Cloud-Based NBFC Software Solutions in India

Why Cloud-Based NBFC Software Is No Longer Optional

India’s NBFC sector is undergoing a seismic shift. With over 9,000 registered NBFCs operating across the country, the competition to acquire borrowers, disburse faster, and manage risk intelligently has never been fiercer. In this landscape, cloud-based NBFC software solutions have moved from being a “nice to have” technology advantage to an absolute operational necessity.

Traditional on-premise lending systems are expensive to deploy, slow to upgrade, and wholly inadequate for the pace at which digital lending in India is evolving. NBFCs that continue to rely on legacy infrastructure are already losing ground — in loan processing speed, cost efficiency, regulatory compliance, and customer experience — to leaner, cloud-native competitors.

This guide explores everything a modern NBFC needs to know about cloud-based software solutions in India: what they are, what to look for, how they solve real operational pain points, and why platforms like **Roopya** are setting the gold standard for the industry.

Start Free Trial

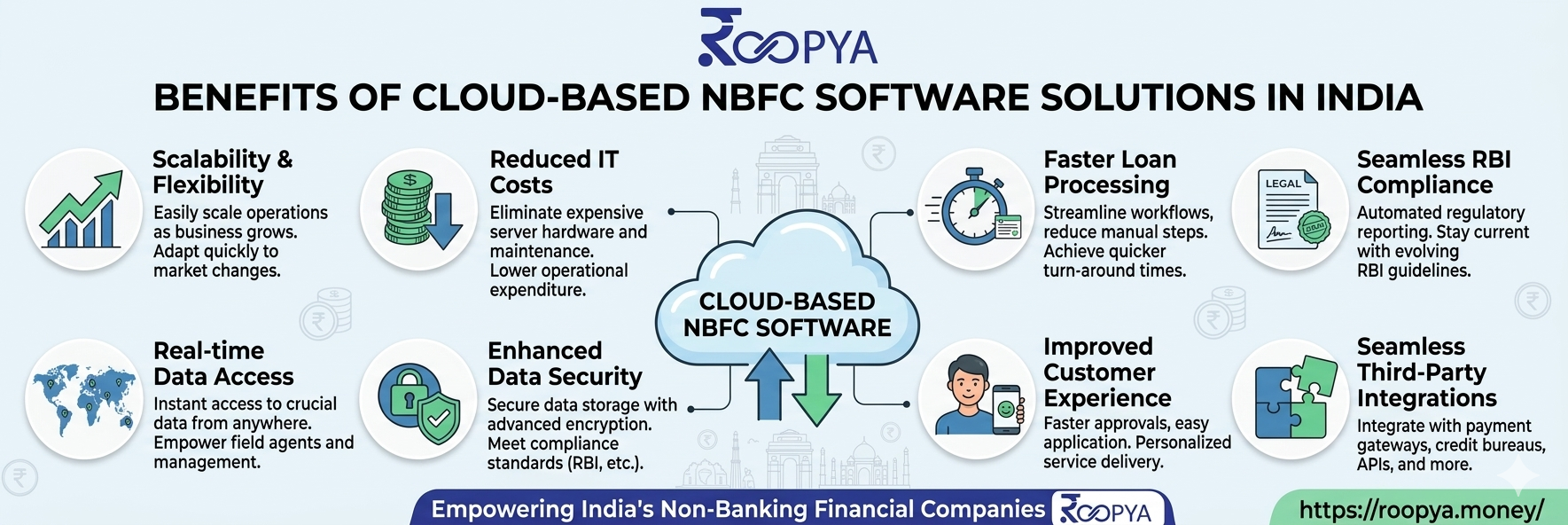

Cloud-based NBFC software is a digital lending infrastructure hosted on remote servers and delivered over the internet, eliminating the need for costly on-premise hardware, dedicated IT teams, or complex software installations. It typically encompasses:

What Is Cloud-Based NBFC Software?

Cloud-based NBFC software is a digital lending infrastructure hosted on remote servers and delivered over the internet, eliminating the need for costly on-premise hardware, dedicated IT teams, or complex software installations. It typically encompasses:

- Loan Origination System (LOS): Digitising the entire process from loan application to disbursement.

- Loan Management System (LMS): Managing the full lifecycle of a loan post-disbursement — repayments, EMI schedules, collections, and portfolio oversight.

- Collections Management: Automating borrower communication and recovery workflows.

- Credit Risk Analytics: AI/ML-powered credit scoring, PD modelling, and early warning signals.

- Regulatory Reporting: Auto-generating compliance reports for RBI, CERSAI, and other authorities.

The cloud delivery model means NBFCs can access all of these capabilities as a subscription service — paying only for what they use, scaling instantly as the business grows, and receiving continuous platform updates without disruptive upgrade cycles.

The State of Cloud Lending Technology in India

India’s digital lending market is projected to reach 515 billion by 2030. Regulatory developments — from RBI’s digital lending guidelines to the Account Aggregator framework — are actively pushing NBFCs towards digitised, auditable, and transparent lending operations.

The growth of UPI, the expansion of India Stack, and increased smartphone penetration have together created a borrower base that expects instant credit decisions, minimal documentation, and fully digital journeys. Meeting these expectations is simply not possible with legacy NBFC software. Cloud-based solutions address these imperatives directly:

- Speed: Loan origination timelines that once took days can now be compressed to minutes.

- Scale: Cloud infrastructure scales dynamically with application volumes — critical during festive seasons or rapid growth phases.

- Compliance: Leading platforms are continuously updated to reflect RBI guidelines, ensuring NBFCs always remain compliant.

- Data Security: Reputable cloud NBFC platforms offer enterprise-grade security, encryption, and access controls that most NBFCs could never afford to build in-house.

Key Features to Look for in Cloud-Based NBFC Software

Choosing the right cloud NBFC platform is one of the most consequential technology decisions an NBFC will make. Here are the non-negotiable capabilities to evaluate:

1. End-to-End Loan Origination System (LOS)

A robust LOS should support fully digital application forms, real-time bureau checks, automated KYC through Aadhaar/DigiLocker, AI-powered credit decisioning, and straight-through processing for low-risk applications. Manual intervention should be the exception, not the rule.

2. Comprehensive Loan Management System (LMS)

Post-disbursement, the LMS should manage amortisation schedules, EMI processing, prepayment calculations, penalty management, and borrower communication — all from a single dashboard. Portfolio health metrics should be available in real time.

3. No-Code Business Rule Engine (BRE)

Lending policies are dynamic. A no-code BRE allows credit and operations teams to modify credit policies, approval thresholds, product configurations, and eligibility criteria without raising IT development tickets.

4. 300+ Pre-Integrated APIs

From credit bureaus (CIBIL, Equifax, Experian, CRIF) to KYC providers, bank statement analysers, payment gateways, and insurance partners — the breadth of pre-built integrations determines how quickly an NBFC can go live and how much custom development is avoided.

5. AI-Powered Credit Decisioning

AI-powered platforms evaluate alternative data signals — transaction history, device metadata, behavioural patterns — alongside traditional bureau data to improve approval rates while managing risk.

6. Regulatory Compliance Built In

The platform should auto-generate RBI-mandated reports, support GST-compliant invoicing, maintain a complete audit trail, and incorporate data localisation requirements. Compliance should be a feature, not an afterthought.

7. Collections and Early Warning System

Proactive collections management combined with an early warning system that flags at-risk accounts before they slip into NPA is essential for portfolio quality.

8. Flexible Pricing: Pay-As-You-Use

For NBFCs — especially small and mid-sized ones — capital efficiency is critical. A cloud platform with zero upfront costs and usage-based pricing preserves capital for lending operations rather than technology.

Roopya: India’s Leading Cloud-Based NBFC Software Platform

Roopya (by GeoAlgo Technologies Pvt. Ltd, Gurugram) is built precisely for this moment in Indian lending. It is a no-code, unified cloud lending infrastructure platform that covers the complete lending lifecycle — from application to collections — with AI at its core.

Go Live in 1 Day

Roopya’s plug-and-play infrastructure and streamlined onboarding process allow NBFCs to go live and start processing loans in as little as one day. For an NBFC eager to seize market opportunity, this is transformative.

Truly No-Code Platform

Every element of the lending workflow, from customer journeys to credit policies, can be configured through an intuitive interface. Zero coding is required, which dramatically reduces operating costs and eliminates dependency on scarce technical talent.

300+ Pre-Integrated APIs Ready to Use

Roopya comes with over 300 pre-integrated APIs covering the entire NBFC technology stack:

- Credit bureaus (CIBIL, Equifax, Experian, CRIF High Mark)

- eKYC and eSign providers

- Bank statement analysers

- Payment gateways (NACH, UPI, NEFT)

- GST and ITR verification

- Insurance and co-lending partners

20+ Pre-Configured Loan Products

Roopya ships with more than 20 ready-to-launch loan products, including Personal Loan, Business and SME Loan, Home Loan, Gold Loan, Payday and Salary Advance, Auto and Vehicle Loan, Small Ticket Loan, and Microfinance (MFI) Lending Solutions.

AI-Powered Intelligence Across the Lending Lifecycle

- AI Document Analysis: Advanced OCR and NLP extract, verify, and analyse documents with 99%+ accuracy — detecting fraud and anomalies in seconds.

- Intelligent Credit Decisioning: ML models evaluate thousands of data points including alternative data and behavioural signals to deliver accurate risk assessments in milliseconds.

- AI-Enhanced Business Rule Engine: The BRE learns from historical lending data, suggesting rule improvements and optimising approval logic continuously.

- AI-Driven Analytics and Reporting: Natural language querying lets business users generate complex portfolio reports simply by asking questions in plain English.

The platform’s published outcomes:

- 10x faster loan processing

- 40% better credit scoring accuracy vs traditional methods

- 80% reduction in fraudulent applications

- 60% improvement in collections recovery rates

Cloud NBFC Software vs On-Premise NBFC Software: Direct Comparison

| Parameter | Cloud NBFC Software | On-Premise NBFC Software |

| Deployment Time | 1–7 days | 3–12 months |

| Upfront Cost | Zero / Low | High (hardware + licences) |

| Scalability | Instant, elastic | Constrained by infrastructure |

| Compliance Updates | Automatic | Manual, delayed |

| Maintenance | Managed by vendor | In-house IT team required |

| Disaster Recovery | Built-in, multi-region | Requires separate investment |

| Integration Ecosystem | 300+ pre-built APIs | Custom development needed |

| AI/ML Capabilities | Native, continuously learning | Requires separate platforms |

How Cloud NBFC Software Solves Real Operational Pain Points

Pain Point 1: Slow Loan Processing

Problem: Paper-heavy processes and manual verification slow loan disbursement to days or weeks, resulting in borrower drop-off and competitive disadvantage.

Cloud Solution: Automated KYC, instant bureau checks, and AI-powered decisioning compress the loan journey to minutes. Roopya’s LOS supports straight-through processing for eligible applications with zero human intervention.

Pain Point 2: High Technology Costs

Problem: Building and maintaining an in-house NBFC technology stack is prohibitively expensive, especially for small and mid-sized NBFCs.

Cloud Solution: Roopya’s pay-as-you-use model eliminates capital expenditure on technology. Enterprise-grade lending technology becomes accessible to NBFCs of every size.

Pain Point 3: Regulatory Compliance Burden

Problem: Keeping up with RBI’s evolving digital lending guidelines, Fair Practices Code, KYC norms, and data protection requirements is a significant operational burden.

Cloud Solution: Roopya’s platform is updated continuously to incorporate regulatory changes. Compliance reports are auto-generated and audit trails are maintained automatically.

Pain Point 4: Poor Portfolio Visibility

Problem: Fragmented systems and manual reporting mean portfolio health data is always stale — NBFCs discover problems only after NPAs have formed.

Cloud Solution: Roopya’s real-time analytics dashboard provides instant visibility into portfolio performance, delinquency rates, collection efficiency, and risk concentrations.

Pain Point 5: Collections Inefficiency

Problem: Manual collections processes lead to high NPAs and poor recovery rates, eroding profitability.

Cloud Solution: Roopya’s AI-driven collections engine automates borrower reminders, generates digital payment links, and optimises collection strategies by borrower segment — delivering a 60% improvement in recovery rates.

RBI Regulatory Landscape and Cloud NBFC Software

The Reserve Bank of India has progressively tightened its oversight of digital lending. Key regulatory developments NBFCs must navigate include:

- RBI Digital Lending Guidelines (2022): Mandating disbursement and repayment flows through regulated entity accounts, prohibiting pass-through payment models via LSPs.

- KYC Master Direction: Requiring video KYC (V-CIP), Aadhaar-based eKYC, and ongoing customer due diligence.

- Account Aggregator Framework: Enabling consent-based financial data sharing for credit assessment.

- Fair Practices Code: Governing loan communication, interest rate disclosure, and grievance redressal.

Roopya’s platform ensures compliance with all of the above — with automated audit trails, standardised customer communication templates, regulatory reporting modules, and a built-in grievance management system.