5 Benefits of Loan Origination System & Software Banks Can’t Ignore

The lending landscape in India is changing at a pace that leaves no room for complacency. With digital-first borrowers, aggressive fintech competition, and tightening regulatory expectations, banks that still rely on manual, paper-heavy loan origination processes are quietly bleeding market share — one slow approval at a time.

Loan origination System (LOS) has moved from being a “nice to have” innovation to a non-negotiable foundation for any lending institution serious about growth. The numbers back this up. A report by McKinsey found that banks deploying end-to-end digital lending platforms reduce cost-per-loan by up to 40% while improving customer satisfaction scores significantly. In a market as competitive as India’s, that kind of edge is not optional.

Yet, many banks — especially mid-sized commercial banks, cooperative banks, and NBFCs — hesitate. They worry about integration complexity, upfront costs, or simply the inertia of decades-old workflows. This article cuts through that hesitation and presents five concrete, high-impact benefits of loan origination software that every lending institution needs to understand before its next planning cycle.

Start Free Trial

What Is Loan Origination System & Software?

Before diving into the benefits, it helps to be precise about what loan origination software actually does.

Loan origination software is a digital platform that manages the entire lifecycle of a loan application — from the moment a borrower submits their request, through credit evaluation, document verification, underwriting, approval, and final disbursement. A modern LOS replaces the fragmented combination of spreadsheets, physical files, email threads, and manual credit checks that characterise traditional lending workflows.

Platforms like Roopya take this a step further by offering a no-code, unified lending infrastructure that covers origination, loan management, collections, early warning systems, and analytics — all in a single ecosystem. This means banks are not just digitising one step; they are transforming the entire credit delivery engine.

With that foundation in place, here are the five benefits banks simply cannot afford to overlook.

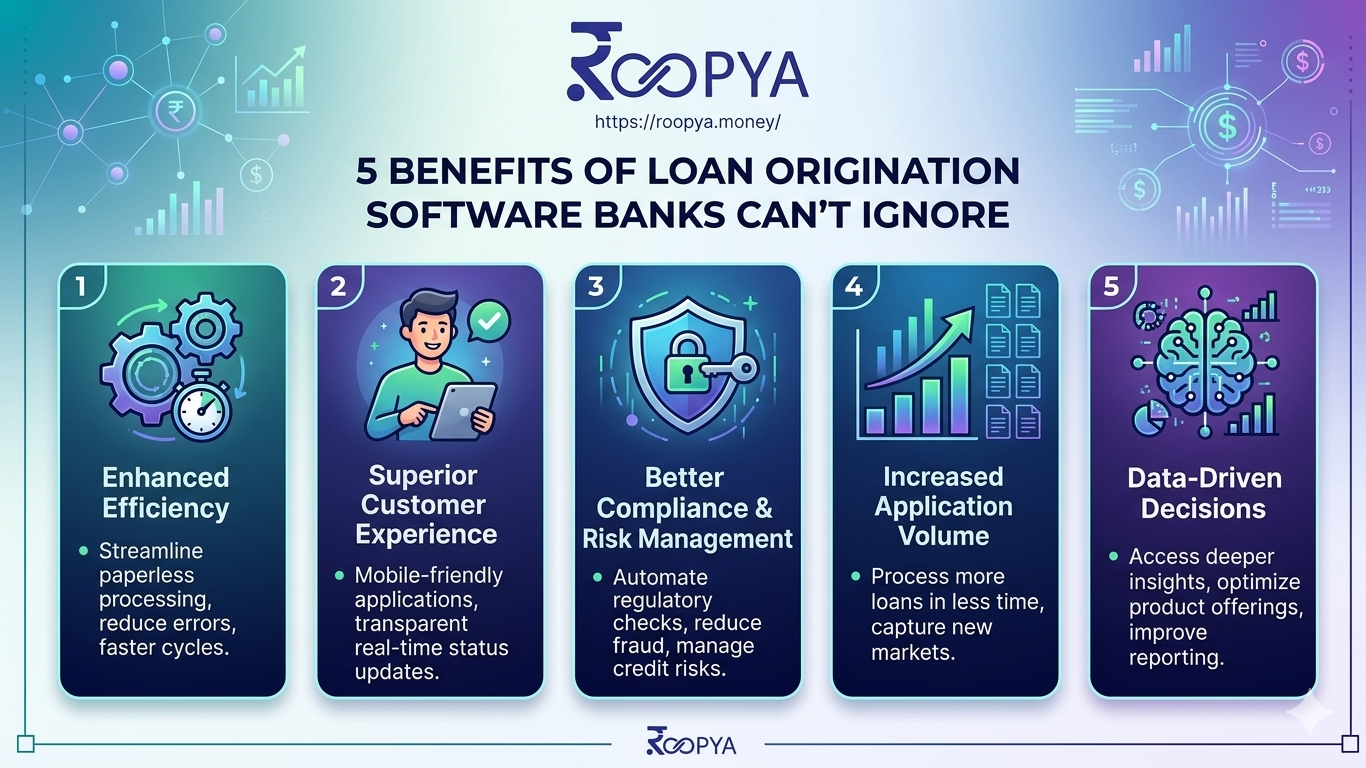

Benefit 1: Dramatically Faster Loan Processing and Disbursement

Speed is currency in modern lending. A borrower who applies for a personal loan or business credit today expects a decision — not in days, but in hours or even minutes. Banks that cannot meet this expectation are not just losing a transaction; they are losing a customer relationship, often permanently.

Traditional loan origination involves a painful sequence of manual steps. A loan officer collects documents, a credit team manually pulls bureau reports, a risk analyst reviews the file, a branch manager signs off, and then the documentation goes back and forth before disbursement. In practice, this process can take anywhere from 5 to 21 working days, depending on the loan type and the bank’s internal workflows.

Loan origination System & software collapses this timeline by automating every step that does not require genuine human judgment. Digital application forms capture borrower information accurately. Pre-integrated APIs pull credit bureau reports from CIBIL, Experian, or CRIF in real time. AI-powered document processing reads and verifies KYC documents, bank statements, and income proofs in seconds rather than hours. Automated rule engines evaluate creditworthiness against predefined policies and fire instant decisions.

Roopya’s platform, for instance, comes with 300+ pre-integrated APIs covering credit bureaus, e-KYC providers, bank statement analysers, and payment gateways — all activated without any additional development work. The result is a loan journey that can go from application to disbursement in a matter of hours for standard retail products.

For banks, faster processing directly translates to higher loan volumes without proportional increases in headcount. For borrowers, it means a dramatically better experience that builds loyalty. Both outcomes improve the institution’s bottom line.

The practical impact: Banks that have deployed modern loan origination platforms report reductions in turnaround time (TAT) of 60–80%. For high-volume products like personal loans or two-wheeler financing, this is the difference between processing 200 applications a day and processing 2,000.

Benefit 2: Superior Credit Risk Assessment and Lower NPA Rates

Non-performing assets remain one of the most persistent threats to bank profitability in India. While macroeconomic factors play a role, a significant proportion of NPAs trace back to weak underwriting — loans approved on incomplete information, outdated scoring models, or the instincts of individual loan officers rather than data-driven frameworks.

Modern loan origination software addresses this problem at the root. Instead of relying on a single credit score and a few financial ratios, a good LOS integrates multiple data sources and applies machine learning models to generate a far more nuanced picture of borrower risk.

This includes:

- Bureau data from multiple credit information companies to assess repayment history across lenders

- Bank statement analysis to evaluate actual cash flows, spending patterns, and income stability — not just declared income

- GST and ITR data for SME borrowers, providing verified revenue and tax compliance signals

- Alternative data signals such as mobile phone usage patterns, utility bill payment history, and social indicators, particularly useful for thin-file borrowers

Beyond data richness, a sophisticated loan origination system like Roopya includes a no-code Business Rule Engine (BRE) that allows credit teams to configure and update underwriting rules without depending on IT. This means risk policies can be tightened immediately when market conditions shift — for example, reducing exposure to a particular borrower segment during an economic slowdown — without waiting weeks for a software update.

AI-powered credit scoring models on modern platforms also analyse thousands of data points simultaneously and continuously learn from the bank’s own portfolio outcomes, improving predictive accuracy over time. Roopya’s platform, for instance, offers machine learning-based credit scoring that delivers up to 40% better accuracy compared to traditional rule-based approaches.

The outcome is measurably lower default rates. When the right borrowers are approved at the right loan amounts with appropriate pricing, the bank’s NPA ratio improves. This is not a theoretical claim — it is the lived experience of lending institutions that have moved from gut-feel underwriting to data-driven origination platforms.

The practical impact: Better risk models mean fewer defaults, lower provisioning costs, and stronger capital adequacy ratios. For a mid-sized bank managing a ₹2,000 crore retail loan book, even a 1% improvement in NPA rates translates to ₹20 crore in reduced credit losses annually.

Benefit 3: Regulatory Compliance Built In, Not Bolted On

Regulatory compliance is one of the most significant operational burdens facing banks in India. RBI guidelines on KYC norms, Fair Practices Code requirements, digital lending regulations, data localisation rules, and reporting obligations create a complex web that must be navigated meticulously — on every loan, every day.

Manual processes are inherently compliance-risky. When individual officers are responsible for verifying documents, maintaining audit trails, and generating regulatory reports, errors are inevitable. A missed field, a misplaced document, or a reporting gap can trigger regulatory scrutiny and penalties.

Loan origination software bakes compliance into the process architecture rather than treating it as an afterthought. Every step in a digitised loan journey is logged automatically, creating an immutable audit trail. Document collection is standardised — the system will not allow an application to proceed to the next stage unless mandatory KYC fields are complete and verified. Consent management is built into digital onboarding flows, ensuring borrowers explicitly agree to data usage and terms before processing begins.

This is particularly critical in the context of the RBI’s Digital Lending Guidelines, which place strict requirements on lender conduct, transparency, and data privacy for digital loan products. A modern LOS like Roopya is continuously updated to reflect the latest regulatory changes, so banks do not have to scramble to retrofit compliance requirements after the fact.

Automated regulatory reporting is another major advantage. Monthly and quarterly submissions to regulators — portfolio data, sector exposures, delinquency reports — can be generated directly from the LOS data layer, reducing the manual effort of compiling reports across multiple systems and eliminating transcription errors.

Beyond mandatory compliance, there is also the question of internal governance. Loan origination software enforces delegation of authority (DoA) hierarchies automatically, ensuring that loan approvals above a certain threshold go through the correct sign-off chain. This prevents rogue approvals and strengthens internal controls.

The practical impact: Banks using integrated loan origination platforms report significant reductions in compliance-related audit findings and near-zero instances of process non-compliance on audited loans. The cost savings from avoiding regulatory penalties and the reputational protection this provides are difficult to overstate.

Benefit 4: Scalability Without Proportional Cost Increases

One of the most compelling economic arguments for loan origination software is what it does to the cost structure of lending operations. Traditional banks face a frustrating constraint: growing the loan book requires growing the team. More applications mean more loan officers, more credit analysts, more operations staff, and more branch infrastructure. The marginal cost of each new loan approved stays stubbornly high.

Loan origination software fundamentally changes this equation. By automating the high-volume, repetitive tasks that consume the majority of operational hours — data entry, document verification, credit bureau pulls, eligibility checks — an LOS allows the bank to handle significantly more loan applications without a proportional increase in headcount.

Consider a bank processing 500 personal loan applications per month with a team of 15 operations staff. After deploying a loan origination platform, the same team can handle 3,000 applications per month because the system automatically processes 80–90% of the work. The marginal cost per loan drops dramatically, and the team’s energy is redirected to genuinely complex cases and customer relationships.

Roopya’s pricing model reinforces this scalability argument. Unlike legacy software vendors who charge large upfront licence fees plus annual maintenance contracts, Roopya operates on a pay-as-you-use model with zero upfront cost. Banks only pay for what they actually process, which means the platform scales economically with the business rather than creating a fixed cost burden during lean periods.

The platform’s no-code configuration also dramatically reduces dependency on external technology vendors for product changes. When a bank wants to launch a new loan product — say, a co-lending product with an NBFC partner, or a new SME working capital line — the business team can configure the product journey, set the eligibility rules, and activate the product within days using Roopya’s no-code interface. The traditional alternative — scoping a project with an IT vendor, waiting for development, testing, and deployment — could take 3 to 6 months.

This agility is a form of scalability too. Banks that can launch new products faster capture market opportunities that slower-moving competitors miss.

The practical impact: Deploying loan origination software typically reduces the cost per loan originated by 30–50%. For a bank disbursing ₹500 crore annually in retail loans, this translates to crores in operational savings that can be reinvested in growth, technology, or customer acquisition.

Benefit 5: A Lending Experience That Wins and Retains Customers

The fifth benefit is the one that ties all the others together: loan origination software delivers a borrower experience that modern customers actually want — and rewards institutions that provide it with loyalty, referrals, and repeat business.

Today’s borrowers — whether individual consumers or small business owners — benchmark their banking experience against the best digital experiences they encounter anywhere. They expect the ability to apply for a loan from their smartphone in minutes. They expect transparency about where their application stands. They expect to provide documents digitally, not through physical courier or branch visits. And they expect a decision that respects their time.

Banks that cannot meet these expectations are not competing on the same playing field as fintech lenders and new-age NBFCs that were built digital-first. Loan origination software is the infrastructure that allows traditional banks to close this experience gap without starting from scratch.

A well-designed LOS provides borrowers with a seamless digital application journey — mobile-optimised forms, video KYC, digital document upload, real-time application status updates, and instant in-principle decisions. For branch-based applications, the same platform ensures the loan officer has a clean, guided digital interface rather than juggling paper forms and multiple screens.

Post-approval, the integration between the LOS and the Loan Management System (LMS) ensures that disbursement, repayment scheduling, and account servicing are equally smooth. Borrowers who have a positive end-to-end experience are significantly more likely to return for their next credit need — and to recommend the bank to family, friends, and business associates.

Roopya’s platform extends this further with an automated customer loan journey module that handles borrower communication at every touchpoint — application confirmation, document request reminders, approval notifications, and disbursement alerts — all without manual intervention. This creates a professional, consistent experience even for banks with limited customer communication infrastructure.

There is also a powerful data advantage embedded in this benefit. Every interaction a borrower has within the LOS generates data — application behaviour, document submission patterns, channel preferences — that the bank can use to personalise future offers, identify cross-sell opportunities, and deepen the customer relationship over time.

The practical impact: Banks with superior digital lending journeys report customer acquisition costs that are 40–60% lower than traditional channel acquisition, and retention rates significantly higher than industry averages. In a market where acquiring a new credit customer costs anywhere from ₹1,500 to ₹5,000, the retention advantage alone justifies the investment in a modern LOS.

Bringing It All Together: The Roopya Advantage

The five benefits outlined above — faster processing, better risk assessment, built-in compliance, operational scalability, and superior customer experience — are not independent advantages. They compound each other. A bank that approves loans faster with better risk models, at lower cost, in full compliance, while delighting borrowers, is a fundamentally different competitive entity from one that operates manually.

Roopya’s lending platform is designed to deliver all five benefits simultaneously. As India’s leading digital lending infrastructure provider for NBFCs, banks, and modern lenders, Roopya offers:

- A no-code loan origination platform that goes live in as little as one day

- 300+ pre-integrated APIs covering every touchpoint in the lending lifecycle

- An AI-powered credit decisioning engine that learns and improves with every loan

- A pay-as-you-use pricing model that eliminates upfront capital risk

- A continuously updated compliance framework that keeps institutions ahead of RBI guidelines

- 20+ pre-configured loan products ready to launch immediately

Whether you are a scheduled commercial bank looking to modernise your retail lending stack, or an NBFC scaling from ₹100 crore to ₹1,000 crore in disbursements, Roopya provides the infrastructure to grow without the friction.

Loan origination software is not a technology upgrade — it is a strategic imperative. The institutions that recognise this early will compound their advantages quarter after quarter: lower costs, better asset quality, faster growth, and deeper customer relationships. Those that wait will find the gap increasingly difficult to close.

The question is not whether your bank needs a modern loan origination platform. The question is how much longer you can afford to operate without one.

Ready to see what Roopya can do for your lending operations? Request a demo today and experience the platform that is redefining how India’s lenders grow.

Roopya is India’s #1 digital lending software platform, offering complete LOS and LMS solutions for NBFCs, banks, and modern lenders. Learn more at roopya.money.