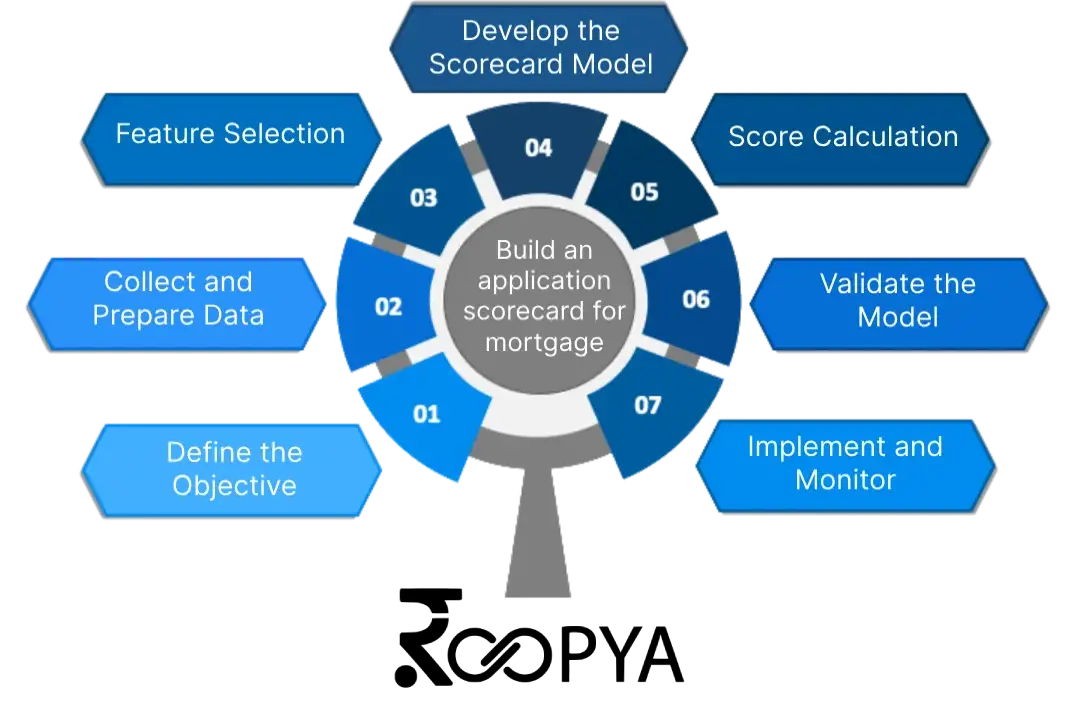

Roopya typically uses statistical modelling by using dataset of past loan applications with known outcomes (i.e., whether the loan was repaid or defaulted). Typical steps followed are:

Step 1: Define the Objective

The objective is to predict the likelihood of an applicant defaulting on a mortgage loan. This helps in decision-making regarding loan approvals and terms.

Step 2: Collect and Prepare Data

Gather historical data on mortgage applicants, including both those who have successfully repaid their loans and those who have defaulted. Key data points might include:

- Credit score (e.g., 300-850)

- Income (annual)

- Employment status (e.g., employed, self-employed, unemployed)

- Loan-to-value ratio (LTV)

- Debt-to-income ratio (DTI)

- Assets and savings

- Loan amount

- Property type (e.g., single-family etc)

Step 3: Feature Selection

Identify which variables (features) are most predictive of loan default. Statistical analysis and domain expertise can help in selecting the most relevant features.

Step 4: Develop the Scorecard Model

4.1 Split the Data

Divide your dataset into a training set (to build the model) and a test set (to validate the model).

4.2. Choose a Modelling Technique

Logistic regression is commonly used for binary outcomes like loan default (yes/no). However, other techniques such as decision trees or machine learning algorithms can also be applied.

4.3. Build the Model

Using the training set, develop a model that assigns weights (coefficients) to each of the selected features based on their ability to predict loan default.

Example:

- Credit Score: High scores reduce risk, so a higher credit score might subtract points from the default risk score.

- Debt-to-Income Ratio: Higher DTI increases risk, so a higher DTI might add points to the default risk score.

Step 5: Score Calculation

Create a scoring mechanism where each applicant is scored based on the model. For example, you might start with a base score of 100 and then add or subtract points based on the applicant’s features according to the model’s coefficients.

Step 6: Validate the Model

Test the model on the test set to evaluate its performance. We use metrics like accuracy, ROC AUC, and confusion matrices to assess how well the model predicts loan defaults.

Step 7: Implement and Monitor

Deploy the scorecard in the loan application process. Continuously monitor its performance and update the model as needed to adapt to changes in economic conditions or applicant behaviour.