LMS vs Core Banking System: What Indian NBFCs Actually Need in 2026

India’s lending ecosystem is changing rapidly. From digital onboarding and AI-based underwriting to co-lending and RBI compliance, modern NBFCs are under pressure to scale faster while keeping operations efficient and compliant.

One of the biggest technology questions NBFCs face in 2026 is:

Start Free Trial

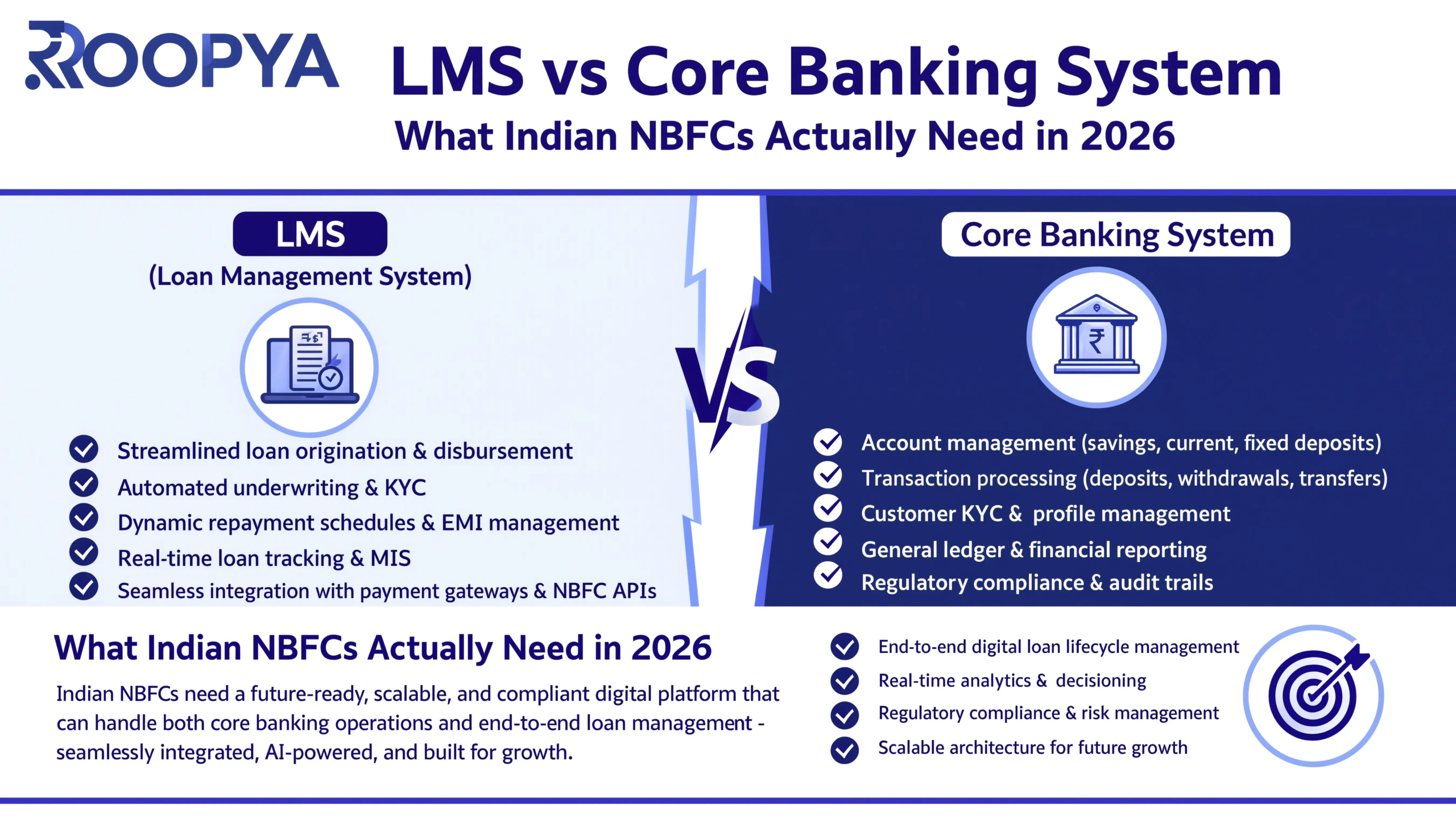

Should you use a Core Banking System (CBS) or a Loan Management System (LMS)?

Many lenders still assume both systems are the same. In reality, they serve very different purposes.

A Core Banking System is designed mainly for traditional banking operations such as deposits, savings accounts, branch banking, and internal financial management. On the other hand, a Loan Management System focuses entirely on the lending lifecycle — from loan disbursement and EMI collection to delinquency tracking, co-lending, and recovery automation.

For Indian NBFCs, fintech lenders, microfinance institutions, and digital lending startups, the choice can directly impact scalability, customer experience, compliance, and profitability.

In this guide, we will explain:

- What an LMS is

- What a Core Banking System is

- Key differences between LMS and CBS

- Why NBFCs prefer LMS platforms in 2026

- RBI compliance considerations

- Integration requirements

- Cost comparison

- Which solution is best for your lending business

What Is a Loan Management System (LMS)?

A Loan Management System (LMS) is software specifically designed to manage the entire post-loan lifecycle.

It helps NBFCs automate:

- Loan servicing

- EMI schedules

- Collections

- NACH/UPI autopay

- DPD tracking

- Recovery workflows

- Customer communication

- Compliance reporting

- Portfolio analytics

- Co-lending operations

Modern LMS platforms like those offered by Roopya Money are cloud-based, API-first, and designed for digital lending operations.

Key Functions of an LMS

Loan Account Management

Manage thousands or millions of active loans from a centralized dashboard.

EMI Scheduling

Automatically generate EMI calendars based on:

- Reducing balance

- Flat interest

- Daily interest

- Weekly repayment

- Bullet loans

Collection Automation

Automate repayment collection using:

- NACH

- UPI Autopay

- eMandates

- Payment gateways

- WhatsApp reminders

- SMS alerts

DPD & Delinquency Tracking

Monitor overdue accounts in real-time using:

- Bucket classification

- Risk segmentation

- Recovery prioritization

RBI Compliance

Generate:

- Audit logs

- Bureau reports

- Regulatory reports

- Consent tracking

- Digital lending records

Co-Lending Support

Support multi-lender loan participation and revenue sharing.

Analytics & Reporting

Track:

- Portfolio health

- NPA trends

- Collection efficiency

- Risk indicators

- Geographic performance

What Is a Core Banking System (CBS)?

A Core Banking System (CBS) is centralized banking software primarily used by banks.

CBS platforms are designed to handle:

- Savings accounts

- Current accounts

- Deposits

- Treasury

- Branch banking

- Internal accounting

- Customer records

- Interbank transactions

CBS became essential when banks moved from branch-based operations to centralized digital banking systems.

Large banks in India rely heavily on CBS platforms for daily operations.

However, many NBFCs mistakenly adopt CBS platforms even when they only require lending functionality.

Why CBS Was Popular Earlier

Before digital lending became mainstream, many NBFCs used lightweight banking systems because:

- Loan volumes were smaller

- Collections were manual

- Compliance requirements were simpler

- APIs were uncommon

- Mobile lending did not exist

In 2026, lending businesses operate very differently.

Today’s NBFCs require:

- Real-time APIs

- AI-driven workflows

- Instant onboarding

- Embedded finance

- Automated collections

- RBI digital compliance

- Co-lending infrastructure

Traditional CBS platforms often struggle to support these requirements efficiently.

LMS vs Core Banking System: Key Differences

| Feature | LMS | Core Banking System |

| Primary Focus | Lending operations | Banking operations |

| Best For | NBFCs & fintechs | Banks |

| EMI Management | Advanced | Limited |

| Collection Automation | Strong | Basic |

| DPD Tracking | Real-time | Often manual |

| Co-Lending | Supported | Limited |

| API Integrations | Extensive | Moderate |

| Loan Analytics | Advanced | General |

| Customer Journeys | Digital-first | Branch-first |

| RBI Digital Lending Compliance | Specialized | Partial |

| Cloud Deployment | Common | Less flexible |

| Scalability for Lending | High | Moderate |

| Mobile Lending | Optimized | Not optimized |

| Recovery Workflows | Automated | Limited |

Why Indian NBFCs Prefer LMS Platforms in 2026

The Indian lending market has evolved dramatically due to:

- UPI growth

- Embedded finance

- Digital KYC

- GST-based underwriting

- Account Aggregator framework

- RBI digital lending regulations

Because of these changes, NBFCs require lending-focused technology instead of generic banking software.

-

Faster Loan Processing

Modern LMS platforms automate:

- Repayment setup

- Loan servicing

- Disbursement reconciliation

- Customer notifications

This reduces operational workload significantly.

-

Better Collection Efficiency

Collections are the heart of NBFC profitability.

A good LMS enables:

- Auto-debit management

- Bounce handling

- DPD alerts

- Recovery assignment

- Field collection tracking

Without these capabilities, lenders face rising NPAs.

-

Digital Lending Compliance

RBI’s digital lending regulations require lenders to maintain:

- Transparent borrower communication

- Consent records

- Audit trails

- Data protection

- Recovery monitoring

LMS platforms are specifically designed for these workflows.

-

Easier Integration Ecosystem

NBFCs now rely heavily on integrations such as:

- Aadhaar KYC

- PAN verification

- Bureau checks

- GST APIs

- Account Aggregator

- Payment gateways

- WhatsApp APIs

An API-first LMS simplifies integration management.

When Does an NBFC Need a Core Banking System?

Although LMS platforms are ideal for lending operations, some institutions may still require CBS capabilities.

You May Need CBS If:

You Handle Deposits

Deposit-taking NBFCs may require banking-grade accounting systems.

You Operate Like a Full Bank

Institutions offering:

- Savings products

- Current accounts

- Treasury services

may benefit from CBS infrastructure.

Complex Internal Accounting

Large financial institutions sometimes integrate CBS for enterprise-level accounting.

However, even these organizations increasingly combine:

- CBS for banking

- LMS for lending

instead of relying on CBS alone.

Why LMS Is Better for Digital Lending Startups

Indian fintechs prioritize:

- Speed

- Scalability

- Automation

- API integrations

- Mobile-first experiences

Traditional CBS systems are often:

- Expensive

- Slow to customize

- Difficult to integrate

- Not optimized for embedded lending

An LMS platform allows startups to launch lending products quickly.

Cloud LMS vs Traditional CBS

Cloud LMS Advantages

Lower Infrastructure Cost

No expensive hardware setup.

Faster Deployment

Launch within weeks instead of months.

Automatic Updates

Compliance and feature updates happen automatically.

Better Scalability

Scale from 1,000 loans to 10 lakh+ loans efficiently.

Remote Accessibility

Teams can work from anywhere securely.

RBI Compliance Requirements in 2026

Modern NBFCs must comply with RBI requirements related to:

- Digital lending transparency

- Bureau reporting

- Data security

- KYC tracking

- Consent management

- Collection governance

An LMS helps automate compliance operations.

Essential Compliance Features

Audit Logs

Every action must be traceable.

Consent Capture

Borrower approvals must be recorded.

Collection Monitoring

Recovery activities must remain compliant.

Data Encryption

Sensitive borrower data must be protected.

Credit Bureau Integration

Regular reporting is mandatory.

Key LMS Features Every NBFC Needs

Automated EMI Collection

The system should support:

- NACH

- UPI Autopay

- Payment links

- QR collections

Delinquency Management

Advanced DPD tracking helps reduce NPAs.

Recovery Workflow Automation

Assign cases automatically based on:

- Region

- Bucket

- Risk level

Customer Self-Service

Borrowers should access:

- Loan statements

- Repayment history

- Payment options

Real-Time Dashboards

Management teams require instant visibility into:

- Portfolio performance

- Collection ratios

- Recovery trends

Integration Requirements for Modern NBFCs

A modern LMS should integrate with:

| Integration Type | Purpose |

| CKYC APIs | Customer verification |

| Bureau APIs | Credit checks |

| GST APIs | MSME underwriting |

| Account Aggregator | Bank data access |

| Payment Gateways | EMI collection |

| WhatsApp APIs | Notifications |

| E-sign APIs | Digital agreements |

| Video KYC | Compliance |

Cost Comparison: LMS vs CBS

LMS Cost

Modern cloud LMS pricing usually depends on:

- Loan volume

- Active users

- API usage

- Modules selected

Typical Range

₹50,000 to ₹15 lakh+ annually depending on scale.

CBS Cost

CBS implementation often includes:

- License fees

- Hardware setup

- Customization

- Maintenance

- Integration costs

Typical Range

₹25 lakh to several crores.

For most NBFCs, CBS becomes unnecessarily expensive.

Challenges of Using CBS for Lending

Poor Lending Flexibility

Many CBS platforms were designed decades ago and struggle with:

- BNPL

- Embedded lending

- Instant loans

- Co-lending

Slow Product Launch

Launching new loan products may require lengthy development cycles.

Weak Collection Tools

CBS systems usually lack advanced:

- Recovery workflows

- DPD automation

- Field collection management

Hybrid Approach: LMS + CBS

Some large institutions use a hybrid architecture:

| System | Role |

| CBS | Banking & accounting |

| LMS | Lending operations |

This approach combines:

- Enterprise-grade finance management

- Modern lending automation

However, for most NBFCs, a standalone LMS is sufficient.

Use Cases by Lending Segment

Personal Loan NBFCs

Need:

- Fast approvals

- EMI automation

- Collection analytics

Best Fit: LMS

MSME Lenders

Need:

- GST underwriting

- Bank statement analysis

- Working capital workflows

Best Fit: LMS

Gold Loan Companies

Need:

- LTV tracking

- Branch workflows

- Auction management

Best Fit: LMS

Microfinance Institutions

Need:

- Group collections

- Weekly EMI tracking

- Field recovery tools

Best Fit: LMS

Large Banks

Need:

- Deposit systems

- Treasury

- Branch operations

Best Fit: CBS + LMS

Future of Lending Technology in India

The future of Indian lending will be driven by:

- AI underwriting

- Embedded finance

- Open banking

- Account Aggregator ecosystem

- Real-time collections

- Predictive risk analytics

These innovations require highly flexible lending infrastructure.

This is why most fintech lenders are moving toward API-first LMS platforms instead of traditional banking systems.

How Roopya Money Helps NBFCs Scale

Roopya Money provides advanced digital lending solutions designed specifically for Indian NBFCs and fintech companies.

Key Solutions

Loan Management System

Automate servicing, collections, DPD management, and reporting.

Loan Origination System

Digitize onboarding, KYC, underwriting, and approvals.

Collection System

Improve recovery efficiency using automated workflows.

Early Warning System

Detect risky accounts before they become NPAs.

Lending Analytics

Gain portfolio-level visibility using real-time dashboards.

API Integrations

Connect with bureau, GST, AA, CKYC, payment, and e-sign providers.

Final Verdict: LMS or Core Banking System?

For most Indian NBFCs in 2026, the answer is clear.

If your business focuses mainly on lending, collections, digital onboarding, and portfolio management, a modern Loan Management System is the better choice.

A Core Banking System may still be necessary for full-service banks or large deposit-taking institutions, but it is not optimized for modern digital lending operations.

An LMS provides:

- Faster deployment

- Better lending automation

- Lower cost

- Stronger compliance support

- Better scalability

- Modern API ecosystem

- Improved borrower experience

As India’s lending market becomes more digital and compliance-driven, NBFCs need technology built specifically for lending — not legacy banking infrastructure.

The Indian lending market in 2026 demands speed, automation, compliance, and scalability. Traditional Core Banking Systems were not designed for today’s digital-first lending ecosystem.

A modern Loan Management System empowers NBFCs to:

- Automate operations

- Improve collections

- Launch products faster

- Stay compliant

- Scale efficiently

For lenders looking to modernize operations and grow competitively, investing in the right LMS platform is no longer optional — it is essential.

To explore digital lending solutions for your NBFC, visit: Roopya Money