Implementing Credit Risk Modelling Strategy

What is Credit Risk Modelling

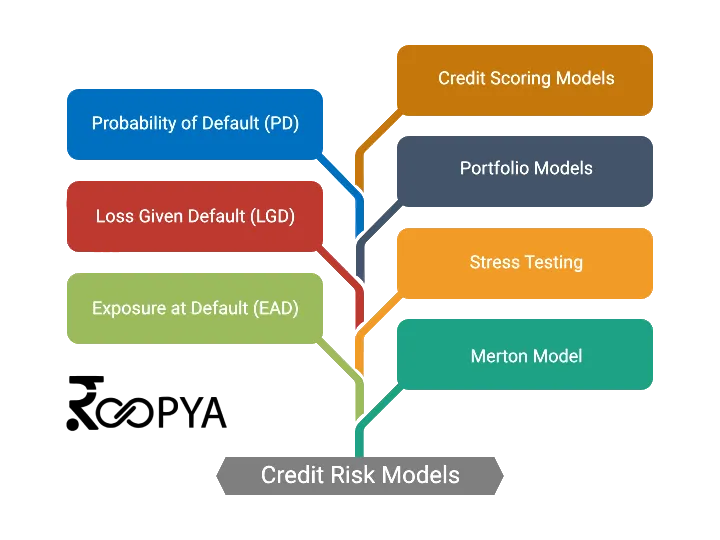

Roopya Credit risk modelling is a statistical approach implemented by financial institutions to estimate the likelihood of a borrower defaulting on their loan obligations. This complex process involves the use of statistical models to assess the creditworthiness of borrowers, incorporating a variety of factors including credit scores, loan-to-value ratios, debt-to-income ratios, and economic conditions. The most prevalent models in credit risk assessment are the Probability of Default (PD), Loss Given Default (LGD), and Exposure at Default (EAD) models. The PD model estimates the likelihood that a borrower will default within a specific timeframe, while the LGD model assesses the amount of loss a lender might face in the event of default, taking into consideration the recovery rate of the collateral. EAD models, on the other hand, estimate the total amount at risk at the time of default. These models are integral to the Basel Accords regulations, guiding banks in the allocation of capital to cushion against potential losses from credit risk. Advanced statistical techniques, including logistic regression, survival analysis, and machine learning algorithms, are employed to enhance the accuracy and predictive power of these models, enabling lenders to make more informed lending decisions and manage the risk associated with extending credit.

Start Free Trial