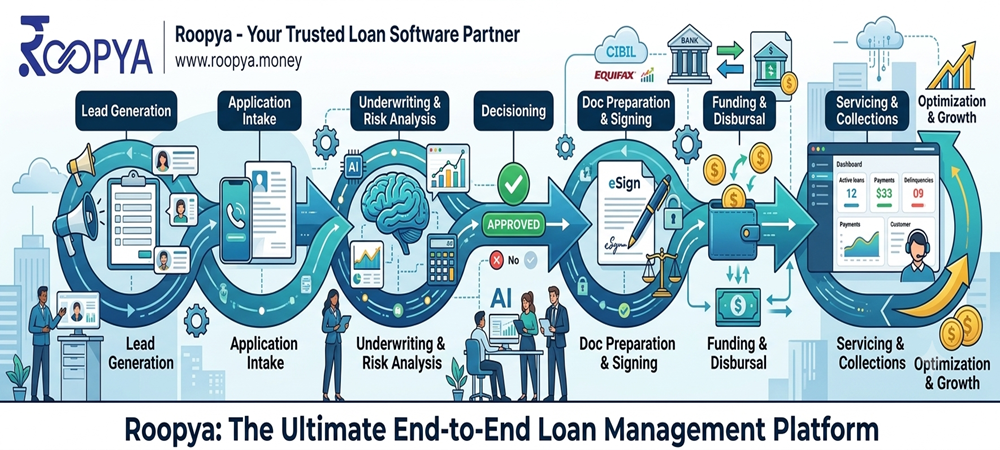

End-to-End Loan Management Software Platform: Power Your Entire Lending Lifecycle with Roopya

In today’s fast-evolving financial landscape, lenders — from NBFCs and banks to microfinance institutions and digital lending startups — need more than just a basic loan processing tool. They need an intelligent, integrated, and scalable infrastructure that handles every step of the lending journey without friction. That is exactly what Roopya’s end-to-end loan management software platform delivers.

Roopya is built for modern lenders who want to move fast, stay compliant, and scale confidently. Whether you are originating your first loan or managing a portfolio of thousands, Roopya gives you the complete technology backbone to do it all — without writing a single line of code.

Start Free Trial

What Is an End-to-End Loan Management Software Platform?

An end-to-end loan management software platform is a unified digital infrastructure that covers the complete lifecycle of a loan — from the moment a borrower applies to the moment the loan is fully repaid or written off. Unlike standalone tools that only address one part of the journey, a true end-to-end platform connects every stage seamlessly.

For lenders, this means eliminating data silos, reducing manual handoffs, and gaining a single source of truth across origination, underwriting, disbursement, servicing, collections, and reporting. For borrowers, it means a faster, more transparent, and more satisfying credit experience.

Roopya’s platform is designed precisely around this philosophy — one unified system, zero redundancy, total visibility.

The Core Modules of Roopya’s Loan Management Platform

1. Loan Origination System (LOS)

The lending journey begins the moment a borrower expresses interest. Roopya’s Loan Origination System ensures this first impression is seamless and professional. It handles digital application forms, document collection, KYC verification, bureau checks, and credit assessment — all within a single, automated workflow.

Key capabilities of the LOS include:

- Digital Application Forms: Configurable, mobile-friendly application interfaces that capture borrower data accurately and quickly. Lenders can customize forms for different loan products without any technical help.

- Automated Credit Scoring: Integrated with 300+ APIs including credit bureaus like CIBIL, Experian, and CRIF, the platform pulls real-time credit data and runs it through configurable scoring models to produce instant credit decisions.

- Document Verification: AI-powered OCR and NLP extract and verify information from identity documents, bank statements, salary slips, and business financials with over 99% accuracy.

- Real-Time Decisioning: Rules-based and ML-driven decisioning engines evaluate applications in milliseconds, reducing turnaround time from days to minutes.

The LOS is not just about speed — it is about precision. Every application that enters the pipeline is screened, scored, and processed with consistent logic, eliminating human bias and reducing error rates.

2. Loan Management System (LMS)

Once a loan is disbursed, the work is far from over. The Loan Management System is the operational heart of the platform, ensuring that every active loan is tracked, serviced, and managed throughout its life.

Roopya’s LMS provides:

- Portfolio Management: A real-time dashboard that gives lenders complete visibility into their entire loan book — outstanding principal, interest accruals, overdue amounts, repayment trends, and risk concentrations.

- Automated Payment Processing: Integration with payment gateways and NACH mandates ensures that EMI collections are automated, reconciled, and recorded without manual intervention.

- Dynamic Amortization Schedules: The system automatically generates accurate repayment schedules for every loan product — whether flat rate, reducing balance, bullet repayment, or custom structures.

- Customer Portal: Borrowers get access to a self-service portal where they can view their loan details, download statements, make payments, and raise service requests — reducing the load on lender support teams.

The LMS is the foundation of healthy loan servicing. By automating routine tasks and surfacing exceptions, it allows lender teams to focus on high-value decisions rather than administrative work.

3. Collections Management System

For lenders, collections are often the most challenging part of the lending lifecycle. Roopya’s Collections System transforms this challenge into a structured, data-driven process.

The collections module includes:

- Automated Reminders: SMS, email, and WhatsApp reminders are triggered automatically based on due dates, overdue buckets, and borrower behavior — reducing missed payments before they become defaults.

- Intelligent Collection Workflows: Rule-based and AI-driven workflows assign delinquent accounts to the right collection strategy at the right time — reducing recovery costs and improving resolution rates.

- Flexible Payment Plans: Collections agents can offer borrowers restructured repayment plans, moratoriums, or partial settlements — all configurable within the platform with full audit trails.

- Agent Management: The platform provides a complete agent productivity suite with case assignment, call disposition tracking, and performance dashboards.

Roopya’s collections system does not treat every delinquent borrower the same. It segments borrowers by risk profile, payment history, and behavioral signals to deploy the most effective intervention — humanizing collections while maximizing recovery.

4. Early Warning System (EWS)

Prevention is always better than cure. Roopya’s Early Warning System identifies loans that are showing signs of stress before they slip into delinquency — giving lenders the time to intervene proactively.

The EWS monitors:

- Changes in repayment behavior such as late payments, partial payments, or bounced mandates

- Shifts in bureau data indicating increased borrower indebtedness

- Business or income deterioration signals from alternative data sources

- Portfolio-level concentration risks and sector-specific trends

When warning signals are detected, the system triggers configurable alert workflows — notifying relationship managers, flagging accounts for review, or initiating proactive borrower outreach. This predictive capability can reduce NPA formation significantly and protect portfolio quality.

5. Lending Analytics and Reporting

Data is the lifeblood of a modern lending business. Roopya’s embedded analytics engine transforms raw operational data into actionable intelligence — helping lenders optimize pricing, refine credit policy, monitor portfolio health, and meet regulatory reporting requirements.

The analytics and reporting module delivers:

- Portfolio Analytics: Deep dives into book composition, vintage analysis, delinquency trends, and sector exposure — enabling portfolio managers to make informed decisions.

- Performance Metrics: Real-time KPIs for every stage of the lending funnel, from application volumes and approval rates to disbursement timelines and NPA ratios.

- Regulatory Reporting: Pre-built report templates for RBI submissions, NHB compliance, and other statutory requirements — reducing the burden of manual report preparation.

- Custom Dashboards: Role-based dashboards for CXOs, credit managers, operations teams, and collections supervisors — each surfacing the metrics most relevant to their function.

- Export Capabilities: Reports can be scheduled, exported in multiple formats, and distributed automatically to relevant stakeholders.

Why Roopya Stands Apart from Traditional Loan Management Software

The Indian lending software market has several legacy solutions built on outdated architectures. These platforms are often difficult to configure, expensive to integrate, and slow to update. Roopya was built from the ground up as a cloud-native, API-first, no-code platform — and the difference is visible from day one.

Go Live in 1 Day

Most enterprise lending software implementations take months. Roopya’s streamlined onboarding, pre-configured loan products, and plug-and-play infrastructure mean you can be processing loans within 24 hours of signing up. This is not a marketing claim — it is the reality experienced by lenders across India who have launched on Roopya.

Truly No-Code Configuration

Business users — not just IT teams — can configure loan products, credit policies, approval workflows, interest calculations, and collection rules through Roopya’s intuitive visual interface. No coding. No vendor dependency. No change-request queues.

300+ Pre-Integrated APIs

Roopya comes with pre-built integrations with credit bureaus, KYC providers, bank statement analyzers, payment gateways, e-sign platforms, telecom verification services, and more. This ecosystem of 300+ ready-to-use APIs eliminates the integration burden that consumes months in traditional implementations.

Pay-As-You-Use Pricing

Unlike legacy software that demands large upfront license fees, Roopya operates on a flexible, consumption-based pricing model. Lenders pay for what they actually use — making the platform accessible for early-stage NBFCs and scalable for large financial institutions alike.

Always Compliant

The regulatory landscape for lending in India is dynamic. RBI guidelines, FLDG norms, co-lending regulations, and data localization requirements evolve continuously. Roopya’s compliance team monitors regulatory changes and updates the platform proactively — so lenders are always on the right side of the law without additional effort.

AI-Powered Intelligence at Every Stage

Roopya is not just an automation platform — it is an intelligent one. Artificial intelligence and machine learning are embedded across the entire loan management lifecycle.

- AI Document Analysis processes identity proofs, bank statements, and financial documents in seconds with 99%+ accuracy, flagging anomalies and potential fraud instantly.

- AI Credit Decisioning evaluates alternative data signals — including mobile usage patterns, utility payment history, and GST returns — alongside traditional bureau data to build a richer picture of borrower creditworthiness.

- AI Business Rule Engine learns from historical approval and rejection patterns to suggest rule optimizations — helping lenders continuously improve their credit policy without manual trial-and-error.

- AI-Driven Collections analyzes borrower behavior to predict optimal contact windows, messaging, and recovery strategies — improving collection efficiency by up to 60%.

- Natural Language Reporting allows managers to ask questions in plain English and receive instant analytical responses — democratizing data access across the organization.

The result is a platform that not only automates the lending lifecycle but makes it smarter with every transaction.

Who Is Roopya Built For?

Roopya’s end-to-end loan management software platform is designed for a broad spectrum of lending institutions:

- NBFCs looking to digitize operations, reduce TAT, and scale their loan book without proportional headcount growth

- Banks and SFBs seeking a modern digital lending layer on top of their core banking infrastructure

- Microfinance Institutions (MFIs) managing high-volume, small-ticket loans with complex repayment structures

- Digital Lending Startups that want to launch fast with a production-grade platform and iterate as they grow

- Loan Service Providers (LSPs) and business correspondents that originate and service loans on behalf of regulated entities

- Co-lending platforms that need to coordinate origination, servicing, and collections between two or more lenders

Regardless of size, geography, or loan product type, Roopya provides the infrastructure to lend with confidence.

20+ Pre-Configured Loan Products Ready to Launch

Roopya comes with more than 20 pre-configured loan product templates, covering the most common lending categories in India. These include:

- Personal Loans

- Business Loans and SME Credit

- Payday and Salary Advance Loans

- Gold Loans

- Home Loans

- Vehicle and Auto Loans

- Agriculture and Kisan Loans

- Education Loans

- Loan Against Property (LAP)

- Microfinance and Group Loans

Each product template comes with pre-set workflows, document checklists, repayment structures, and reporting configurations. Lenders can launch with a template and customize it to their exact requirements — dramatically compressing time to market.

Security, Reliability, and Data Privacy

Roopya is built on enterprise-grade cloud infrastructure with end-to-end encryption, role-based access controls, multi-factor authentication, and comprehensive audit logging. The platform complies with India’s data privacy regulations and follows RBI guidelines on data localization and cybersecurity.

Uptime SLAs, disaster recovery protocols, and regular penetration testing ensure that lenders can rely on Roopya as their mission-critical lending infrastructure — 24 hours a day, 365 days a year.

Getting Started with Roopya

Transitioning to Roopya’s end-to-end loan management software platform is straightforward. A dedicated onboarding team guides you through product configuration, API integration, team training, and go-live readiness — typically completing the entire process within one business day for standard implementations.

Roopya offers a free demo where prospective lenders can see the platform in action, ask questions specific to their business model, and assess fit before making any commitment.