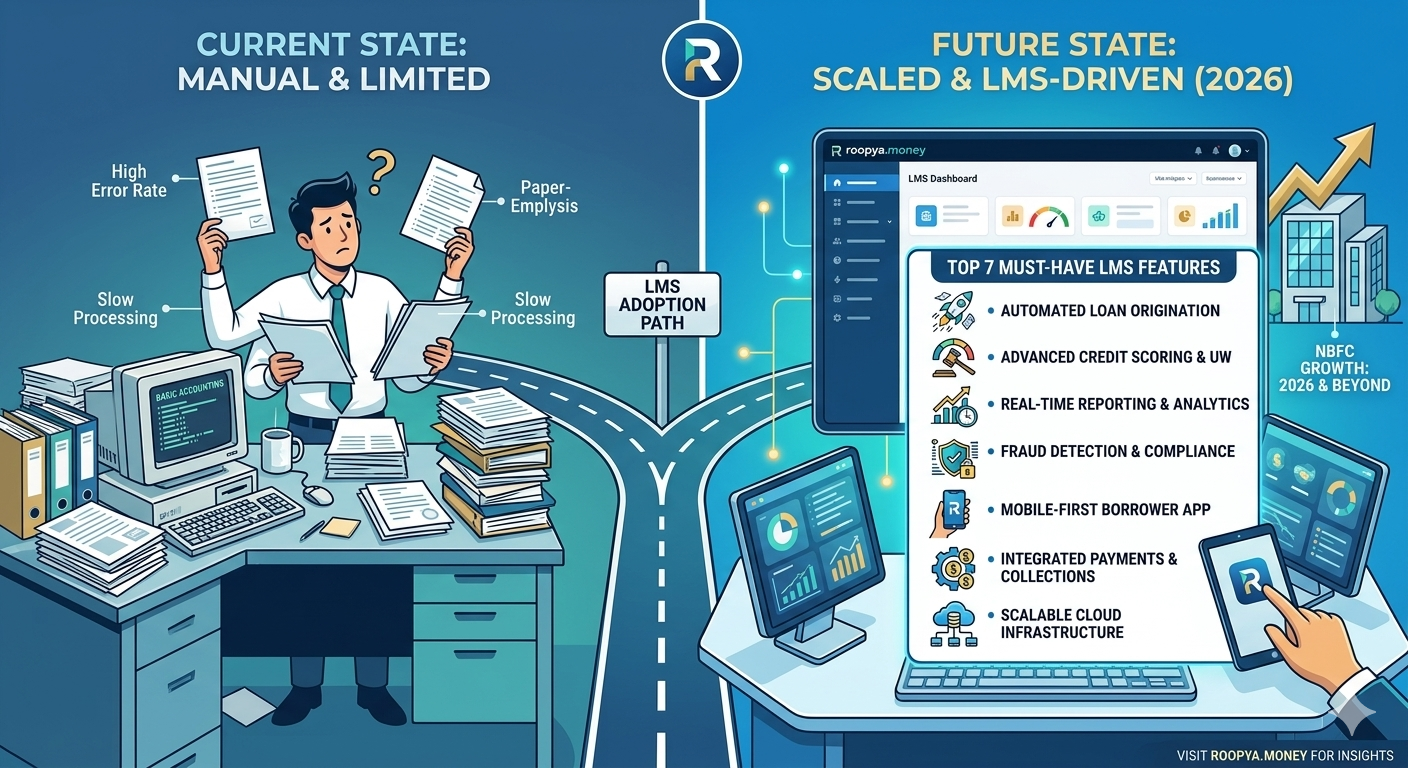

Top 7 Loan Management System Features Every NBFC Must Have Before Scaling in 2026

India’s lending industry is evolving faster than ever before.

From digital-first NBFCs and embedded lending startups to MSME lenders and co-lending partnerships, the lending ecosystem in 2026 looks completely different from what it was just a few years ago.

Today’s borrowers expect:

- Instant approvals

- Digital onboarding

- Real-time loan tracking

- Seamless EMI repayment

- Mobile-first experiences

At the same time, NBFCs face increasing pressure from:

- RBI compliance requirements

- Rising operational costs

- Higher competition

- Fraud risks

- NPA management challenges

- Complex collection workflows

Start Free Trial

This is why modern lenders are investing heavily in scalable Loan Management Systems (LMS).

A basic loan servicing platform is no longer enough.

Before scaling operations in 2026, every NBFC must ensure its LMS supports:

- Automation

- Real-time analytics

- API integrations

- AI-powered workflows

- Digital collections

- RBI compliance

- Multi-product lending

According to industry analysis, Indian NBFCs are increasingly shifting toward cloud-native LMS platforms that combine LOS, collections, analytics, and compliance into a single ecosystem.

This guide explains the Top 7 LMS Features Every NBFC Must Have Before Scaling in 2026.

Why Choosing the Right LMS Matters in 2026

Scaling a lending business without the right technology stack creates major operational risk.

Many growing NBFCs still rely on:

- Excel sheets

- Manual reconciliation

- Legacy software

- Disconnected systems

As loan volumes increase, these outdated processes lead to:

- Delayed collections

- Higher NPAs

- Compliance failures

- Customer dissatisfaction

- Poor portfolio visibility

A modern Loan Management System becomes the operational backbone of the lending business.

It manages:

- EMI servicing

- Collections

- Repayment schedules

- DPD tracking

- Recovery workflows

- Accounting

- Compliance reporting

- Analytics

- Customer communication

Modern LMS platforms also support AI-driven automation and real-time integrations with India’s growing digital finance ecosystem.

What Is a Loan Management System (LMS)?

A Loan Management System is software that manages the post-disbursement lifecycle of a loan.

It helps lenders automate:

- Loan servicing

- Repayment collection

- Customer communication

- Delinquency management

- Recovery operations

- Reporting and compliance

Modern LMS platforms are cloud-based, API-first, and designed specifically for digital lending businesses.

Platforms like Roopya Money provide integrated:

- LMS

- LOS

- Collection management

- Early warning systems

- Lending analytics

- RBI-compliant workflows

for Indian NBFCs and fintech companies.

The Future of NBFC Lending Technology

The Indian lending market is moving rapidly toward:

- AI underwriting

- Embedded finance

- Co-lending

- Account Aggregator integration

- Real-time bureau reporting

- API-driven collections

- Predictive analytics

This means NBFCs need scalable lending infrastructure instead of traditional software systems.

Industry reports show strong growth in demand for integrated LMS + LOS platforms due to rising digital lending adoption and regulatory expectations.

Feature 1: Automated EMI Collection & Recovery Management

Collections are the heart of every lending business.

An NBFC can disburse thousands of loans, but without efficient collections, portfolio quality deteriorates quickly.

This is why automated collections are the most important LMS feature in 2026.

Why Manual Collections Fail

Manual collection systems create several problems:

- Missed follow-ups

- Delayed payment reminders

- Poor DPD visibility

- High recovery cost

- Compliance risks

As portfolios scale, manual recovery operations become unsustainable.

What a Modern Collection Engine Should Support

A scalable LMS must automate:

NACH Management

Automate recurring EMI debit workflows.

UPI Autopay

Enable mobile-first repayment experiences.

Payment Gateway Integration

Accept:

- Cards

- Net banking

- Wallets

- QR payments

DPD Tracking

Monitor delinquency in real time.

Automated Reminders

Send:

- SMS alerts

- WhatsApp reminders

- Email notifications

Recovery Workflow Allocation

Assign cases automatically to:

- Call center agents

- Field recovery teams

- Legal departments

Importance of DPD-Based Automation

DPD (Days Past Due) tracking helps lenders identify risk early.

Modern LMS platforms automatically trigger actions based on:

- 1 DPD

- 5 DPD

- 30 DPD

- 90+ DPD

This improves collection efficiency significantly.

Why This Feature Matters Before Scaling

Without automated collections:

- NPAs rise rapidly

- Recovery teams become inefficient

- Operational cost increases

- Cash flow suffers

A scalable LMS must manage lakhs of repayment transactions efficiently.

Feature 2: RBI Compliance & Audit-Ready Infrastructure

The Reserve Bank of India has significantly tightened digital lending regulations.

In 2026, compliance is no longer optional.

NBFCs must maintain:

- Audit trails

- Consent records

- Recovery governance

- Bureau reporting

- Data protection

- Transparent borrower communication

Key Compliance Features Every LMS Must Have

Audit Logs

Every borrower activity must be traceable.

Consent Management

Track borrower approvals digitally.

Data Encryption

Protect sensitive customer information.

Bureau Reporting

Automate credit bureau submissions.

Recovery Governance

Ensure compliant collection practices.

Regulatory Reporting

Generate RBI-ready reports automatically.

Risks of Weak Compliance Infrastructure

Without proper compliance systems, lenders face:

- Regulatory penalties

- Customer disputes

- Legal exposure

- Operational risk

A compliance-ready LMS reduces these risks significantly.

Why Compliance Automation Matters

Manual compliance tracking becomes impossible at scale.

An advanced LMS automates:

- Logs

- Reports

- Consent tracking

- Monitoring workflows

This is essential for growing NBFCs.

Feature 3: API-First Integration Ecosystem

Modern lending is powered by APIs.

Today’s NBFCs rely on multiple external systems for:

- KYC

- Credit checks

- GST verification

- Bank statement analysis

- Payments

- Fraud detection

A modern LMS must integrate seamlessly with India’s digital finance ecosystem.

Industry analysis highlights that API integration coverage is now one of the most critical criteria when evaluating LMS platforms in India.

Essential APIs Every LMS Should Support

| API Type | Purpose |

|---|---|

| CKYC APIs | Customer verification |

| Bureau APIs | Credit scoring |

| GST APIs | MSME underwriting |

| Account Aggregator APIs | Bank data access |

| eSign APIs | Digital agreements |

| Payment APIs | EMI collection |

| Video KYC APIs | Compliance onboarding |

| Fraud APIs | Risk monitoring |

Why API Flexibility Matters

Without integrations, lenders face:

- Delayed onboarding

- Manual verification

- Poor customer experience

- Operational inefficiency

Modern cloud LMS platforms now offer 300+ integrations for lenders.

Feature 4: AI-Powered Analytics & Risk Intelligence

AI is transforming lending operations in India.

Modern NBFCs use AI for:

- Credit scoring

- Fraud detection

- Collection prioritization

- Portfolio forecasting

- Delinquency prediction

An LMS without analytics capabilities will struggle in 2026.

Important AI Features in Modern LMS Platforms

Early Warning System (EWS)

Detect high-risk borrowers before default occurs.

Predictive DPD Analysis

Forecast delinquency trends.

Collection Prioritization

Focus recovery efforts on high-risk accounts.

Fraud Detection

Identify suspicious applications and transactions.

Portfolio Analytics

Track:

- NPA trends

- Geographic performance

- Product performance

- Recovery efficiency

Why AI Matters Before Scaling

As loan portfolios grow:

- Risk complexity increases

- Fraud exposure rises

- Collection challenges expand

AI-driven systems improve decision-making and reduce operational cost.

Feature 5: Co-Lending & Multi-Partner Lending Support

Co-lending is one of the biggest trends in Indian lending.

Banks and NBFCs increasingly collaborate to:

- Share risk

- Expand reach

- Improve capital efficiency

However, co-lending creates major operational complexity.

What a Co-Lending LMS Must Handle

Multi-Lender Accounting

Track lender participation accurately.

Revenue Sharing

Split interest and fees automatically.

EMI Split Logic

Allocate repayments correctly.

Partner Reporting

Generate institution-specific MIS reports.

Compliance Tracking

Maintain audit-ready workflows.

Reddit discussions among Indian fintech professionals highlight that native co-lending support is now one of the biggest differentiators between modern LMS platforms.

Why Co-Lending Support Matters

NBFCs planning aggressive growth increasingly rely on:

- Bank partnerships

- Embedded finance

- Marketplace lending

A scalable LMS must support these ecosystems.

Feature 6: No-Code Product Configuration

Traditional lending software requires developers for every change.

This creates:

- Slow product launches

- High IT dependency

- Delayed innovation

In 2026, no-code LMS platforms are becoming essential.

What No-Code LMS Means

Business teams can configure:

- Loan products

- Interest rates

- Repayment schedules

- Eligibility rules

- DPD logic

- Collection workflows

without developer support.

Benefits of No-Code Lending Infrastructure

Faster Product Launch

Launch products in days instead of months.

Lower IT Cost

Reduce developer dependency.

Better Agility

Adapt quickly to market demand.

Faster Compliance Updates

Respond quickly to RBI changes.

Industry comparisons show that no-code platforms significantly reduce deployment time and operational complexity for Indian lenders.

Feature 7: Cloud-Native Scalability & Real-Time Performance

Cloud infrastructure is now the default choice for modern NBFCs.

Traditional on-premise systems struggle with:

- Scalability

- Remote accessibility

- API integrations

- Real-time processing

Why Cloud LMS Is Dominating in 2026

Faster Deployment

Go live quickly.

Lower Infrastructure Cost

Reduce server and maintenance expenses.

Easier Scalability

Support rapid portfolio growth.

Better Disaster Recovery

Improve operational resilience.

Real-Time Accessibility

Enable remote operations securely.

Industry reports show strong growth in cloud-based LMS adoption among Indian NBFCs because of lower cost and faster scalability.

Additional Features That Matter in 2026

Beyond the top 7 features, lenders should also evaluate:

Borrower Self-Service Portal

Allow customers to:

- Download statements

- Pay EMIs

- Raise support requests

Mobile Collection App

Enable field recovery operations digitally.

Multi-Product Lending

Support:

- MSME loans

- Gold loans

- BNPL

- Personal loans

- Vehicle loans

Embedded Lending Support

Enable API-based partner lending.

Signs Your Current LMS Cannot Scale

Your LMS may need replacement if:

- Collections are manual

- Reporting takes days

- APIs are limited

- Product launches are slow

- Recovery tracking is weak

- Co-lending is unsupported

- Compliance workflows are manual

These limitations create major scaling bottlenecks.

How Roopya Money Helps NBFCs Scale in 2026

Roopya Money provides advanced digital lending infrastructure for Indian NBFCs and fintech lenders.

Core Solutions

Loan Management System

Automate:

- Servicing

- Collections

- DPD management

- Repayment tracking

Loan Origination System

Digitize:

- Onboarding

- KYC

- Underwriting

- Disbursement

Collection Management System

Improve recovery efficiency using:

- DPD workflows

- Field recovery

- AI prioritization

Early Warning System

Predict potential NPAs early.

Lending Analytics

Gain portfolio-level visibility using real-time dashboards.

300+ API Integrations

Connect seamlessly with:

- Bureau APIs

- Payment gateways

- Account Aggregator

- GST systems

- CKYC

- eSign providers

Roopya’s no-code lending infrastructure and cloud-native architecture are designed specifically for India’s rapidly evolving NBFC ecosystem.

Future of Loan Management Systems in India

The next generation of LMS platforms will focus heavily on:

- AI automation

- Embedded finance

- Real-time underwriting

- Predictive collections

- API ecosystems

- Hyper-personalized lending

NBFCs that continue relying on legacy systems may struggle to compete.

Final Thoughts

Scaling an NBFC in 2026 requires much more than loan disbursement capability.

Modern lenders need Loan Management Systems that support:

- Automated collections

- RBI compliance

- AI-driven analytics

- API integrations

- Co-lending

- No-code configuration

- Cloud scalability

The right LMS helps NBFCs:

- Reduce operational cost

- Improve collections

- Minimize fraud

- Stay compliant

- Launch products faster

- Scale efficiently

As India’s lending ecosystem becomes increasingly digital and competitive, investing in a scalable LMS is no longer optional — it is a strategic necessity.

To explore modern lending infrastructure for your NBFC or fintech company, visit:Roopya Money