How to Automate EMI Collection with NACH, DPD Triggers & Field Workflows

In India’s fast-growing digital lending ecosystem, collections have become the most critical function for NBFCs and fintech lenders. While loan disbursement can drive rapid portfolio growth, poor collection management can quickly increase NPAs, reduce cash flow, and damage profitability.

In 2026, manual collection processes are no longer sustainable.

Modern NBFCs are now adopting automated EMI collection systems powered by:

- NACH mandates

- UPI Autopay

- DPD-based workflows

- AI-driven reminders

- Field collection applications

- Recovery analytics

- Early warning systems

With RBI increasing focus on compliant recovery practices, lenders must modernize their collection infrastructure while improving borrower experience.

This guide explains how NBFCs can automate EMI collection using modern Loan Management Systems (LMS) like those offered by Roopya Money.

Start Free Trial

Why EMI Collection Automation Matters in 2026

India’s lending market is expanding rapidly across:

- Personal loans

- MSME loans

- BNPL

- Gold loans

- Vehicle loans

- Microfinance

- Embedded lending

As loan volumes increase, manual recovery processes become inefficient.

Without automation, lenders face problems such as:

- Missed repayments

- Delayed collection follow-ups

- Higher operational costs

- Rising DPD buckets

- Poor recovery visibility

- Compliance risks

- Customer dissatisfaction

Automated collection systems help lenders scale efficiently while reducing delinquency.

What Is EMI Collection Automation?

EMI collection automation refers to using software and payment infrastructure to automate the repayment lifecycle.

This includes:

- Auto-debit setup

- EMI reminders

- Payment tracking

- Bounce handling

- DPD monitoring

- Recovery assignment

- Field collection routing

- Settlement tracking

- Customer communication

A modern Loan Management System automates these workflows end-to-end.

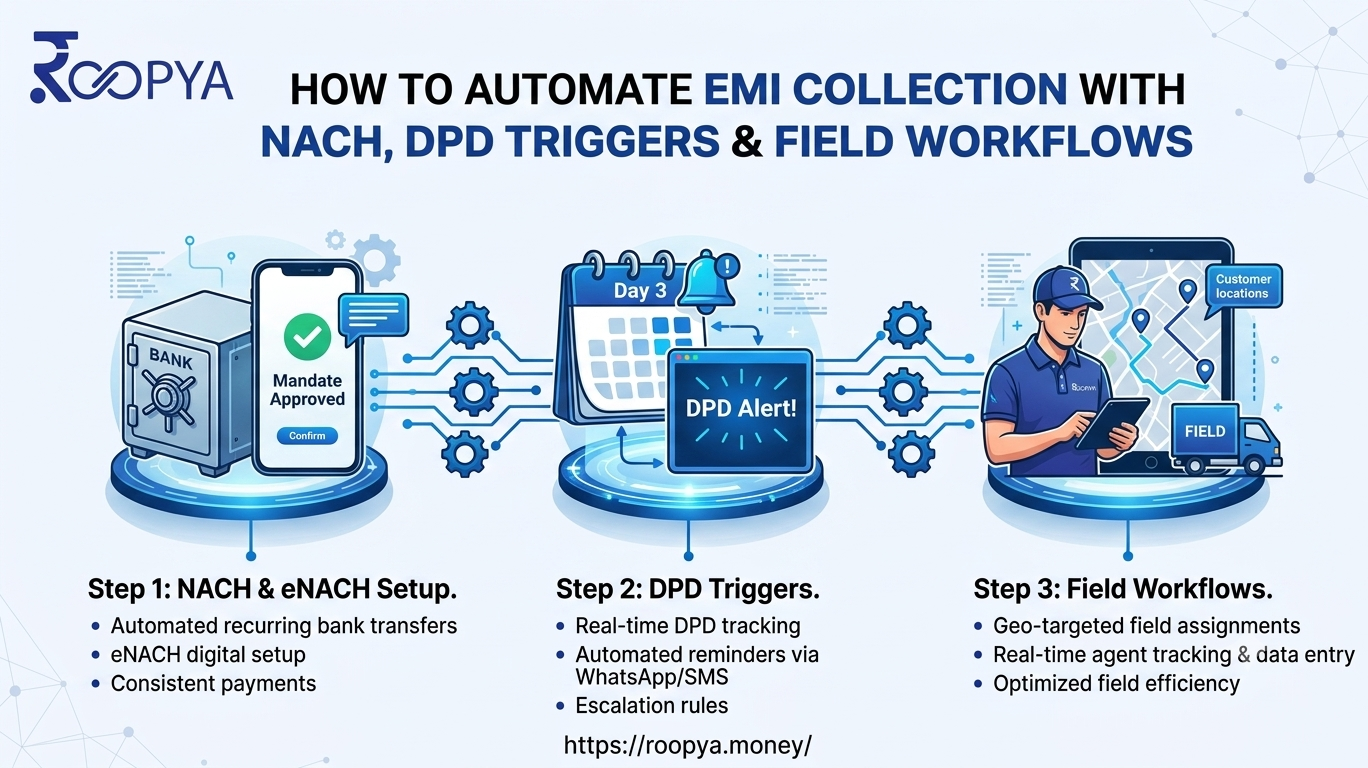

Understanding NACH in Loan Collections

What Is NACH?

The National Payments Corporation of India developed the National Automated Clearing House (NACH) framework to automate recurring bank transactions.

NACH allows NBFCs to collect EMIs automatically from borrower bank accounts.

It is one of the most widely used repayment mechanisms in India.

How NACH Works

Step 1: Borrower Authorization

The borrower approves an eMandate during onboarding.

Step 2: Mandate Registration

The lender registers the mandate with the banking network.

Step 3: EMI Presentation

The system automatically presents EMI requests on due dates.

Step 4: Debit Processing

The bank debits the borrower account.

Step 5: Status Updates

The lender receives:

- Success reports

- Bounce reports

- Failure reasons

This entire process can be automated through a modern LMS.

Benefits of NACH Automation for NBFCs

Higher Collection Efficiency

Automated debits reduce missed payments.

Lower Operational Cost

Less manual follow-up is required.

Better Customer Experience

Borrowers avoid manual repayment steps.

Reduced Delinquency

Timely deductions improve repayment discipline.

Scalable Operations

Lenders can manage lakhs of EMI transactions daily.

What Are DPD Triggers?

DPD stands for Days Past Due.

It measures how many days a borrower has missed a scheduled payment.

For example:

| Status | Meaning |

| 0 DPD | Payment on time |

| 1–30 DPD | Early delinquency |

| 31–60 DPD | Medium risk |

| 61–90 DPD | High risk |

| 90+ DPD | Potential NPA |

DPD triggers automate actions based on delinquency stages.

Why DPD Automation Is Critical

Without automated DPD tracking, recovery teams cannot prioritize risk effectively.

Modern systems automatically trigger:

- SMS reminders

- WhatsApp alerts

- Call center tasks

- Field visits

- Escalations

- Legal workflows

based on borrower risk level.

Automated DPD Workflow Example

Before EMI Due Date

- Reminder SMS

- WhatsApp notification

- Payment link sharing

On Due Date

- NACH presentation

- UPI Autopay trigger

1 DPD

- Soft reminder

- Automated IVR call

5 DPD

- Collection agent assignment

15 DPD

- Escalation to senior recovery team

30+ DPD

- Field recovery workflow activation

60+ DPD

- Settlement negotiation process

This reduces manual intervention significantly.

Role of Loan Management Systems in EMI Automation

A modern Loan Management System acts as the central engine for collections.

Core Collection Features

NACH Management

Track mandates, status, retries, and failures.

UPI Autopay

Enable recurring digital repayments.

Bounce Handling

Automatically identify failed transactions.

DPD Classification

Categorize delinquent borrowers instantly.

Collection Allocation

Assign recovery agents automatically.

Field Collection App

Enable on-ground recovery tracking.

Payment Reconciliation

Match incoming payments in real-time.

UPI Autopay vs NACH

| Feature | NACH | UPI Autopay |

| Bank Account Based | Yes | Yes |

| Real-Time | Limited | Faster |

| Customer Experience | Traditional | Better |

| Setup Complexity | Moderate | Lower |

| Popularity | High | Rapidly growing |

| Mobile Friendly | Moderate | Excellent |

Most NBFCs now support both systems.

Field Collection Workflows Explained

Field collections remain important in:

- Microfinance

- Vehicle loans

- Gold loans

- Rural lending

- High-risk portfolios

Modern field collection systems digitize recovery operations.

Key Features of Field Collection Software

Geo-Tagged Visits

Track agent visit locations.

Mobile Collection App

Agents update recovery status instantly.

Digital Receipts

Borrowers receive instant payment confirmation.

Route Optimization

Reduce travel time for recovery teams.

Real-Time Escalation

Managers monitor field activity live.

Why Manual Collections Fail

Traditional collection processes face several issues:

- Spreadsheet dependency

- No real-time visibility

- Duplicate follow-ups

- Poor borrower communication

- Delayed escalations

- Compliance risks

Automation eliminates these inefficiencies.

RBI Compliance in EMI Collection

The Reserve Bank of India has strengthened recovery compliance norms for digital lenders.

NBFCs must ensure:

- Transparent borrower communication

- Ethical recovery practices

- Audit trails

- Consent-based communication

- Data protection

A compliant LMS helps automate these controls.

Collection Communication Automation

Modern systems automate borrower communication through:

| Channel | Use Case |

| SMS | EMI reminders |

| Payment links | |

| Statements | |

| IVR | Auto-calling |

| Push Notifications | App reminders |

This improves repayment rates significantly.

AI in EMI Collections

AI-powered collection systems now predict delinquency risks before default occurs.

AI-Based Capabilities

Risk Scoring

Identify likely defaulters early.

Collection Prioritization

Focus efforts on high-risk accounts.

Smart Communication Timing

Send reminders when borrowers are most responsive.

Behavioral Analysis

Track repayment patterns.

Early Warning Systems in Collections

An Early Warning System (EWS) identifies potential default signals such as:

- Reduced bank balance

- EMI bounce patterns

- Declining transaction activity

- Increased DPD trend

- Multiple missed calls

NBFCs use EWS to intervene before accounts become NPAs.

Recovery Workflow Automation

Modern systems automate:

- Agent allocation

- Bucket management

- Escalation rules

- Settlement approval

- Legal handover

This increases operational efficiency.

Collection Analytics That Matter

Important Metrics

| Metric | Purpose |

| Collection Efficiency Ratio | Recovery performance |

| Bounce Rate | Failed payment analysis |

| Roll Rate | Bucket movement |

| Resolution Time | Recovery speed |

| DPD Distribution | Portfolio health |

Real-time dashboards help management make faster decisions.

Challenges in EMI Collection Automation

Mandate Failures

Some borrowers lack sufficient bank balance.

Customer Resistance

Borrowers may disable mandates.

Multiple Bank Accounts

Tracking repayment sources becomes difficult.

Rural Connectivity Issues

Field collections remain necessary in some areas.

Despite these challenges, automation dramatically improves efficiency.

Best Practices for NBFC Collection Automation

Use Multiple Repayment Channels

Support:

- NACH

- UPI

- Debit cards

- Wallets

- QR payments

Automate Escalations

Never rely solely on manual follow-ups.

Track Every Borrower Interaction

Maintain audit logs for compliance.

Integrate Field Recovery

Digital and physical recovery must work together.

Monitor Portfolio Health Daily

Real-time analytics prevent rising NPAs.

How Embedded Finance Impacts Collections

Embedded lending increases collection complexity because loans originate inside:

- E-commerce apps

- B2B platforms

- Mobility apps

- SaaS platforms

An API-first LMS helps lenders manage repayment infrastructure efficiently.

Why Cloud-Based Collection Systems Are Growing

Cloud collection systems offer:

- Faster deployment

- Lower infrastructure cost

- Better scalability

- Easier API integrations

- Real-time monitoring

This is why most fintech lenders prefer cloud LMS platforms in 2026.

Key Features to Look for in Collection Software

Mandatory Features

- NACH automation

- UPI Autopay

- DPD workflows

- Recovery allocation

- Field collection app

- Real-time dashboards

- Compliance audit logs

- API integrations

- AI risk alerts

- Multi-channel communication

How Roopya Money Helps Automate Collections

Roopya Money provides advanced collection automation solutions for Indian NBFCs and fintech companies.

Core Solutions

Loan Management System

Automate repayment tracking and servicing.

Collection Management System

Improve recovery performance using DPD-based workflows.

Early Warning System

Detect risky borrowers early.

Lending Analytics

Monitor portfolio health in real-time.

API Integrations

Connect with banks, payment gateways, bureaus, and communication platforms.

Benefits of Using Roopya Money Collection Solutions

Faster Collections

Reduce manual follow-ups.

Lower Delinquency

Improve repayment discipline.

Reduced Operational Cost

Automate repetitive tasks.

Better Compliance

Maintain RBI-compliant workflows.

Higher Scalability

Handle growing loan portfolios efficiently.

Future of Collections in India

By 2026 and beyond, collections will become increasingly:

- AI-driven

- Predictive

- Automated

- API-powered

- Real-time

Lenders that fail to modernize collection infrastructure may struggle with rising NPAs and operational inefficiencies.

Final Thoughts

EMI collection automation is no longer optional for Indian NBFCs.

With increasing loan volumes and stricter RBI compliance requirements, lenders need:

- NACH automation

- DPD-based workflows

- AI-powered analytics

- Field collection integration

- Real-time dashboards

A modern Loan Management System enables NBFCs to:

- Improve collection efficiency

- Reduce NPAs

- Enhance borrower experience

- Scale operations sustainably

For NBFCs and fintech lenders looking to modernize collections, automation is the key to long-term profitability.

To explore advanced collection automation solutions, visit: Roopya Money