Loan Management System: A Step-by-Step Guide for Banks and NBFCs

The lending landscape in India is undergoing a fundamental transformation. With the Reserve Bank of India (RBI) tightening regulations, borrower expectations at an all-time high, and competition intensifying between banks, NBFCs, and fintech lenders, financial institutions can no longer afford to manage loans through legacy systems or manual processes. A Loan Management System (LMS) is no longer a luxury — it is the operational backbone of every modern lender.

This guide walks banks and NBFCs through everything they need to know about a Loan Management System: what it is, why it matters, what features to look for, how implementation works step by step, and how platforms like Roopya are making world-class LMS technology accessible to lenders of all sizes.

Start Free Trial

What Is a Loan Management System (LMS)?

A Loan Management System is a software platform that manages the complete lifecycle of a loan — from the moment it is disbursed to the day it is fully repaid or written off. Unlike a Loan Origination System (LOS), which focuses on evaluating and approving loan applications, an LMS takes over post-disbursement and handles everything that happens after the money reaches the borrower.

Key functions of an LMS include:

- Account management — tracking outstanding balances, interest accruals, and loan tenure

- EMI scheduling and amortization — generating accurate repayment schedules

- Payment processing — recording and reconciling incoming payments

- Collections management — managing overdue accounts and delinquency

- Customer self-service — enabling borrowers to view statements, download NOCs, and raise service requests

- Regulatory reporting — generating RBI-compliant NPA, ALM, and other regulatory reports

A robust LMS integrates tightly with the LOS and with external systems such as payment gateways, credit bureaus, and accounting platforms, creating a seamless end-to-end lending workflow.

Why Banks and NBFCs Need a Modern LMS

India’s lending sector is one of the fastest-growing in the world. According to RBI data, NBFCs account for a significant share of credit to MSMEs, individuals, and underserved segments. Yet many lenders still operate on spreadsheets or outdated core banking modules that were not designed for the pace and complexity of digital lending.

A modern LMS solves several critical challenges:

1. Operational Efficiency Manual tracking of EMIs, interest calculations, and payment reconciliation is error-prone and expensive. An automated LMS handles these processes in real time, reducing the cost per loan and freeing up staff for higher-value work.

2. Compliance and Regulatory Reporting RBI mandates that NBFCs and banks maintain strict NPA classification, provision accordingly, and submit periodic returns. A compliant LMS automates these calculations and generates audit-ready reports, reducing regulatory risk.

3. Portfolio Visibility Without a centralized LMS, lenders often lack a real-time view of their portfolio health. Modern platforms provide dashboards showing delinquency trends, vintage analysis, collection efficiency, and early warning signals — enabling proactive risk management.

4. Borrower Experience Today’s borrowers expect digital interactions. A good LMS includes a customer portal where borrowers can check their outstanding balance, download statements, pay EMIs online, and request service — reducing inbound calls to the loan servicing team.

5. Scalability Whether a lender is disbursing 100 loans a month or 100,000, a cloud-native LMS scales automatically without requiring infrastructure upgrades.

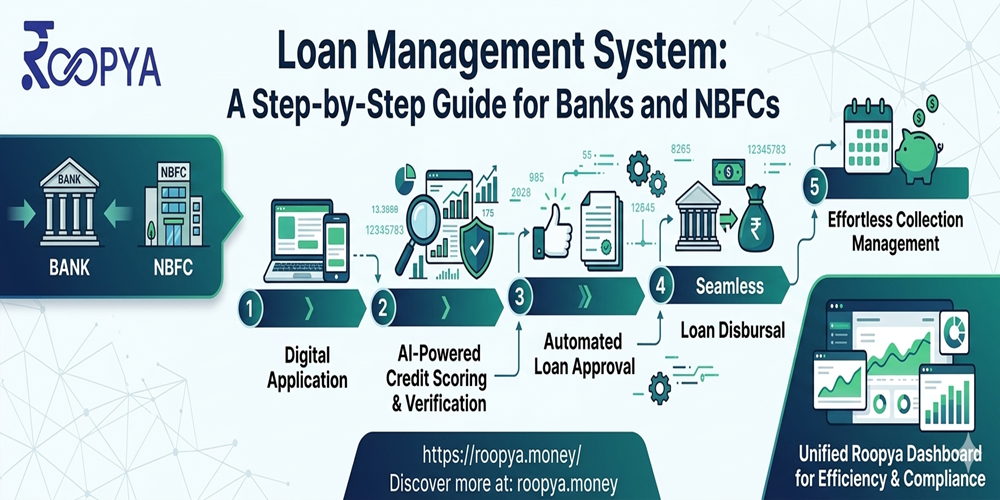

Step-by-Step Guide to Implementing a Loan Management System

Implementing an LMS is one of the most important technology decisions a financial institution will make. Here is a practical, step-by-step breakdown of how lenders can approach this process.

Step 1: Define Your Requirements

Before evaluating any platform, your team must clearly define what you need. Consider:

- Loan products: Personal loans, business loans, gold loans, home loans, microfinance — each product has unique amortization, fee, and documentation requirements.

- Scale: How many active loan accounts do you have or plan to have?

- Regulatory requirements: Are you an RBI-registered NBFC, a scheduled commercial bank, or a microfinance institution? Your compliance requirements will differ.

- Integration needs: Which payment gateways, credit bureaus, core banking systems, and accounting platforms do you already use?

- Team capabilities: Do you have an in-house IT team, or do you need a no-code platform that business users can manage?

Document these requirements in a detailed Request for Proposal (RFP) to compare vendors systematically.

Step 2: Evaluate and Select an LMS Platform

When evaluating platforms, look for these critical capabilities:

Loan Lifecycle Management The system must handle the complete loan account lifecycle — from account creation at disbursement through EMI collections, prepayments, foreclosures, restructuring, and write-offs.

Payment Processing and Reconciliation The LMS must integrate with NACH/eNACH for auto-debit, support multiple payment gateways (Razorpay, PayU, NPCI UPI), and automatically reconcile incoming payments with the correct loan accounts.

Collections and Delinquency Management Look for built-in collection workflows, automated SMS/WhatsApp/email reminders, DPD (Days Past Due) bucket management, and agent assignment tools.

Regulatory Compliance The platform must support RBI-mandated NPA classification, provision calculations (as per Ind AS 109 / IRAC norms), GST and TDS calculations, credit bureau reporting, and ALM reports.

Integration and APIs A good LMS offers pre-built integrations with major credit bureaus (CIBIL, Experian, Equifax, CRIF), KYC providers (DigiLocker, UIDAI), accounting systems (Tally, SAP), and communication gateways.

Security and Data Privacy The platform must offer data encryption at rest and in transit, role-based access control, multi-factor authentication, and compliance with India’s data protection framework.

Platforms like Roopya (roopya.money/loan-management-system) offer a no-code, AI-first LMS that covers all of the above with 300+ pre-integrated APIs and a go-live time of as little as 5–7 days.

Step 3: Sign Up and Account Setup (Day 1)

With a modern cloud-native LMS, onboarding has been dramatically simplified. On Roopya, the process begins with a single online registration — entity verification, license and compliance checks, and provisioning of a sandbox environment can be completed within 2–4 hours.

During this phase:

- Your organization’s details and regulatory credentials are verified

- A dedicated implementation manager is assigned

- Sandbox credentials are issued so your team can begin exploring the platform immediately

Step 4: Product and Workflow Configuration (Days 2–3)

This is where the LMS is customized to reflect your lending business. Key configuration tasks include:

- Loan product setup: Define interest rate types (flat, reducing balance), processing fees, prepayment charges, penal interest rates, and loan tenures for each product

- Amortization schedules: Configure how EMIs are calculated and how payments are applied (principal vs. interest priority)

- Approval hierarchies and workflows: Set up the chain of approval for loan account changes such as restructuring, top-ups, or write-offs

- Document checklists: Define what post-disbursement documents must be maintained per loan product

- User roles and permissions: Configure role-based access so relationship managers, credit officers, collections agents, and senior management each see only what they need

- Communication templates: Set up automated SMS, email, and WhatsApp messages for EMI reminders, payment confirmations, overdue alerts, and NOC issuance

- Branding: Apply your logo, color scheme, and branding to the customer portal

On a no-code platform, all of this is done through intuitive visual interfaces — no programming required.

Step 5: Integration Setup (Days 3–4)

Once the LMS is configured, integrations with external systems are activated:

- Payment gateways: Connect Razorpay, PayU, CCAvenue, or your preferred gateway for online EMI payments

- NACH/eNACH: Set up auto-debit mandates for recurring EMI collection

- Credit bureaus: Enable automatic credit bureau reporting for NPA accounts (required by RBI)

- KYC providers: Connect DigiLocker and UIDAI for ongoing KYC refresh requirements

- Accounting systems: Integrate with Tally, SAP, or Oracle for automated bookkeeping entries on disbursements, repayments, and provisions

- SMS/WhatsApp/Email gateways: Activate communication channels for borrower notifications

With 300+ pre-built integrations available on platforms like Roopya, this step that used to take months now takes just 1–2 days.

Step 6: Team Training and User Acceptance Testing (Days 4–5)

Before going live, your team must be trained and the system must be tested end-to-end.

Training sessions should cover:

- Loan account creation and disbursement recording

- Payment processing and manual payment entry

- Running amortization schedules and generating statements

- Collections workflow — assigning agents, recording promises to pay, escalating overdue accounts

- Generating regulatory reports

User Acceptance Testing (UAT) should simulate real loan scenarios:

- Process a fresh disbursement and verify the EMI schedule

- Record a payment and verify the outstanding balance is updated correctly

- Simulate a prepayment and verify the revised schedule

- Test an overdue scenario and confirm the correct DPD bucket classification

- Generate an NPA report and verify accuracy

Document all test results and resolve any discrepancies before proceeding to production.

Step 7: Data Migration (if applicable)

If you are migrating from an existing LMS or manual system, data migration must be handled carefully. This involves:

- Extracting historical loan data (account numbers, outstanding balances, EMI schedules, payment history, DPD status)

- Mapping data fields to the new LMS schema

- Validating data integrity after migration

- Running parallel systems briefly to verify output consistency

Reputable LMS vendors provide dedicated data migration support and zero-downtime migration tools to ensure business continuity.

Step 8: Go-Live and Continuous Monitoring (Days 5–7)

With configuration complete, integrations tested, team trained, and data migrated, you are ready to go live. The go-live process includes:

- Final security checks and pen testing

- Production environment provisioning

- Switching payment gateway and NACH integrations to production credentials

- Activating live customer portal access

Post-launch, the first week should be supported by dedicated technical resources monitoring system performance, payment reconciliation accuracy, and collection workflow execution.

Key Features to Look for in an LMS in 2025–2026

As the lending technology landscape evolves, here are the capabilities that separate best-in-class platforms from legacy systems:

AI-Powered Collections: Machine learning models analyze borrower behavior to predict default probability and recommend the optimal collection strategy — call timing, channel preference, payment plan — for each account.

Early Warning System: Proactive alerts based on behavioral signals (irregular payment patterns, increased utilization) allow lenders to intervene before an account becomes NPA.

No-Code Business Rule Engine: Lenders need to change interest rates, fee structures, and credit policies frequently. A no-code BRE lets business teams make these changes without waiting for IT.

Cloud-Native Architecture: Ensures 99.9% uptime, automatic scaling during peak disbursement periods, and enterprise-grade security without on-premise infrastructure costs.

Embedded Analytics: Built-in dashboards for portfolio health, vintage analysis, cohort tracking, and collection efficiency eliminate the need for separate BI tools.

How Roopya’s LMS Helps Banks and NBFCs

Roopya (roopya.money) is one of India’s leading digital lending platforms, offering a no-code, AI-first, cloud-native LMS built specifically for modern lenders. Key advantages include:

- Go-live in 5–7 days with a streamlined onboarding process

- 300+ pre-integrated APIs covering credit bureaus, payment gateways, KYC providers, and accounting systems

- AI-powered credit decisioning and fraud detection with 99%+ accuracy

- Fully compliant with RBI regulations including NPA classification, ALM reporting, and credit bureau reporting

- Zero upfront cost with a pay-as-you-use pricing model

- 24/7 support with a dedicated implementation manager

- Multi-product support — personal loans, business loans, gold loans, home loans, auto loans, and more

Whether you are an established NBFC looking to modernize your loan servicing operations or a new-age digital lender preparing to launch, Roopya provides the technology infrastructure to scale efficiently and compliantly.

A Loan Management System is the operational core of any lending institution. Choosing the right platform, configuring it correctly, and integrating it with your existing ecosystem can mean the difference between a loan book that grows profitably and one that is plagued by operational inefficiencies, compliance gaps, and poor borrower experience.

The step-by-step implementation approach outlined in this guide — from requirements definition through go-live and monitoring — gives banks and NBFCs a clear roadmap to modernize their loan management operations. With platforms like Roopya reducing go-live timelines to under a week and eliminating the need for large IT investments, there has never been a better time to upgrade your lending infrastructure.

Ready to transform your lending operations? Request a Demo with Roopya today.