Introduction to Credit Scorecard

What is Credit Scorecard?

A credit scorecard is a statistical model used by lenders to evaluate the risk of lending money to consumers. It helps in determining the creditworthiness of an individual by scoring various aspects of their financial history and current financial status. The scorecard is designed to predict the likelihood that a borrower will repay a loan on time.

Start Free Trial

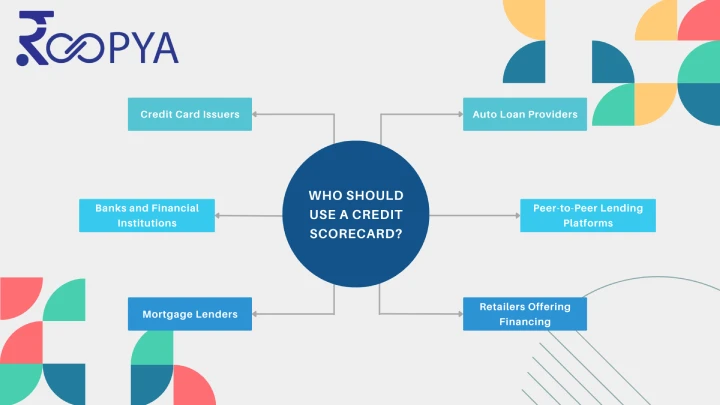

Who should use a Credit Scorecard?

Credit scorecards are essential tools for lenders to evaluate the financial health and creditworthiness of applicants and the following type of lenders use credit scorecards:

| Lender Types | Purpose of Using Credit Scorecard |

| Banks and Financial Institutions | To assess the creditworthiness of individuals for personal loans, mortgages, or credit lines. |

| Credit Card Issuers | For evaluating applications for new credit cards and determining credit limits and interest rates. |

| Auto Loan Providers | To decide on the approval and terms of car loans, including interest rates and down payment requirements. |

| Mortgage Lenders | To evaluate the risk of lending for home purchases and set loan terms like interest rates and amounts. |

| Retailers Offering Financing | For assessing the risk of offering instalment payments or personal lines of credit to customers. |

| Peer-to-Peer Lending Platforms | To assess borrower risk profiles and set interest rates on loans funded by individual investors. |