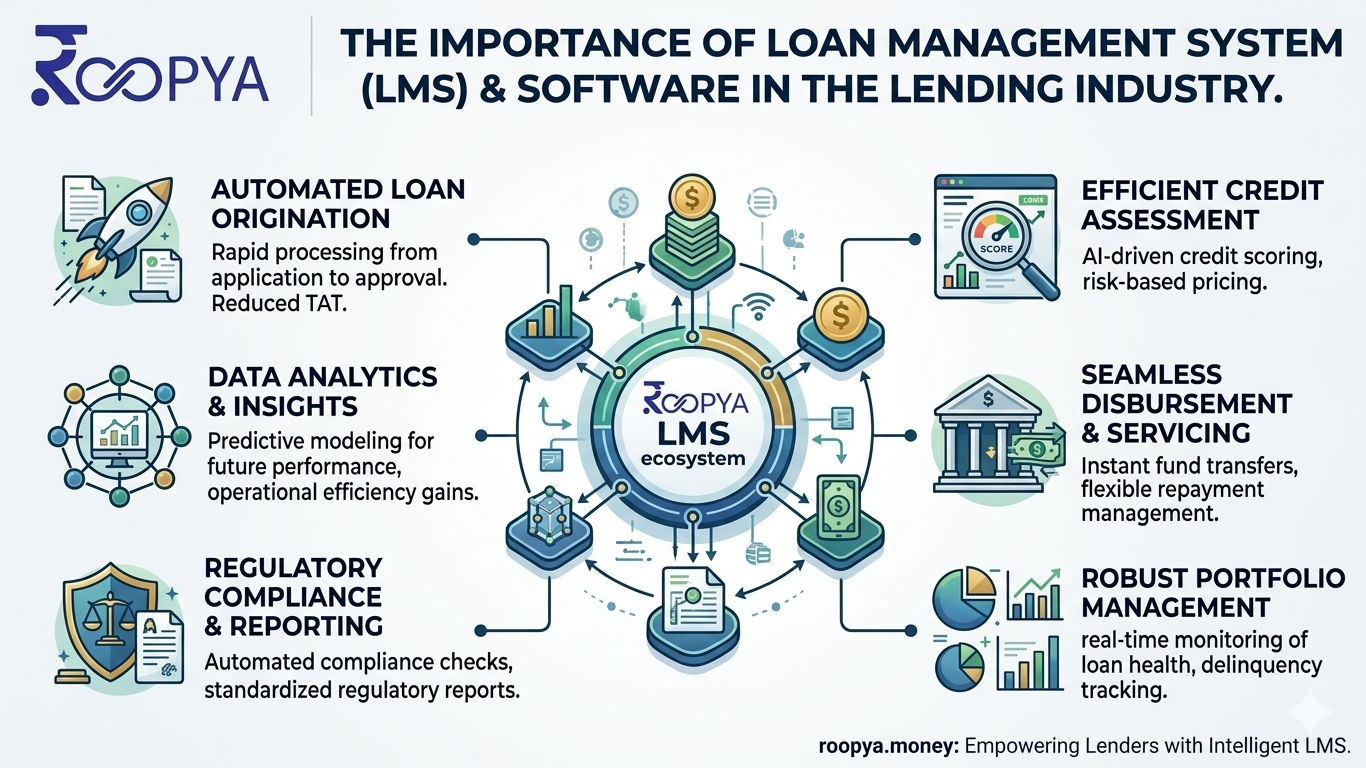

A Loan Management System is a software platform that manages the full lifecycle of a loan after it has been sanctioned — from disbursement through repayment, restructuring, prepayment, and eventual closure. It is the operational backbone of a lending institution’s post-origination activities.

To be precise about the scope: a Loan Origination System (LOS) handles the front end of lending — application, credit assessment, underwriting, and approval. The Loan Management System (LMS) takes over from the moment the loan is disbursed and stays active until the account is fully closed.

In practice, the two systems are deeply interrelated. The origination platform feeds verified borrower data, approved loan terms, and documentation into the management system. From that point, the LMS governs everything: generating amortisation schedules, processing monthly EMIs, managing NACH mandates, tracking delinquencies, calculating interest accruals, handling prepayments, and producing regulatory reports.

Modern platforms like Roopya offer both systems in a unified, no-code, cloud-native infrastructure — so the borrower data, credit decisions, and repayment behaviour all live in one ecosystem. This eliminates the integration gaps and data reconciliation headaches that plague institutions running separate, disconnected systems for origination and servicing.

Why the Lending Industry Cannot Afford to Underestimate LMS Software

1. The Loan Book Doesn’t Manage Itself

One of the most common misconceptions among smaller lenders — particularly those transitioning from manual operations — is that once a loan is disbursed, the hard work is done. In reality, disbursement is where the management challenge begins.

Consider a mid-sized NBFC with 15,000 active loan accounts. Every month, it needs to:

- Correctly calculate the EMI due for each account, accounting for variable interest rates, moratoriums, restructurings, and part-prepayments

- Present mandates through NACH channels and reconcile which payments came in and which did not

- Identify accounts that missed a payment and classify them into the correct DPD (Days Past Due) bucket

- Generate provisioning calculations for the finance team

- Update each account’s outstanding balance, interest accrued, and principal repaid

- Produce borrower statements on request

Without an LMS, all of this relies on spreadsheets, manual entries, and the institutional memory of individual staff members. The error rate is high, the operational cost per account is unsustainable, and the risk of misclassifying a delinquent account — or worse, generating an incorrect amortisation schedule that misleads a borrower — is significant.

An LMS automates every one of these tasks. The system computes amortisation schedules at the time of disbursement, auto-deducts EMIs through integrated payment gateways, reconciles transactions in real time, and classifies accounts into correct DPD buckets without human intervention. Staff time is freed for exceptions, relationships, and growth.

2. Regulatory Compliance Demands It

The Reserve Bank of India’s regulatory framework for lending institutions is comprehensive and unforgiving. NBFCs are required to comply with asset classification norms (standard, SMA-0, SMA-1, SMA-2, substandard, doubtful, loss), maintain precise provisioning calculations, submit periodic returns on portfolio composition, and adhere to the Fair Practices Code in every borrower interaction.

For scheduled commercial banks, the compliance requirement is even more extensive — CRR, SLR, ALM reports, NPA disclosures, credit concentration reporting, and sector-wise exposure limits are all subject to regular scrutiny.

Without a robust loan management system, generating these reports accurately requires a laborious manual process of pulling data from multiple sources, reconciling discrepancies, and hoping nothing was missed. The margin for error is zero — a misclassified NPA or an incorrect provisioning figure can trigger regulatory action, impact credit ratings, and damage the institution’s reputation.

A modern LMS like Roopya’s platform handles compliance as a native function, not an add-on. Asset classification runs automatically based on DPD logic configured to RBI norms. Provisioning is calculated at the portfolio level in real time. Regulatory reports — NPA reports, ALM statements, credit bureau submissions — are generated directly from the system’s data layer, with audit trails that document every transaction and decision. The compliance burden on operations teams drops dramatically, and the risk of regulatory non-compliance approaches zero.

This matters especially as the RBI continues to tighten its supervision of NBFCs and digital lenders. Institutions with clean, auditable data systems are better positioned to respond to regulatory queries quickly and confidently. Those relying on manual records face a stressful scramble every time an inspection is announced.

3. Collections Efficiency Directly Impacts Profitability

The health of a lending institution’s loan book is determined not just by how well it originates loans, but by how effectively it manages repayments and recoveries. Collections is where profitability is either protected or eroded — and it is one of the areas where loan management software creates the most direct financial impact.

A well-designed LMS includes a sophisticated collections module that goes far beyond sending reminder SMS messages. Effective LMS-driven collections involves:

Early Warning Detection: The system continuously monitors account behaviour — payment patterns, balance trends, external bureau triggers — and flags accounts showing early signs of stress before they become delinquent. Acting on SMA-0 accounts (accounts that are 0–30 days overdue) is dramatically more cost-effective than recovering from substandard assets.

Automated Communication at Scale: The LMS triggers personalised communications through SMS, email, and WhatsApp at appropriate points in the collection cycle — a gentle reminder three days before EMI due date, a follow-up on the due date, and a more urgent outreach 5 days after a missed payment. All of this happens automatically, without requiring collections staff to manually identify who to call.

Intelligent Agent Assignment: For accounts that move into delinquency despite automated outreach, the LMS assigns cases to collections agents based on geography, account value, and DPD bucket. Agent performance is tracked, and strategies are optimised based on historical recovery data.

Payment Promise Tracking: When a borrower commits to paying by a specific date, the LMS logs the promise and monitors whether it is kept. If the date passes without payment, the system escalates the account automatically.

Settlement and Restructuring Workflows: For accounts that require more complex resolution — settlement offers, EMI restructuring, moratorium extensions — the LMS provides a structured workflow that ensures the right authorisations are obtained, the revised terms are accurately reflected in the account, and the documentation is maintained for audit purposes.

Roopya’s loan management platform includes all of these capabilities, powered by AI-driven collection strategies that learn from portfolio outcomes and continuously optimise which interventions work best for which borrower segments. Institutions using AI-driven collection systems report recovery rate improvements of 30–60% compared to purely manual collections operations.

4. Scalability: Growing the Book Without Growing the Headcount

Every lending institution faces a fundamental scaling constraint: as the loan book grows, the operational complexity grows with it. More accounts mean more EMI cycles to process, more payment reconciliations to complete, more collection cases to manage, and more regulatory data to compile.

In a manual or partially digitised environment, this scaling constraint is almost entirely a headcount constraint. Doubling the loan book size requires roughly doubling the operations team. The marginal cost per loan stays high, limiting how profitable growth can actually be.

A loan management system decouples operational capacity from headcount. The system processes 10,000 EMI transactions with the same effort as 1,000. Reconciliation is automated regardless of volume. DPD classification runs nightly across the entire portfolio, not just the accounts an analyst happened to review. Regulatory reports cover the full book with a single generation run.

This means that as a lending institution grows, its unit economics improve rather than deteriorate. A bank that processes ₹100 crore in monthly EMIs with a 20-person operations team can often grow to ₹400 crore with the same team once a proper LMS is in place. The incremental cost of managing each additional loan account drops significantly.

Roopya’s cloud-native architecture is built specifically for this kind of scaling. The platform handles automatic capacity scaling during high-volume processing periods — like the EMI surge on the 1st and 5th of every month — without performance degradation. Banks and NBFCs using Roopya do not need to provision expensive on-premises infrastructure to handle peak loads; the cloud does it automatically.

The no-code configuration layer adds another dimension to scalability. When a lending institution wants to launch a new loan product — a top-up loan facility, a co-lending product, or a revised restructuring scheme — the business team can configure the product in the LMS without waiting for IT development cycles. Product agility becomes a competitive advantage rather than a technology bottleneck.

5. Customer Experience After Disbursement Is a Competitive Differentiator

Most lending institutions invest heavily in the borrower acquisition and origination experience — a smooth digital application, fast approval, and quick disbursement. But the post-disbursement experience — the years of EMI payments, account queries, and service interactions that follow — is often an afterthought.

This is a strategic mistake. A borrower’s loyalty to a lender is built not primarily on how painless the approval process was, but on how well they are served over the life of the loan. A borrower who can view their outstanding balance, download statements, make prepayments, and raise service requests through a self-service portal — without ever needing to call a branch or wait on hold — is a satisfied borrower who will return for their next credit need.

A modern LMS delivers this through a well-designed customer portal that provides:

- Real-time account dashboard showing current outstanding, next EMI date, and payment history

- Statement download for any period, instantly, without staff intervention

- Online EMI payment with instant receipt generation

- Prepayment calculator showing interest savings for different prepayment amounts

- Service request submission and tracking for changes like address updates or repayment date modifications

- NOC and no-due certificate generation at loan closure

Roopya’s platform includes this borrower-facing customer portal as a native component of the LMS, not a separately priced add-on. Borrowers access it through mobile or web, and every interaction is logged for audit purposes. The operational benefit to the lending institution is significant — fewer inbound service calls, lower customer support costs, and faster query resolution.

Beyond the portal, the LMS also enables proactive borrower communication that builds trust. An automatic notification when an EMI mandate is registered. A confirmation SMS when a payment is processed. An alert when a loan is about to be closed, with the option to apply for a top-up. These touchpoints, all automated through the LMS, create a relationship that feels managed and attentive rather than transactional and indifferent.

6. Data and Analytics: Turning Loan Data Into Strategic Intelligence

A loan management system is not just an operational tool — it is one of the richest sources of strategic data that a lending institution possesses. Every EMI paid or missed, every prepayment made, every restructuring requested tells a story about borrower behaviour, product performance, and portfolio health.

Without an LMS, this data sits in disconnected spreadsheets and legacy systems, largely inaccessible for analysis. With a modern LMS, it becomes a continuous stream of intelligence that drives better business decisions.

Portfolio analytics shows which loan products, geographies, or borrower segments are performing well and which are generating disproportionate delinquency. Vintage analysis reveals whether loans originated in a particular quarter are tracking better or worse than historical cohorts — an early indicator of underwriting quality. Approval and rejection analytics help credit teams calibrate their policies. Collections efficiency metrics show which agent strategies are working and which are not.

Roopya’s LMS includes real-time dashboards and a custom report builder that allows operations, risk, and finance teams to generate the specific views they need without depending on IT. Senior management can track portfolio KPIs — disbursement volumes, collection efficiency ratios, NPA trends, yield — in real time rather than waiting for a monthly MIS report compiled by hand.

For institutions looking to deepen their analytical capabilities, Roopya also integrates with its Lending Analytics and Credit Risk Analytics modules, enabling advanced portfolio modelling, stress testing, and expected credit loss (ECL) calculations under Ind AS 109 — all connected to live LMS data.

The Real Cost of Operating Without a Loan Management System

At this point, the benefits of an LMS are clear. But it is worth stating plainly what the alternative looks like — because many institutions underestimate the true cost of their current state.

Operating a growing loan book without a dedicated LMS means:

- Operational errors in EMI calculations and payment reconciliation that create borrower disputes and trust erosion

- Compliance risk from manual NPA classification and provisioning that may not consistently reflect RBI norms

- Higher NPAs from reactive rather than proactive collections, driven by lack of early warning visibility

- Slower growth because operations bottlenecks cap how many loans can be serviced without adding headcount

- Regulatory exposure during audits when data cannot be produced quickly, cleanly, and with full audit trails

- Poor customer experience when borrowers cannot self-serve and must call a branch for basic account information

Each of these costs is real and measurable. Together, they make the case that the question is not whether a lending institution can afford to invest in a loan management system — it is whether it can afford not to.

Why Roopya’s LMS Is Built for India’s Lending Reality

Roopya’s Loan Management System is designed specifically for the needs of Indian banks, NBFCs, MFIs, and modern lenders — not adapted from a foreign platform with limited relevance to the Indian regulatory and payment infrastructure context.

Key capabilities that make it the right choice for Indian lenders:

- No-Code Configuration: Business teams configure loan products, repayment schedules, and workflows without writing code. Product launches that used to take months now take days.

- NACH/eNACH Integration: Native integration with India’s NACH infrastructure for automated mandate registration, debit scheduling, and payment reconciliation.

- Bureau Reporting: Automated credit information submissions to CIBIL, Experian, Equifax, and CRIF, ensuring the bureau reflects accurate account status.

- RBI-Ready Compliance Reports: Pre-built regulatory report templates updated as RBI guidelines evolve, so institutions are always compliant.

- AI-Driven Collections: Machine learning models optimise collection strategies based on the institution’s own portfolio data.

- Cloud-Native Scalability: 99.9% uptime guarantee with automatic scaling for EMI surge periods.

- Go Live in 5–7 Days: The entire implementation — including product configuration, integration setup, and team training — is completed in under a week.

And critically, all of this is available on a pay-as-you-use model with zero upfront cost — making enterprise-grade loan management infrastructure accessible to institutions of every size, not just the large players with deep technology budgets.

The lending industry is unforgiving of operational inefficiency. In a business where margins are measured in basis points, defaults are measured in percentage of portfolio, and regulatory compliance is non-negotiable, the quality of the technology infrastructure that manages loan accounts is a direct determinant of institutional health.

A Loan Management System is not a luxury or an upgrade for large banks only. It is the operational foundation that every lending institution needs to manage its book responsibly, serve borrowers well, stay compliant, and grow without hitting a ceiling imposed by manual processes.

The institutions that have made this investment are growing their loan books faster, reporting healthier asset quality, passing regulatory inspections with greater confidence, and retaining more customers through better post-disbursement service. Those operating without modern LMS software are working harder to stand still — and the gap is widening every quarter.

If your institution is ready to move from spreadsheets and manual processes to a purpose-built, AI-powered loan management platform, Roopya is built for exactly that transition.

Request a demo at roopya.money and see how India’s most advanced LMS platform can transform your lending operations — from disbursement to closure, and every EMI in between.

Roopya is India’s #1 digital lending software platform, offering a complete Loan Management System (LMS), Loan Origination System (LOS), Collections, Early Warning, and Lending Analytics — all in one no-code, cloud-native platform. Learn more at roopya.money.