Roopya Lending Platform helps lenders to implement all the best practices for loan origination like:

1. Pre-Application and Lead Management

Lead Qualification and Management: Roopya platform has advanced analytics to qualify leads effectively and use CRM systems to manage interactions, ensuring timely follow-ups.

Digital Marketing and Outreach: Use targeted digital marketing strategies to reach potential borrowers based on their interests and financial behaviour.

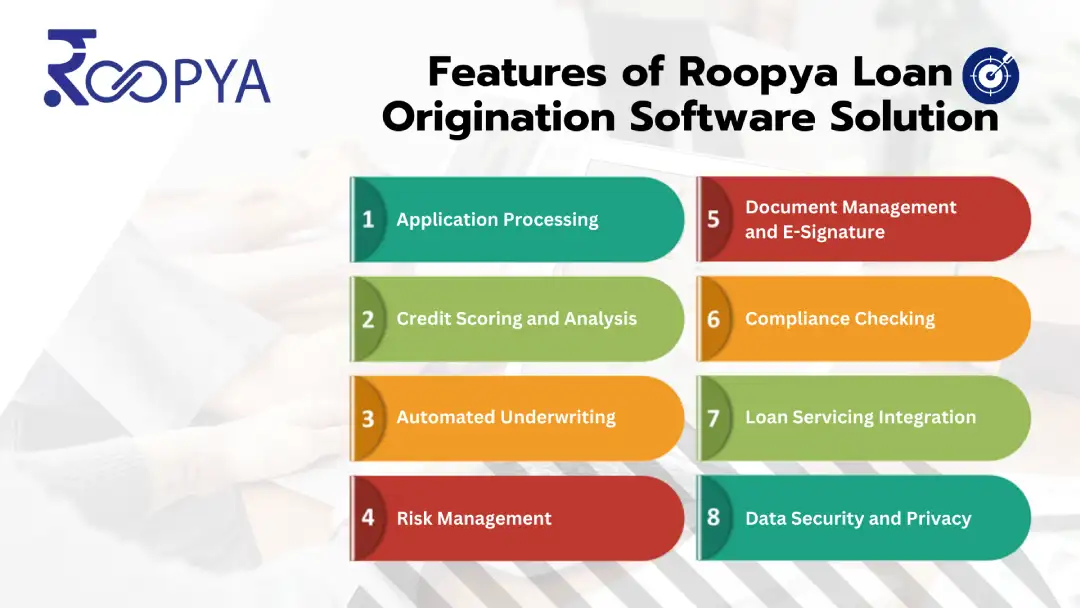

2. Application Processing

Digital Application Processes: Roopya offers automated online journey for loan application process that is user-friendly, accessible on multiple devices, and capable of saving progress.

Automated Data Capture: Use OCR (Optical Character Recognition) and data extraction tools to minimize manual data entry and accelerate the application process.

3. Roopya Credit Scoring and Analysis

Comprehensive Credit Assessment: Incorporate traditional and alternative data (like rent payment history, utility payments) for a more holistic view of creditworthiness.

Transparent Scoring Criteria: Maintain transparency about the factors affecting credit scores and loan decisions to build trust with applicants.

4. Underwriting and Decision Making

Automated Underwriting Systems (AUS): Roopya AUS speeds up decision-making processes, while ensuring consistency and compliance with lending policies.

Manual Review for Complex Cases: Establish protocols for manual review of applications flagged by automated systems to ensure fair and thorough evaluation.

5. Approval and Disbursement

Electronic Signatures and Documentation: Roopya platform facilitates use of e-signatures and digital documents to expedite the loan closing and disbursement process.

Timely Disbursement: Ensure loan amounts are disbursed promptly upon approval to meet customer expectations and enhance satisfaction.

6. Roopya Risk Management Platform

Dynamic Risk Assessment Models: Regularly update risk models to incorporate new data and trends, improving predictive accuracy over time.

Stress Testing: Conduct periodic stress tests on loan portfolios to assess potential impacts of economic downturns and adjust risk parameters accordingly.

7. Compliance and Regulatory Adherence

Continuous Regulatory Monitoring: Stay updated on changes in lending laws and regulations with Roopya platform, to ensure compliance across all stages of the loan origination process.

Compliance Training: Provide ongoing training for staff on regulatory requirements and compliance best practices to mitigate risk.

8. Customer Service and Support

Omnichannel Support: Offer support across various channels (phone, email, chat) to address borrower queries and concerns promptly.

Post-Loan Support: Engage with customers post-disbursement to collect feedback and offer support for any subsequent queries or issues.

9. Data Security and Privacy

Roopya platform prioritize the security and privacy of customer data with robust cybersecurity measures and compliance with data protection regulations.

10. Continuous Improvement and Feedback Loop

Customer Feedback: Platform regularly collects and analyses customer feedback to identify areas for improvement.

Process Optimization: Implement a continuous improvement culture, using data analytics to identify inefficiencies and optimize processes across the loan origination value chain.