Benefits of a Loan Origination System for NBFCs & Banks: The Complete Guide

Why Loan Origination Is the Backbone of Every Lending Business

In the highly competitive landscape of Indian lending, NBFCs and banks face a common challenge: processing loan applications fast, accurately, and at scale — without compromising compliance or borrower experience. Manual loan processing, siloed data, lengthy turnaround times, and rising operational costs have made legacy origination processes a liability, not an asset.

Enter the Loan Origination System (LOS) — a purpose-built digital infrastructure that transforms every step of the lending lifecycle, from the first application click to final loan disbursal.

A modern Loan Origination Software is not just a form-digitization tool. It is an intelligent, end-to-end platform that orchestrates credit decisions, automates KYC and document verification, integrates with multiple credit bureaus, and delivers real-time decisioning at scale. For NBFCs, MFIs, and banks operating in India’s fast-moving credit ecosystem, adopting the right LOS can mean the difference between growing 10x and stagnating.

In this comprehensive guide, we explore every significant benefit of a Loan Origination System for NBFCs and banks — and how Roopya’s AI-powered Loan Origination Platform is purpose-built to deliver these advantages from day one.

Start Free Trial

What Is a Loan Origination System (LOS)?

A Loan Origination System is a technology platform that manages and automates the entire loan application and approval process. It covers every stage of the loan lifecycle — from customer onboarding and application submission through credit assessment, underwriting, documentation, approval, and disbursal.

Think of an LOS as the central nervous system of a lending institution. It connects the front-end borrower experience with back-end credit, compliance, and risk operations into one seamless, automated workflow.

The Core Loan Origination Process Includes:

1. Lead Capture & Customer Onboarding — Borrowers submit applications through digital channels (web, mobile, DSA portals). The LOS captures application data, validates identity documents, and initiates KYC checks instantly.

2. Document Collection & Verification — Applicants upload required documents. The system uses AI-powered OCR to extract and validate data from Aadhaar, PAN, bank statements, salary slips, and more.

3. Credit Bureau Checks — The LOS automatically pulls credit reports from CIBIL, Experian, Equifax, and CRIF, providing a multi-bureau view of the applicant’s credit history and risk profile.

4. Automated Underwriting & Decisioning — Using scorecards, business rules, and AI/ML models, the platform evaluates the applicant’s creditworthiness and delivers an instant approval, rejection, or counter-offer decision.

5. Loan Sanctioning & Documentation — Approved applications move to a digital documentation stage where loan agreements, sanction letters, and terms are generated and executed digitally.

6. Disbursal & Handoff to LMS — Once documentation is complete, the LOS triggers disbursement and seamlessly passes the loan to the Loan Management System (LMS) for servicing.

The Business Case: Why Manual Loan Processing Is No Longer Viable

Before diving into benefits, it is important to understand the cost of NOT having a modern LOS.

Manual and semi-digital loan processing results in:

- High TAT (Turnaround Time): Manual processes take 5–15 days for decisions that an LOS can deliver in minutes.

- High Operational Costs: Large teams of credit analysts, verification officers, and data entry personnel drive up cost-per-loan.

- Data Errors & Fraud Exposure: Manual data entry creates errors and leaves institutions vulnerable to identity fraud and document forgery.

- Regulatory Risk: Manual compliance tracking increases the risk of RBI guideline violations, audit failures, and penalties.

- Poor Borrower Experience: Slow, opaque, paper-heavy processes lead to application abandonment and poor NPS scores.

- Limited Scalability: Manual workflows create a ceiling on loan volume that prevents growth without proportionally increasing headcount.

A modern Loan Origination Software eliminates all of these pain points simultaneously.

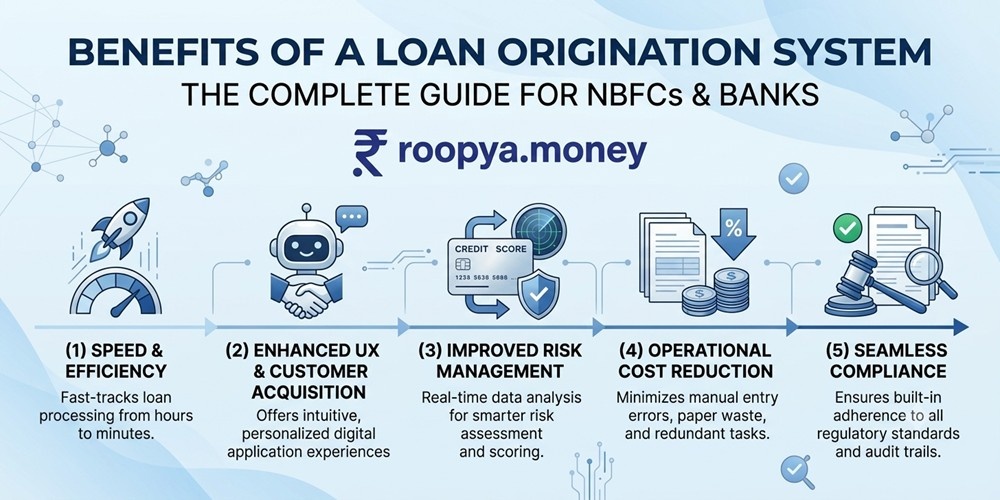

Top 15 Benefits of a Loan Origination System for NBFCs & Banks

1. Dramatically Reduced Loan Processing Time (TAT)

Speed is the most immediately visible benefit of an LOS. What once required days of manual review — credit bureau pulls, document verification, underwriting — can now happen in minutes.

Modern platforms like Roopya process loan applications end-to-end with automated decisioning pipelines that evaluate hundreds of data points simultaneously. Credit decisions that previously required analyst review can be automated for standard profiles, reserving human review only for edge cases or complex credit structures.

For NBFCs targeting high-volume retail or MSME lending, a reduced TAT directly translates to higher loan disbursement volumes, better conversion rates, and stronger borrower satisfaction. In a competitive market where borrowers compare multiple lenders, a lender that responds in 2 minutes will always win over one that responds in 2 days.

Real Impact: Leading NBFCs using modern LOS platforms report TAT reductions of up to 80%, moving from multi-day processing to same-day or real-time disbursal.

2. End-to-End Process Automation

A Loan Origination System automates every manual step in the lending process:

- Application intake and data extraction

- Identity verification (Aadhaar OTP, DigiLocker, Video KYC)

- Credit bureau queries across multiple bureaus

- Document collection, OCR, and validation

- Scorecard-based and rule-based credit decisioning

- Loan agreement generation and eSign

- Disbursal triggers to banking or payment systems

This automation eliminates repetitive manual tasks, reduces error rates to near zero, and allows lending teams to focus on relationship management and exception handling rather than data processing. For small and mid-size NBFCs, this means operating with a lean team at significantly higher loan volumes.

Roopya’s No Code Loan Origination Platform automates the complete journey without requiring any technical development, making automation accessible to lenders of all sizes.

3. Intelligent Automated Underwriting

Traditional credit underwriting relies heavily on manual judgment, which introduces inconsistency, bias, and delays. An LOS replaces manual underwriting with structured, rule-based, and AI-driven decisioning that is both faster and more consistent.

Automated underwriting in a modern LOS includes:

- Application Scorecards: Statistical models that score each applicant based on demographic, financial, and behavioral attributes.

- Business Rule Engine (BRE): Configurable logic trees that encode the lender’s credit policy, including hard rejections, conditional approvals, and tiered pricing rules.

- AI/ML Credit Models: Machine learning models that go beyond traditional bureau scores to evaluate alternative data signals — bank account behavior, GST filings, utility payments, and digital footprint.

- Multi-bureau Deduplication: Combining data from CIBIL, Experian, Equifax, and CRIF for a comprehensive credit picture.

Roopya’s AI-Enhanced Business Rule Engine continuously learns from approval and rejection outcomes, improving decisioning accuracy over time without requiring manual rule updates.

Real Impact: AI-powered underwriting delivers 40% better credit decision accuracy compared to traditional manual models, reducing both default rates and false rejections.

4. Seamless Digital KYC and Document Verification

KYC compliance is mandatory for every lender, but traditional KYC is one of the biggest sources of friction and delay in the loan process. A modern LOS integrates with India’s KYC infrastructure to deliver instant, friction-free verification.

Roopya’s LOS supports:

- Aadhaar-based eKYC (OTP and biometric)

- DigiLocker integration for instant document access

- Video KYC (V-KYC) for remote customer verification

- PAN verification through NSDL/UTIITSL

- GST verification for business borrowers

- Bank account verification via penny drop or account aggregator

- AI-powered OCR for document data extraction with 99%+ accuracy

For NBFCs targeting digital-first borrowers, seamless KYC is not just a regulatory requirement — it is a competitive differentiator. Borrowers who encounter friction during KYC abandon applications at high rates. A smooth, paperless KYC experience significantly improves conversion rates.

5. 300+ Pre-Integrated APIs for Complete Ecosystem Access

One of the most time-consuming aspects of building a lending technology stack is integrating with the dozens of third-party services required for modern lending — credit bureaus, KYC providers, payment gateways, account aggregators, GST APIs, eSign platforms, and more.

A mature LOS platform like Roopya comes with 300+ pre-built API integrations spanning:

- Credit Bureaus (CIBIL, Experian, Equifax, CRIF)

- eKYC Providers (Aadhaar, DigiLocker)

- Account Aggregator (AA) Framework

- Bank Statement Analysers

- Payment Gateways and NACH/eNACH providers

- eSign and eSeal providers

- GST and Income Tax data APIs

- Legal and property verification services

- Fraud detection and device fingerprinting services

This pre-integrated ecosystem means an NBFC can go live with a fully functional LOS in as little as 1 day, rather than spending months and crores building API integrations from scratch.

6. No-Code Configuration for Business Agility

In a fast-moving lending market, the ability to rapidly change credit policies, launch new loan products, or modify workflows is critical. Traditional LOS platforms require IT involvement and weeks of development time to make changes. This creates dangerous bottlenecks between business strategy and execution.

Roopya’s Truly No-Code Platform gives business users — not developers — full control over:

- Credit policy rules and business logic (BRE)

- Loan product configurations (interest rates, tenures, eligibility criteria)

- Customer application journeys and form fields

- Approval workflows and escalation matrices

- Document checklists and verification rules

- Reporting templates and dashboard configurations

This self-service configurability means an NBFC can respond to a market opportunity, a regulatory change, or a portfolio insight within hours rather than weeks. The competitive advantage of speed-to-market in launching new loan products cannot be overstated.

7. Advanced Fraud Detection and Risk Mitigation

Loan fraud is a growing challenge for Indian lenders, with identity fraud, document forgery, synthetic identities, and collusion between applicants and agents all on the rise. Manual verification processes are entirely inadequate at detecting sophisticated fraud.

A modern LOS incorporates multiple layers of AI-powered fraud detection:

- Document Authenticity Verification: AI models detect tampered documents, forged bank statements, and altered identity documents with high accuracy.

- Facial Liveness Detection: During Video KYC, liveness checks prevent photo spoofing or pre-recorded video attacks.

- Negative Database Checks: Applicants are screened against internal and industry-wide negative lists, including defaulter lists and fraud databases.

- Device Intelligence: Device fingerprinting identifies suspicious patterns such as multiple applications from the same device with different identities.

- Network Analysis: Graph-based analytics detect collusion networks between borrowers, guarantors, and agents.

Roopya’s built-in AI fraud modules have demonstrated up to 80% fraud reduction for lenders compared to manual verification processes. Every rupee saved from fraud flows directly to the bottom line.

8. Regulatory Compliance Built Into the Workflow

The regulatory environment for NBFCs and banks in India is increasingly demanding. RBI guidelines on KYC norms, FLDG regulations, account aggregator compliance, Fair Practices Code, and CIBIL reporting requirements must all be adhered to meticulously. Non-compliance can result in penalties, operational restrictions, or reputational damage.

A purpose-built LOS ensures compliance is not an afterthought but a built-in feature of every workflow:

- Automated RBI-compliant KYC workflows

- Mandatory cooling-off period enforcement

- Regulatory report generation (SMA classification, NPA provisioning inputs)

- Audit trail and activity logging for every action in the system

- CIBIL and bureau reporting automation

- FLDG partner compliance workflows

- eSign through legally compliant platforms

Roopya’s platform is continuously updated to reflect the latest regulatory changes, ensuring lenders are always compliant without manual intervention or expensive compliance consultants.

9. Superior Borrower Experience and Higher Conversion

In the digital age, borrowers have zero patience for complicated, slow, or opaque loan processes. The borrower experience delivered by an LOS directly impacts application conversion, customer satisfaction, and referral rates.

A modern LOS delivers borrower experience features including:

- Mobile-First Applications: Fully responsive digital application journeys optimised for smartphone users.

- Real-Time Status Tracking: Borrowers receive live updates on their application status, reducing anxiety and support call volumes.

- Instant In-Principle Approvals: Pre-qualification decisions delivered instantly using soft bureau pulls.

- Digital Documentation: Loan agreements and sanction letters delivered and signed digitally, eliminating the need for physical visits.

- Multilingual Support: Application journeys available in regional languages to reach deeper credit-underserved markets.

- Omnichannel Access: Borrowers can apply via web, mobile app, branch, or through DSA/LSP partners.

Improving borrower experience is not just a branding investment — it directly increases conversion rates and reduces cost-per-acquisition. NBFCs that deliver a sub-3-minute digital application journey report 2–3x higher conversion rates compared to those with traditional processes.

10. Scalability to Handle High Loan Volumes

Growth is the goal of every lending institution, but growth creates processing challenges. Manual processes create hard ceilings on loan volumes — you can only process as many loans as your headcount allows.

A cloud-based LOS removes this ceiling entirely. The system scales automatically to handle surges in application volumes — whether driven by seasonal demand, marketing campaigns, or partnership channels — without adding headcount or infrastructure.

Roopya’s cloud-native infrastructure handles everything from a few hundred applications per month to millions of applications per year on the same platform. This elastic scalability is a fundamental requirement for NBFCs with growth ambitions.

Key scalability features include:

- Cloud-native architecture with auto-scaling

- Parallel processing for simultaneous application handling

- Multi-channel intake (direct, DSA, marketplace, embedded)

- Automated workflows that process applications 24/7

11. Data-Driven Insights and Lending Analytics

Every loan application, approval, rejection, and default is a data point. An LOS captures all of this data and, combined with a lending analytics layer, transforms it into actionable business intelligence.

Analytics capabilities of a modern LOS include:

- Application Funnel Analytics: Track drop-off rates at each stage to identify and fix conversion bottlenecks.

- Credit Policy Performance: Analyse how different credit rules impact approval rates, default rates, and portfolio yield.

- Portfolio Risk Analytics: Monitor portfolio health by segment, geography, channel, and product.

- Channel Performance: Evaluate loan volume, quality, and profitability by origination channel — direct, DSA, embedded, branch.

- TAT Analytics: Track processing times across stages to identify bottlenecks.

- Credit Scorecard Monitoring: Ensure scorecards remain predictive by monitoring Gini coefficients, KS statistics, and PSI.

Roopya combines its Loan Origination Platform with dedicated Lending Analytics and Credit Risk Analytics capabilities, providing lenders with a 360-degree intelligence layer over their entire loan book.

12. Seamless Multi-Channel and DSA/LSP Partner Management

For most NBFCs, a significant proportion of loan volume originates through DSAs (Direct Selling Agents), LSPs (Loan Service Providers), and channel partners. Managing these partners manually — tracking logins, calculating commissions, monitoring performance, and maintaining compliance — is operationally intensive.

An LOS with integrated DSA/LSP Management provides:

- Dedicated partner portals for application submission

- Real-time application status visibility for partners

- Automated commission calculation and payout triggers

- Partner performance dashboards and SLA monitoring

- Compliance documentation management for each partner

- Configurable access controls and product mapping per partner

Roopya’s LSP Onboarding Module allows NBFCs to onboard and activate new channel partners rapidly, expanding distribution without building a captive sales force.

13. Faster Go-Live and Lower Total Cost of Ownership (TCO)

Building a proprietary LOS from scratch is an enormous undertaking. It requires a large engineering team, significant capital investment, 12–24 months of development time, and ongoing maintenance and upgrade costs. For most NBFCs, this is simply not viable.

A SaaS-based LOS platform like Roopya dramatically changes the economics:

- Go-Live in 1 Day: Pre-built, pre-integrated, and pre-configured infrastructure means launch in days, not months.

- Zero Upfront Cost: Pay-as-you-use pricing eliminates large upfront capital commitments.

- No IT Dependency: No-code configuration removes the need for a large in-house technology team.

- Automatic Upgrades: Platform updates, new integrations, and regulatory changes are deployed automatically.

- Predictable Operating Costs: Usage-based pricing grows proportionally with loan volume, aligning technology costs with business performance.

For startups and growth-stage NBFCs, this model means access to enterprise-grade lending infrastructure at a fraction of the traditional cost — leveling the playing field with large banks and established lenders.

14. Comprehensive Audit Trails and Operational Transparency

Every lending decision, user action, system event, and data change in a modern LOS is automatically logged in a tamper-proof audit trail. This provides:

- Regulatory Audit Readiness: Complete documented evidence for RBI and statutory audits.

- Credit Committee Reports: Automated generation of credit appraisal memos and decision documentation.

- Dispute Resolution: Full history of every interaction and decision for resolving borrower or partner disputes.

- Operational Oversight: Management can monitor team productivity, decision override rates, and policy adherence in real time.

- Fraud Investigation: Detailed logs enable forensic investigation of suspected fraudulent applications.

Operational transparency is increasingly important as regulators demand greater accountability from lending institutions. An LOS makes compliance with these transparency requirements effortless.

15. Seamless Integration with LMS, Collections, and the Complete Lending Stack

An LOS does not operate in isolation. The true power of a modern loan origination system is its seamless connection with downstream systems — the Loan Management System, Collections, Early Warning System, and Analytics.

When an LOS and LMS are built on the same platform (as with Roopya), data flows seamlessly from origination to servicing without manual re-entry, reducing errors and processing delays. The borrower profile, credit data, and loan terms established during origination are instantly available in the LMS for payment scheduling, customer service, and portfolio management.

Roopya’s unified lending platform covers the complete lifecycle:

- Loan Origination System (LOS) → Loan disbursal

- Loan Management System (LMS) → Servicing and collections

- Early Warning System → Portfolio risk monitoring

- Collections System → Recovery management

- Lending Analytics → Cross-lifecycle intelligence

This integrated approach eliminates technology fragmentation and provides a single source of truth for the entire lending operation.

LOS vs. Manual Lending Process: A Direct Comparison

| Parameter | Manual Process | Modern LOS (Roopya) |

|---|---|---|

| Application TAT | 5–15 days | Minutes to same day |

| Credit Decision | Manual analyst review | AI + Rules-based automation |

| KYC | Physical documents | Digital/eKYC in seconds |

| Fraud Detection | Limited manual checks | AI-powered, 80% fraud reduction |

| Scalability | Limited by headcount | Unlimited (cloud-native) |

| Compliance | Manual tracking | Built-in, auto-updated |

| Cost per Loan | High (manual effort) | Significantly lower |

| Go-Live Time | 12–24 months (build) | 1 day (SaaS platform) |

| Reporting | Manual MIS | Real-time dashboards |

| Partner Management | Spreadsheets/email | Integrated DSA portals |

Who Should Adopt a Loan Origination System?

A modern Loan Origination System is relevant to a broad range of financial institutions:

NBFCs (Non-Banking Financial Companies): Whether you are a startup NBFC looking to launch or a growth-stage institution looking to scale, an LOS provides the infrastructure backbone for efficient, compliant, and profitable lending.

Microfinance Institutions (MFIs): High-volume, small-ticket lending demands automation. Manual processing of thousands of small loans per day is operationally impossible without an LOS.

Banks (Cooperative, Small Finance, Urban): Smaller banks competing against large private banks and fintechs need technology parity. An LOS delivers digital capabilities that match the best in class.

Fintech Lenders: Digital-native lenders need an LOS that is API-first, cloud-native, and built for high-velocity lending.

Embedded Finance Providers: Organizations offering lending at the point of sale (Buy Now Pay Later, Supply Chain Finance, Merchant Loans) need an LOS that integrates invisibly into partner ecosystems.

Choosing the Right Loan Origination Software: Key Evaluation Criteria

When evaluating Loan Origination Software for your institution, consider the following:

1. Time to Deployment: Can the platform go live in days rather than months? Delays mean lost loan business.

2. No-Code Configurability: Can your team configure credit policies, workflows, and products without engineering involvement?

3. API Ecosystem Depth: How many third-party services are pre-integrated? Every missing integration is a development project.

4. Compliance Coverage: Does the platform maintain up-to-date compliance with RBI and other regulatory requirements?

5. AI & Automation Maturity: How advanced are the platform’s AI-powered decisioning, fraud detection, and document processing capabilities?

6. Scalability Architecture: Is the platform cloud-native and capable of scaling with your growth trajectory?

7. Analytics Depth: Does the platform provide actionable insights, or just raw data?

8. Pricing Model: Is pricing aligned with your growth — pay-per-use vs. fixed license fees?

9. Vendor Track Record: Does the vendor have proven deployments with institutions similar to yours?

10. Integrated LMS: Does the origination platform integrate seamlessly with the servicing system to avoid data fragmentation?

Roopya checks every box on this list — it is India’s only unified, no-code lending platform that combines LOS, LMS, Collections, Early Warning, and Analytics in a single, fully integrated stack.

How Roopya’s Loan Origination System Delivers These Benefits

Roopya was purpose-built for modern Indian lenders — NBFCs, banks, MFIs, and fintechs — who need enterprise-grade lending infrastructure without enterprise-level complexity or cost.

Here is what makes Roopya’s Loan Origination Platform stand apart:

India’s Fastest Go-Live: Roopya’s plug-and-play infrastructure means lenders can start processing loans within 1 day of signing up — with all integrations, workflows, and compliance modules pre-configured.

Truly No-Code: From credit policy to customer journey to reporting, everything in Roopya is configurable by business users without writing a single line of code.

300+ Pre-Integrated APIs: Credit bureaus, KYC providers, bank statement analysers, payment gateways, eSign platforms — all connected and ready to use.

AI-Powered Intelligence: Advanced ML models handle document processing, credit decisioning, fraud detection, and portfolio analytics, delivering measurably better outcomes than manual or rule-only approaches.

Pay-As-You-Use Pricing: Zero upfront costs, no long-term lock-in. Roopya’s pricing grows with your loan book, ensuring technology costs remain proportionate to your business.

Unified Platform: LOS, LMS, Collections, Early Warning, and Analytics — all built and maintained by the same team on the same infrastructure for seamless data flow and zero integration friction.

20+ Pre-Configured Loan Products: Personal loans, business loans, gold loans, payday loans, home loans, auto loans — ready-to-launch product templates reduce time-to-market significantly.

Conclusion: The LOS Is No Longer Optional — It Is Table Stakes

The Indian lending market is at an inflection point. Digital lending disbursements are growing at over 30% annually. The RBI’s regulatory framework is pushing all lending institutions toward digital, compliant, and accountable operations. Borrower expectations — shaped by consumer fintech experiences — demand speed, transparency, and convenience.

In this environment, a Loan Origination System is not a luxury or a nice-to-have. It is the fundamental infrastructure without which an NBFC or bank cannot compete effectively, scale sustainably, or remain compliant reliably.

The question is no longer whether to adopt a Loan Origination Software, but which platform will deliver the best combination of speed, capability, compliance, and value for your institution.

Roopya offers India’s most complete, most affordable, and fastest-to-deploy Loan Origination Platform — built specifically for the institutions, products, and regulatory environment of the Indian lending market.