The Complete Guide to Digital Lending Software Platforms

The financial services industry is experiencing one of the biggest technological transformations in history. Traditional lending processes that once relied on paperwork, manual verification, branch visits, and lengthy approval cycles are rapidly being replaced by digital lending software platforms.

Today’s borrowers expect instant loan approvals, seamless online applications, real-time status updates, and paperless experiences. At the same time, lenders need faster underwriting, improved compliance, lower operational costs, and better risk management.

This is where Digital Lending Software Platforms play a crucial role.

A digital lending platform enables banks, NBFCs, fintech companies, credit unions, microfinance institutions, and online lenders to automate the complete lending lifecycle—from customer onboarding and KYC verification to underwriting, loan approval, disbursement, repayment tracking, and collections. Modern platforms increasingly use cloud-native infrastructure, automation, AI-based decisioning, digital workflows, and integrated analytics to accelerate lending operations.

Start Free Trial

In this comprehensive guide, we’ll explore everything you need to know about digital lending software platforms and how they are revolutionizing the lending industry.

What is a Digital Lending Software Platform?

A Digital Lending Software Platform is an end-to-end technology solution that automates and manages the entire loan lifecycle.

It allows financial institutions to:

- Capture loan applications online

- Verify borrower identity

- Perform digital KYC

- Collect and validate documents

- Conduct credit assessments

- Automate underwriting

- Approve or reject applications

- Generate loan agreements

- Process disbursements

- Manage repayments

- Track collections

- Monitor loan portfolios

Instead of managing multiple systems, lenders can centralize their operations using a single platform. Modern lending platforms often combine Loan Origination Systems (LOS), Loan Management Systems (LMS), decision engines, analytics, and compliance tools into one integrated ecosystem.

Why Traditional Lending Processes Are No Longer Effective

Traditional lending operations face several challenges:

Slow Processing

Manual loan approvals can take days or weeks.

High Operational Costs

Paper-based processes require larger teams and increased administrative expenses.

Increased Human Errors

Manual data entry often results in mistakes and compliance risks.

Poor Customer Experience

Borrowers expect digital-first experiences and instant responses.

Compliance Challenges

Keeping up with regulatory requirements becomes difficult without automation.

Limited Scalability

Growing loan volumes become difficult to manage manually.

Digital lending software eliminates these challenges through intelligent automation and workflow management.

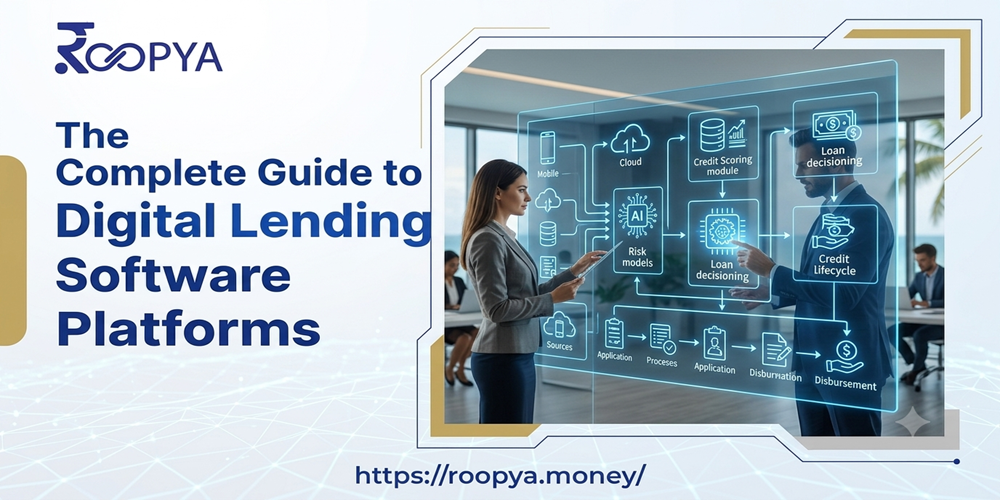

How Digital Lending Platforms Work

A digital lending platform typically follows the following workflow:

1. Digital Borrower Onboarding

Customers submit loan applications through:

- Website forms

- Mobile apps

- Partner portals

- Agent channels

The platform collects:

- Personal information

- Employment details

- Financial information

- Loan requirements

2. Automated KYC Verification

Integrated KYC services verify:

- Aadhaar

- PAN

- Mobile number

- Bank account

- Address proof

Automation significantly reduces onboarding time and manual verification efforts.

3. Document Collection and Verification

The system automatically collects:

- Salary slips

- Bank statements

- Income tax returns

- Identity documents

- Business documents

OCR technology extracts and validates information automatically.

4. Credit Assessment

The platform retrieves data from:

- Credit bureaus

- Banking systems

- Internal scorecards

- Alternative data sources

This enables faster risk assessment and eligibility checks.

5. Automated Underwriting

Modern platforms use:

- Business Rule Engines (BRE)

- AI-based scoring

- Risk analytics

- Fraud detection

Applications are automatically evaluated based on lender-defined rules.

6. Loan Approval

The decision engine determines:

- Approved amount

- Interest rate

- Loan tenure

- Risk category

This reduces manual intervention and improves turnaround time.

7. Digital Disbursement

Approved loans are disbursed electronically through integrated payment systems.

8. Loan Servicing and Collections

The platform manages:

- EMI schedules

- Payment tracking

- Collection workflows

- Customer communications

- Delinquency monitoring

This creates a complete end-to-end lending ecosystem.

Key Features of a Modern Digital Lending Platform

Digital Customer Onboarding

- Online applications

- Mobile onboarding

- Self-service portals

- Multi-channel lead capture

AI-Powered Underwriting

Artificial Intelligence helps lenders:

- Evaluate risks

- Detect fraud

- Predict defaults

- Improve approval accuracy

AI-based automation is becoming a major differentiator in modern lending platforms.

Loan Origination System (LOS)

An LOS automates:

- Lead management

- Application processing

- Credit assessment

- Approval workflows

- Disbursement management

Loan Management System (LMS)

An LMS manages:

- EMI schedules

- Repayment tracking

- Customer servicing

- Collections

Workflow Automation

Automation eliminates repetitive tasks such as:

- Document requests

- Follow-ups

- Notifications

- Status updates

Document Management

Centralized storage for:

- Loan files

- Agreements

- KYC records

- Compliance documents

Analytics and Reporting

Real-time dashboards provide insights into:

- Approval rates

- Loan performance

- Risk exposure

- Portfolio growth

Benefits of Digital Lending Software Platforms

Faster Loan Approvals

Automation reduces processing time from days to minutes. Digital platforms are designed to streamline onboarding, decisioning, and approvals through integrated workflows and automation.

Improved Customer Experience

Borrowers enjoy:

- Instant applications

- Faster approvals

- Real-time tracking

- Paperless processes

Reduced Operational Costs

Automation lowers:

- Staffing costs

- Processing expenses

- Administrative overhead

Better Compliance

Automated compliance checks reduce regulatory risks.

Improved Risk Management

AI and analytics improve lending decisions.

Increased Scalability

Cloud-based infrastructure supports business growth.

Higher Conversion Rates

Faster processing leads to improved customer acquisition.

Digital Lending Software for NBFCs

NBFCs require flexible lending solutions for:

- Personal Loans

- Business Loans

- MSME Loans

- Vehicle Loans

- Gold Loans

- Consumer Loans

A digital lending platform helps NBFCs:

- Reduce TAT

- Improve collections

- Scale operations

- Lower NPAs

Roopya provides configurable workflows and cloud-based infrastructure designed for NBFCs and fintech lenders.

Digital Lending Software for Banks

Banks can use lending platforms to:

- Digitize loan operations

- Improve compliance

- Enhance customer experience

- Automate underwriting

Benefits include:

- Branch digitization

- Faster approvals

- Reduced paperwork

- Improved portfolio monitoring

Digital Lending Software for Fintech Companies

Fintech lenders require:

- API integrations

- Real-time decisioning

- Mobile-first experiences

- Automated workflows

Modern lending platforms support:

- Open APIs

- Bureau integrations

- Payment gateway integrations

- AI decision engines

These capabilities enable fintechs to launch and scale lending products more quickly.

Cloud-Based vs On-Premise Lending Platforms

| Feature | Cloud-Based | On-Premise |

|---|---|---|

| Deployment | Fast | Slow |

| Cost | Lower | Higher |

| Scalability | Excellent | Limited |

| Maintenance | Vendor Managed | Internal Team |

| Security Updates | Automatic | Manual |

| Accessibility | Anywhere | Office Network |

Cloud-native lending platforms are increasingly preferred because they offer rapid deployment, scalability, and lower infrastructure costs.

Emerging Trends in Digital Lending

AI-Based Credit Decisioning

Artificial intelligence is transforming underwriting and fraud detection.

Alternative Credit Scoring

Lenders increasingly evaluate:

- Banking behavior

- Transaction data

- Alternative financial signals

Embedded Finance

Loans are becoming available directly within apps and digital ecosystems.

Open Banking

API-driven banking integrations enable richer financial insights.

Real-Time Lending

Borrowers increasingly expect approvals within minutes.

Industry discussions highlight that achieving speed while maintaining compliance and risk controls requires strong architecture, automated decisioning, and ongoing risk monitoring.

Why Choose Roopya Digital Lending Software Platform?

Roopya offers a comprehensive digital lending ecosystem that helps lenders automate and scale operations.

Key capabilities include:

- Digital borrower onboarding

- Loan Origination System (LOS)

- Loan Management System (LMS)

- Automated underwriting

- Business Rule Engine

- Credit bureau integrations

- AI-powered analytics

- Document management

- Workflow automation

- Compliance management

- Collections management

- Cloud-native infrastructure

The platform supports NBFCs, banks, MFIs, and fintech companies looking to modernize their lending operations.

Digital Lending Software Platforms have become essential for modern financial institutions. They streamline loan origination, automate underwriting, improve compliance, reduce costs, and deliver superior borrower experiences.

As lending continues to evolve, organizations that embrace automation, AI, cloud technology, and data-driven decision-making will gain a significant competitive advantage.

Whether you are an NBFC, bank, fintech startup, or microfinance institution, investing in a modern digital lending platform like Roopya can accelerate growth, improve operational efficiency, and transform the way you serve borrowers.