Automated Loan Management Software: The Complete Guide for Modern Lenders

The lending landscape in India is undergoing a seismic transformation. With the rise of NBFCs, fintech lenders, and digital-first banks, the demand for intelligent, scalable, and automated loan management software has never been greater. Manual processes, siloed systems, and paper-based workflows are no longer just inconvenient — they are existential threats to any lender that wants to stay competitive.

Roopya’s Automated Loan Management Software is purpose-built to solve exactly this problem. Designed for modern financial institutions — from NBFCs and MFIs to banks and loan service providers — Roopya delivers an end-to-end digital lending infrastructure that automates the entire loan lifecycle, from origination to collections, without requiring a single line of code.

In this guide, we cover everything you need to know about automated loan management software: what it is, how it works, why it matters, and how Roopya stands apart as India’s most advanced no-code lending platform.

Start Free Trial

What is Automated Loan Management Software?

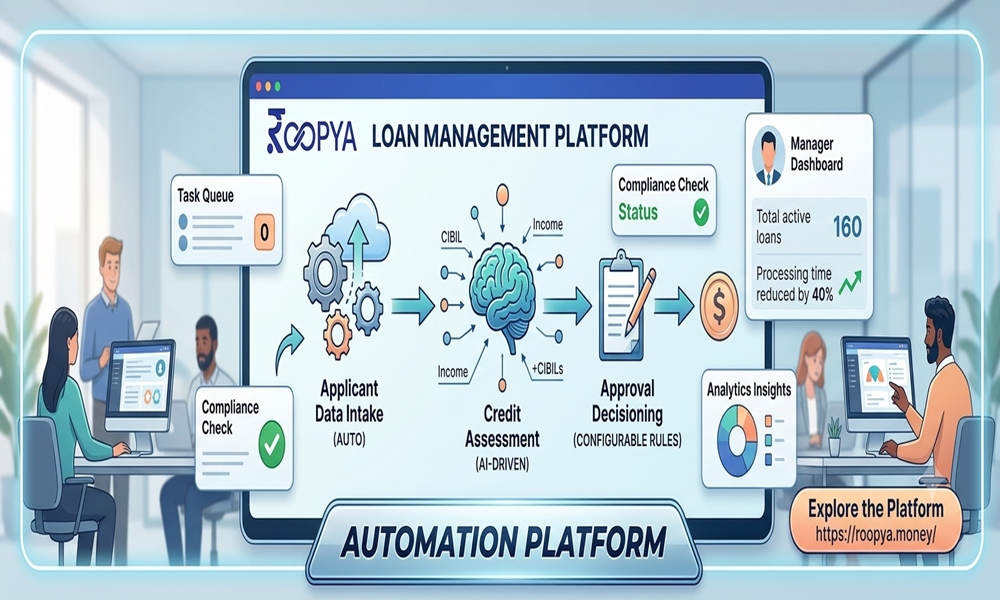

Automated loan management software (LMS) is a technology platform that digitizes and automates the complete lifecycle of a loan — from application intake and credit decisioning through disbursement, repayment tracking, collections, and reporting. Unlike traditional loan management tools that automate only fragments of the process, a true automated LMS integrates every stage into a single, unified platform.

At its core, an automated LMS replaces manual, error-prone tasks with rule-driven workflows, AI-powered decisioning, and real-time data processing. This means lenders can process higher loan volumes with fewer staff, reduce operational errors, maintain regulatory compliance, and deliver a superior borrower experience — all simultaneously.

Key Functions of an Automated Loan Management System:

- Automated loan application intake and document collection

- AI-powered credit scoring and risk assessment

- Rule-based approval and rejection workflows

- Automated disbursement processing

- Repayment scheduling and EMI tracking

- Delinquency monitoring and collections automation

- Regulatory reporting and compliance management

- Portfolio analytics and performance dashboards

Modern lenders recognize that these functions cannot be treated in isolation. An automated LMS that connects all these stages — sharing data, triggering actions, and learning from outcomes — is what transforms a lending business from reactive to proactive.

Why Manual Loan Management is Holding Your Business Back

Before exploring what automated loan management software offers, it is important to understand the cost of not having one. Across India, thousands of NBFCs, MFIs, and small banks still rely on spreadsheets, physical files, or disconnected legacy systems to manage their loan portfolios. The consequences are severe and compounding.

The Hidden Costs of Manual Loan Management:

Operational Inefficiency

Loan officers spend hours each day on data entry, document chasing, and status updates that could be automated. This reduces the time available for high-value activities like relationship building and portfolio strategy. A single loan that takes days to process manually can be completed in minutes with the right software.

High Error Rates

Manual data entry introduces mistakes in repayment schedules, interest calculations, and customer records. Even a small arithmetic error in an amortization schedule can lead to disputes, regulatory penalties, and borrower dissatisfaction. Automated systems apply rules consistently and flawlessly, every single time.

Delayed Decisions

When credit assessment depends on human review of documents, bank statements, and credit bureau reports, approval timelines stretch from days to weeks. In today’s competitive market, borrowers simply move on to faster lenders. Automated credit decisioning reduces approval times from days to seconds.

Poor Compliance Management

RBI guidelines, Fair Practices Code, KYC requirements, and other regulatory mandates are constantly evolving. Manual tracking of compliance obligations is error-prone and puts institutions at risk of penalties. An automated LMS updates compliance rules systematically and maintains audit trails automatically.

Inadequate Portfolio Visibility

Without real-time dashboards and analytics, lenders often discover portfolio problems — rising NPAs, concentration risk, collection failures — only after they become serious. Automated LMS platforms provide early warning signals and predictive insights that allow proactive intervention.

Core Modules of Roopya’s Automated Loan Management Software

Roopya has architected its platform around the complete lending lifecycle. Each module is deeply integrated with the others, ensuring seamless data flow and unified customer records across every stage.

3.1 Loan Origination System (LOS)

The journey begins before a loan is even created. Roopya’s Loan Origination System handles the entire pre-disbursement process with zero manual intervention. Borrowers complete digital application forms on any device. Documents are submitted, verified, and analyzed automatically using AI-powered OCR. Credit bureau data is fetched in real time. Risk scores are computed instantly. The Business Rule Engine evaluates the application against the lender’s credit policy and produces an approval, rejection, or referral decision — all within seconds.

- Digital application forms with conditional logic

- Automated KYC and document verification

- Real-time bureau pulls from CIBIL, Experian, CRIF, and Equifax

- AI-powered income and bank statement analysis

- Configurable credit policy rules with no-code BRE

- Instant decisioning with explainable outcomes

3.2 Loan Management System (LMS)

Once a loan is disbursed, the Loan Management System takes over to handle every aspect of the ongoing loan relationship. This is where automation delivers its most immediate value. Repayment schedules are generated automatically based on the loan product’s parameters. EMI reminders are sent via SMS, WhatsApp, and email at pre-configured intervals. Payment reconciliation happens in real time. Interest accrual, principal reduction, and balance updates occur automatically with every transaction.

- Automated amortization schedule generation

- Multi-channel payment processing integration

- Real-time payment reconciliation and ledger updates

- Prepayment and part-payment handling

- EMI restructuring and moratorium management

- Customer self-service portal for statement access

3.3 Collections Management System

Loan delinquency is inevitable in any portfolio. What separates great lenders from struggling ones is how efficiently and empathetically they manage collections. Roopya’s Collections Management System automates the entire delinquency resolution process. As soon as a payment is missed, the system triggers a configurable escalation workflow — starting with soft reminders and progressively escalating to field agent assignment, legal notice generation, or external collection agency handover.

- Automated DPD (Days Past Due) tracking and classification

- Rule-based escalation workflows by DPD bucket

- Multi-channel automated reminders (SMS, WhatsApp, IVR, email)

- Field agent assignment and visit tracking

- Settlement offer management and payment plan creation

- NPA classification and provisioning automation

3.4 Early Warning System (EWS)

The most powerful form of collections management is preventing delinquency before it occurs. Roopya’s Early Warning System uses behavioral analytics and predictive models to identify borrowers at risk of default weeks before a payment is actually missed. Portfolio managers receive alerts segmented by risk severity, enabling targeted interventions that save both the borrower relationship and the lender’s NPA ratio.

- Predictive default risk scoring on active accounts

- Behavioral pattern analysis across transaction data

- Configurable risk alert thresholds and notifications

- Intervention workflow triggers based on risk signals

- Portfolio-level risk heatmaps and concentration analysis

3.5 Lending Analytics and Reporting

Data is the most valuable asset in lending. Roopya’s integrated analytics layer transforms raw operational data into actionable business intelligence. Lenders can track portfolio performance, monitor collection efficiency, analyze product profitability, and identify credit risk trends — all from a single dashboard. Regulatory reports can be generated and exported with a single click, reducing compliance overhead by hours each week.

- Real-time portfolio performance dashboards

- Product-level and segment-level profitability analysis

- Collection efficiency metrics by agent, channel, and bucket

- Regulatory report generation for RBI submissions

- Customizable reports with scheduled email delivery

- Natural language query interface for ad-hoc analysis

AI-Powered Features That Set Roopya Apart

What separates Roopya from conventional loan management software is its deep integration of artificial intelligence across the entire lending lifecycle. AI is not a bolt-on feature at Roopya — it is embedded in the core architecture of the platform.

AI-Powered Document Analysis

Roopya’s document intelligence engine uses advanced OCR and NLP to extract, validate, and cross-verify information from identity documents, income proofs, bank statements, and property documents with over 99% accuracy. What previously required manual review by trained staff is now completed in seconds, with built-in fraud detection to flag anomalies instantly.

Machine Learning Credit Scoring

Traditional credit scores based solely on bureau data miss a significant portion of creditworthy borrowers, particularly in the underserved segments that NBFCs and MFIs exist to serve. Roopya’s ML-powered credit scoring models analyze thousands of data points — transaction patterns, repayment behavior, digital footprint signals, and alternative data — to produce highly accurate risk assessments for all borrower profiles, including thin-file applicants.

Self-Learning Business Rule Engine

Roopya’s Business Rule Engine does not just execute rules — it learns from outcomes. The platform identifies patterns in approval and rejection decisions, correlates them with loan performance, and suggests rule optimizations to continuously improve credit policy effectiveness. Lenders maintain full control while benefiting from AI-driven insights.

Conversational AI for Borrower Engagement

Borrower queries about EMI dates, outstanding balances, prepayment options, and account statements are handled automatically by Roopya’s conversational AI system. Available 24/7 across WhatsApp, SMS, and web chat, this capability dramatically reduces the load on customer support teams while improving borrower satisfaction through instant, accurate responses.

Roopya’s Unfair Advantages: What No Other LMS Offers

The market for lending software in India is crowded, but Roopya occupies a unique position. Here is what makes the platform genuinely different:

Go Live in 1 Day

Most enterprise lending software implementations take months. Roopya’s plug-and-play infrastructure and pre-configured loan products allow new lenders to go live and start processing loan applications within a single day. This speed to market is a decisive competitive advantage in the fast-moving digital lending space.

Truly No-Code Platform

Roopya is designed for business users, not developers. Loan products, credit policies, approval workflows, collection escalation rules, and reporting configurations are all managed through an intuitive visual interface. No coding skills are required at any stage. This means lenders can adapt to market changes and regulatory updates instantly, without waiting for IT teams or software vendors.

300+ Pre-Integrated APIs

Building an integration ecosystem from scratch is expensive and time-consuming. Roopya comes pre-integrated with over 300 APIs covering credit bureaus, KYC verification services, bank account validation, payment gateways, eSign platforms, and more. This comprehensive API library allows lenders to activate new capabilities in hours rather than months.

Pay-As-You-Use Pricing

Traditional enterprise software requires large upfront licensing fees that burden early-stage lenders. Roopya’s pricing model charges based on actual usage — meaning lenders with smaller portfolios pay proportionally less. As the business grows, the platform scales seamlessly without renegotiating contracts or upgrading infrastructure.

Always-Compliant Platform

Regulatory compliance is a moving target in Indian lending. Roopya’s team continuously monitors RBI guidelines, SEBI regulations, and industry standards, updating the platform proactively so that lenders are never caught off-guard by regulatory changes.

Who Should Use Automated Loan Management Software?

Roopya’s Automated Loan Management Software is designed for a wide range of lending institutions across the credit spectrum:

NBFCs and Fintech Lenders

Non-Banking Financial Companies represent the fastest-growing segment of Indian lending. Whether you are running a personal loan book, a business loan portfolio, or a microfinance operation, Roopya’s automated LMS provides the infrastructure to scale from hundreds to millions of loans without proportional headcount growth.

Microfinance Institutions (MFIs)

MFIs deal with high volumes of small-ticket loans across geographically dispersed customer bases. Manual management of such portfolios is prohibitively expensive and error-prone. Roopya’s automated workflows, mobile-first customer journey, and group lending support are purpose-built for MFI operations.

Banks and Cooperative Banks

Even established banks with legacy core banking systems can benefit from Roopya as a modern lending layer. Roopya’s open API architecture allows seamless integration with existing CBS platforms, enabling banks to modernize their retail and MSME lending operations without replacing their core infrastructure.

Loan Service Providers (LSPs)

LSPs that source and service loans on behalf of regulated lenders need robust technology to manage complex co-lending arrangements, sourcing commissions, and servicing obligations. Roopya supports multi-lender structures and provides the reporting tools needed for transparent performance management.

How Automated Loan Management Software Improves Key Metrics

The business case for investing in automated loan management software is compelling when examined through the lens of measurable outcomes:

| Metric | Manual Process | With Roopya LMS |

| Loan Processing Time | 3–7 days | Minutes to hours |

| Document Verification | Manual, 1–2 days | Automated, seconds |

| Credit Decision Time | 24–48 hours | Real-time |

| Collection Call Efficiency | 50–60 calls/agent/day | 300+ automated touchpoints/day |

| NPA Detection Lead Time | Post-default | 2–4 weeks pre-default |

| Compliance Reporting | 2–3 days/month | One-click, real-time |

| Cost per Loan | ₹800–₹1,500 | ₹150–₹300 |

Implementation Journey: From Sign-Up to First Loan in 1 Day

One of the most common objections to adopting new lending software is the fear of a long, disruptive implementation. With Roopya, that fear is unfounded. Here is a typical implementation journey:

Hour 1–2: Account Setup and Platform Configuration

After signing up, lenders access Roopya’s no-code configuration interface. Basic institutional parameters — company details, regulatory credentials, branding — are set up in under two hours.

Hour 2–4: Loan Product Configuration

Roopya’s 20+ pre-configured loan product templates cover personal loans, business loans, gold loans, home loans, payday loans, and more. Lenders select the relevant products, adjust parameters such as interest rate ranges, tenure, processing fees, and repayment frequency, and the system generates the complete product logic automatically.

Hour 4–6: Credit Policy and BRE Setup

Using the visual Business Rule Engine, lenders configure their credit policy — income eligibility thresholds, bureau score cutoffs, debt-to-income limits, and other underwriting criteria — without writing a single line of code.

Hour 6–8: API Integration and Testing

With 300+ pre-integrated APIs, most third-party connections are activated with a simple toggle. Lenders select their preferred bureau partners, KYC providers, payment gateways, and eSign services, and Roopya handles the integration configuration automatically.

Day 1: First Loan Processed

By end of day one, the platform is live. Borrower applications can flow through the complete automated journey — from application to credit decision to disbursement — with full audit trails and compliance documentation generated automatically.

Security, Compliance, and Data Privacy

For any financial institution, security is not optional — it is foundational. Roopya’s platform is built on enterprise-grade security infrastructure with compliance embedded at every layer:

- Bank-grade data encryption at rest and in transit (AES-256 / TLS 1.3)

- Role-based access control with granular permission management

- Complete audit trails for every user action and system event

- RBI-compliant data localization with servers hosted in India

- UIDAI-compliant Aadhaar eKYC integration

- ISO 27001-aligned security practices and regular penetration testing

- DPDP Act compliant data handling and consent management

- Multi-factor authentication for all platform users

Roopya’s compliance team monitors regulatory developments continuously and updates the platform proactively, ensuring that lenders are never scrambling to meet new requirements.

Choosing the Right Automated Loan Management Software

Not all loan management software is created equal. When evaluating options for your institution, consider the following criteria:

Scalability

Can the platform handle your current loan volume and scale seamlessly as you grow? Roopya’s cloud-native infrastructure supports everything from a 500-loan portfolio to millions of active accounts without performance degradation.

Integration Capability

Does the platform integrate with your existing systems and preferred third-party services? Roopya’s open REST API architecture and 300+ pre-integrated APIs ensure compatibility with virtually any technology stack.

Configurability vs Customization

True no-code configurability is more valuable than custom development. Configurations can be changed instantly by business users; custom code requires developer time and introduces risk. Roopya’s no-code approach gives lenders complete flexibility without technical dependency.

Total Cost of Ownership

Factor in not just the licensing fee but also implementation costs, ongoing maintenance, upgrade fees, and the cost of internal IT resources. Roopya’s pay-as-you-use model and no-code architecture minimize TCO at every stage.

Vendor Track Record

Has the vendor served institutions similar to yours? Roopya is trusted by modern lenders including IndiaKaLoan, QuickFinShop, EazyCredit, Findoc, and Recapita — a diverse portfolio that demonstrates platform versatility and reliability.