End-to-End Digital Lending Software: LOS, LMS & KYC API Explained

Digital transformation has completely reshaped the lending ecosystem in India. From traditional paperwork-heavy processes to instant loan approvals, modern lenders now rely on Digital Lending Software to scale operations, reduce risk, and improve customer experience.

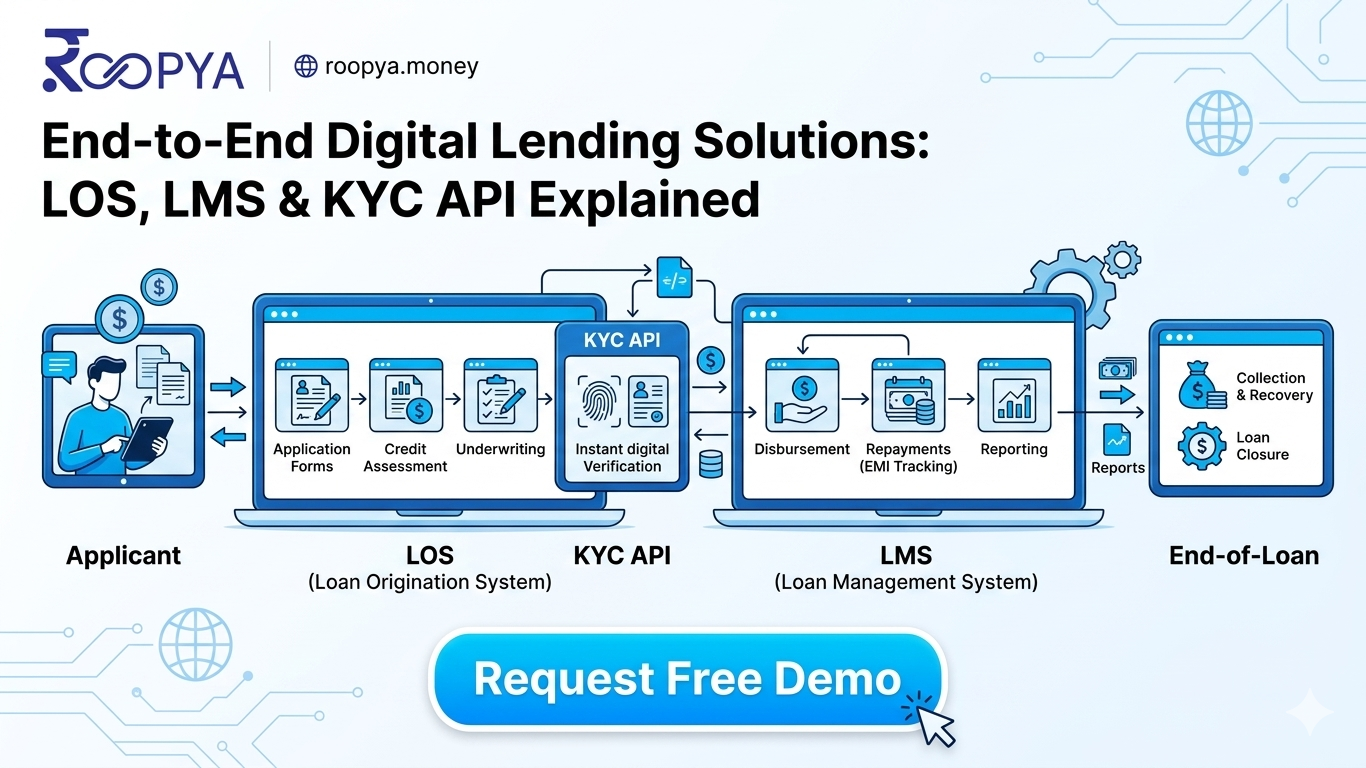

For NBFCs, fintech startups, and banks, an end-to-end digital lending solution integrates three critical components:

- Loan Origination System (LOS)

- Loan Management System (LMS)

- KYC API & Verification Tools

Together, these systems create a seamless, automated, and compliant lending lifecycle—from borrower onboarding to loan closure.

Start Free Trial

What is Digital Lending Software?

Digital lending software is a unified technology platform that automates the entire loan lifecycle—from application and verification to disbursement and repayment. It eliminates manual processes and enables real-time decision-making.

Modern platforms combine LOS, LMS, and API integrations into a single ecosystem, helping lenders:

- Reduce turnaround time (TAT)

- Improve credit decision accuracy

- Ensure RBI compliance

- Scale loan operations efficiently

According to industry insights, digital lending platforms allow lenders to move from application to disbursal within hours instead of days.

Understanding the Core Components

1. Loan Origination System (LOS)

A Loan Origination System (LOS) is the front-end engine of the lending process. It manages everything from loan application to approval and disbursement.

Key Features of LOS:

- Application intake and data capture

- Automated document verification

- Credit bureau integration (CIBIL, Experian)

- Risk scoring and underwriting

- KYC/AML compliance checks

- Approval workflows and decision engine

- Loan offer generation and disbursement

LOS digitizes and automates the entire origination journey, enabling faster approvals and better risk management.

Benefits of LOS:

- Instant loan approvals

- Reduced manual errors

- Improved fraud detection

- Seamless customer onboarding

Modern LOS platforms also use AI-based credit decisioning and real-time analytics to improve approval accuracy and reduce default risk.

2. Loan Management System (LMS)

Once a loan is disbursed, the Loan Management System (LMS) takes over. It handles the entire lifecycle of the loan until repayment or closure.

Key Features of LMS:

- EMI scheduling and repayment tracking

- Loan disbursement management

- Collections and recovery management

- NPA tracking and reporting

- Customer account management

- Real-time portfolio monitoring

LMS ensures smooth backend operations and helps lenders manage large loan portfolios efficiently.

Benefits of LMS:

- Automated loan servicing

- Better portfolio visibility

- Improved collection efficiency

- Compliance-ready reporting

3. KYC API & Verification Systems

KYC (Know Your Customer) APIs are essential for identity verification and fraud prevention in digital lending.

What is a KYC API?

A KYC API enables lenders to verify borrower identity instantly using government databases and digital documents.

Common KYC Integrations:

- Aadhaar verification

- PAN validation

- Video KYC

- CKYC and DigiLocker

- Bank statement analysis

KYC APIs are deeply integrated into LOS and LMS systems to ensure secure onboarding and compliance with RBI regulations.

Why KYC APIs Matter:

- Prevent fraud and identity theft

- Enable instant onboarding

- Ensure regulatory compliance

- Reduce operational costs

India’s digital lending ecosystem faces significant fraud risks, making KYC APIs critical for secure lending operations.

How LOS, LMS & KYC API Work Together

An end-to-end lending platform integrates LOS, LMS, and KYC APIs into a unified system.

Step-by-Step Loan Lifecycle:

- Application Submission (LOS)

- Borrower applies online

- Data captured digitally

- KYC Verification (API Integration)

- Aadhaar/PAN verification

- Fraud detection checks

- Credit Assessment (LOS)

- Risk scoring and underwriting

- Approval decision

- Loan Disbursement (LOS + LMS)

- Funds transferred to borrower

- Loan Servicing (LMS)

- EMI tracking and collections

- Customer support

- Closure (LMS)

- Loan repayment completion

- Account closure

This unified approach eliminates data silos and ensures seamless data flow across the lending lifecycle.

Why NBFCs Need End-to-End Lending Software

Traditional lending systems often rely on multiple disconnected tools, leading to inefficiencies and compliance risks.

Challenges Without Digital Lending Software:

- Manual paperwork and delays

- Data silos across systems

- Poor customer experience

- High operational costs

- Compliance risks

Advantages of Unified Lending Platforms:

- Single source of truth

- Faster loan approvals

- Improved borrower experience

- Reduced operational costs

- Scalability for growth

Modern NBFC software integrates all lending components into one platform, eliminating the need for multiple vendors.

Key Features to Look for in Lending Software

When choosing a Loan Software or NBFC Software, consider the following features:

1. API-First Architecture

- Easy integration with third-party services

- Scalable and flexible system design

2. Automation & AI

- Automated workflows

- AI-based credit decisioning

3. Compliance & Security

- RBI-compliant workflows

- Data encryption and audit trails

4. Customization

- Low-code/no-code configuration

- Multi-product support

5. Real-Time Analytics

- Portfolio insights

- Risk analysis dashboards

Use Cases of Digital Lending Software

1. NBFCs

- Personal loans

- Business loans

- Loan against property

2. Fintech Companies

- Instant digital loans

- BNPL (Buy Now Pay Later)

- Micro-lending

3. Payday Loan Providers

- Quick approval loans

- Short-term lending solutions

4. Banks

- Retail and corporate lending

- Co-lending partnerships

Why Choose Roopya for Digital Lending Solutions?

Roopya offers a complete end-to-end lending platform designed for NBFCs and fintech companies.

Key Highlights:

- Integrated LOS + LMS + KYC APIs

- 300+ API integrations

- AI-powered credit decisioning

- RBI-compliant workflows

- Fast deployment (go live in days)

Roopya eliminates the complexity of managing multiple systems by offering everything in one platform.

Request a Free Demo Today

Ready to transform your lending business?

Request a Free Demo Now

Discover how Roopya can help you:

- Launch faster

- Scale efficiently

- Reduce risk

- Improve customer experience

SEO Keywords Included

- Digital Lending Software

- NBFC Software

- Loan LMS

- Loan LOS

- Loan Software

- Lending Software

- Payday Loan Software

- LMS for NBFC

- KYC API