LOS to LMS: How Data Gets Corrupted Between Origination and Servicing

The modern lending ecosystem runs on data. Every borrower interaction, underwriting decision, repayment schedule, and collection workflow depends on accurate information flowing seamlessly between systems. Yet for many NBFCs, banks, MFIs, and fintech lenders, one of the biggest hidden operational risks lies in the transition between the Loan Origination System (LOS) and the Loan Management System (LMS).

Start Free Trial

The LOS is responsible for capturing applications, verifying documents, underwriting loans, approving borrowers, and initiating disbursement. The LMS takes over after disbursement and manages repayment schedules, interest accrual, collections, foreclosure, restructuring, and portfolio servicing. While these systems represent different stages of the lending lifecycle, the data flowing between them must remain perfectly synchronized.

Unfortunately, this is where many lenders experience major breakdowns.

Data corruption between origination and servicing is not always dramatic or obvious. Sometimes it begins with a missing field, inconsistent borrower profile, duplicated account number, incorrect repayment schedule, or broken API mapping. Over time, these small inconsistencies compound into operational chaos, compliance risk, reconciliation failures, customer complaints, and even RBI scrutiny.

For lenders scaling rapidly in India’s digital lending ecosystem, the consequences can be severe:

- Incorrect EMI schedules

- Wrong interest calculations

- NPA classification errors

- Failed NACH collections

- Duplicate loan records

- Broken co-lending reconciliations

- Customer servicing disputes

- Regulatory reporting inaccuracies

The problem becomes even more dangerous when LOS and LMS systems come from different vendors and rely on fragile integrations. According to lending industry discussions, many NBFCs discover these gaps only after their portfolio reaches scale.

This article explains:

- Why data corruption happens between LOS and LMS

- The most common technical and operational failure points

- The financial and compliance impact on lenders

- Warning signs that your lending stack is failing

- Best practices to prevent data inconsistencies

- Why unified lending infrastructure is becoming essential for modern lenders

Understanding the LOS to LMS Handover

A loan lifecycle has two major operational phases.

Phase 1: Loan Origination (LOS)

The Loan Origination System manages:

- Lead capture

- Application intake

- KYC verification

- Bureau pulls

- Bank statement analysis

- Credit scoring

- Underwriting

- Approval workflows

- Sanction generation

- Disbursement initiation

The primary objective of the LOS is to transform an application into an approved and disbursed loan quickly and accurately.

Phase 2: Loan Servicing (LMS)

Once the loan is disbursed, the LMS becomes the operational backbone of the portfolio. It handles:

- Loan account creation

- EMI schedules

- Interest accrual

- Repayment processing

- NACH reconciliation

- Delinquency tracking

- Collections workflows

- Restructuring

- Foreclosure

- RBI reporting

This servicing layer continues for the entire life of the loan.

The transition between these two systems is one of the most critical events in lending infrastructure.

If the handover fails, the lender’s operational integrity begins to break down immediately.

What Does “Data Corruption” Actually Mean?

Data corruption between LOS and LMS does not always mean total data loss. In lending operations, corruption usually refers to inconsistencies, inaccuracies, or synchronization failures between systems.

Examples include:

- Borrower names mismatching across systems

- Loan tenure differing between LOS and LMS

- EMI dates shifting incorrectly

- Interest rates not updating properly

- Missing repayment schedules

- Duplicate customer IDs

- Partial disbursement records

- Broken payment mappings

- Incorrect co-lending partner allocations

- Invalid DPD calculations

Even a small discrepancy can create major downstream issues.

For example:

A loan approved in the LOS for 24 months at 16% interest may accidentally enter the LMS as 18 months at 18% due to mapping logic errors. That single mistake affects:

- EMI calculations

- Collection schedules

- Interest accrual

- Customer statements

- NPA recognition

- Regulatory reporting

At scale, these errors become operationally catastrophic.

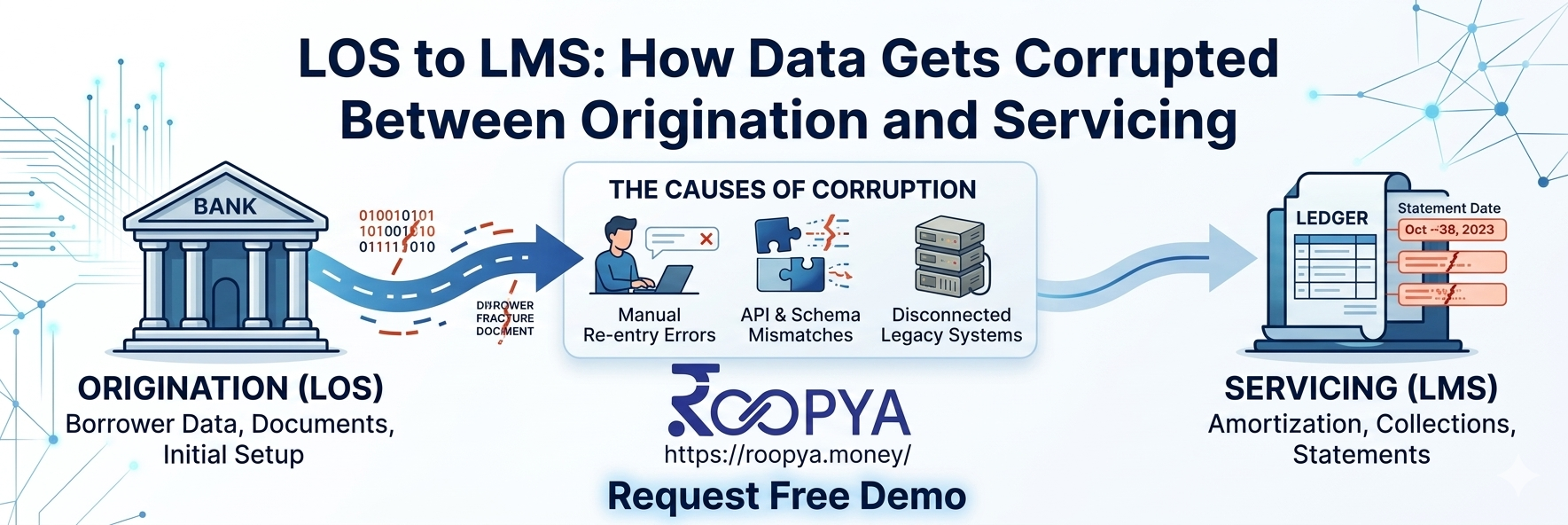

Why Data Gets Corrupted Between LOS and LMS

1. Separate Vendors Using Different Data Models

This is the most common problem in Indian lending infrastructure.

Many lenders buy:

- LOS from Vendor A

- LMS from Vendor B

- Collections software from Vendor C

- Analytics platform from Vendor D

Each platform stores and structures data differently.

One system may define:

- Borrower ID format differently

- Repayment structures differently

- Product rules differently

- Interest calculation logic differently

As a result, integrations require extensive middleware transformations and mapping layers.

Every transformation introduces risk.

Industry experts frequently warn that separate LOS and LMS vendors create brittle integration architectures that eventually fail under operational scale.

2. Incomplete API Integrations

Many lenders assume APIs automatically guarantee clean synchronization.

They do not.

Poorly designed APIs often:

- Skip optional fields

- Fail silently during outages

- Create duplicate records

- Ignore validation mismatches

- Process asynchronous updates incorrectly

For example:

- The LOS may update borrower income.

- The LMS never receives the update.

- Collections workflows still operate on old risk assumptions.

Without proper event synchronization, data divergence becomes inevitable.

3. Manual Data Entry and Excel Dependencies

Many mid-sized lenders still rely heavily on manual operations.

Operations teams often:

- Export LOS data into Excel

- Reformat fields manually

- Upload CSVs into LMS systems

- Correct records manually during reconciliation

This introduces:

- Human errors

- Formatting inconsistencies

- Missing fields

- Incorrect repayment mappings

Spreadsheets become especially dangerous beyond a few hundred active loans.

4. Product Configuration Mismatches

Loan products evolve constantly.

Lenders modify:

- Interest structures

- Tenure logic

- Moratorium policies

- Co-lending rules

- EMI frequencies

- Penal interest formulas

If LOS and LMS product configurations are updated independently, inconsistencies emerge rapidly.

For example:

- LOS launches a daily EMI product.

- LMS still assumes monthly EMI logic.

- Repayment schedules become inaccurate immediately.

Experts evaluating LMS platforms specifically warn that daily EMI handling is a major hidden risk area in Indian lending operations.

5. Inconsistent Validation Rules

The LOS may validate:

- PAN format

- Aadhaar details

- KYC completeness

- Bank account verification

But if the LMS lacks equivalent validations, corrupted or incomplete records can still enter servicing workflows.

This creates operational fragmentation where:

- Origination data is “clean”

- Servicing data becomes unreliable

6. Partial Disbursement Failures

Disbursement is the exact handover moment between LOS and LMS.

If:

- Payment gateway confirmations fail

- Banking APIs timeout

- NACH setup remains incomplete

- Loan account creation is delayed

Then the lender may face:

- Disbursed funds without active servicing records

- Active servicing accounts without successful disbursement

- Duplicate repayment schedules

This creates reconciliation nightmares.

7. Legacy Infrastructure Limitations

Older LMS platforms were designed for traditional branch-led lending environments.

Modern digital lending introduces:

- Instant underwriting

- Real-time APIs

- Embedded finance

- Multi-channel onboarding

- Co-lending workflows

- Dynamic risk pricing

Legacy servicing systems often struggle to process these modern origination structures accurately.

The Real Cost of Data Corruption

Operational Cost

Operations teams spend thousands of hours:

- Reconciling ledgers

- Fixing repayment schedules

- Resolving customer complaints

- Correcting DPD records

- Manually updating accounts

As loan books scale, these inefficiencies become unsustainable.

Financial Losses

Data inconsistencies directly impact:

- Interest income

- Collection efficiency

- Cash flow forecasting

- NPA recognition

- Provisioning accuracy

Even small servicing errors create revenue leakage across large portfolios.

Compliance Risk

The RBI’s digital lending environment is becoming increasingly strict around:

- KYC accuracy

- Reporting transparency

- Borrower disclosures

- Repayment accounting

- Co-lending reconciliation

Incorrect servicing data can expose lenders to:

- Audit observations

- Regulatory penalties

- Consumer disputes

- Legal escalation

Industry discussions repeatedly highlight regulatory risk from fragmented lending infrastructure.

Customer Experience Damage

Borrowers quickly lose trust when:

- EMI amounts change unexpectedly

- Payment records disappear

- Statements contain errors

- Foreclosure amounts mismatch

- Collections teams use incorrect balances

Poor servicing experiences damage:

- Brand reputation

- Retention

- Repeat borrowing

- Referral growth

Common Warning Signs Your LOS and LMS Are Breaking

Lenders should watch for these operational signals:

Frequent Manual Reconciliation

If your finance or operations team spends days reconciling:

- EMI collections

- Loan balances

- DPD status

- NACH failures

Then your data flow is already fragmented.

Increasing Customer Complaints

Repeated complaints around:

- Payment mismatches

- EMI confusion

- Incorrect overdue status

- Loan closure disputes

Often indicate deeper system synchronization failures.

Duplicate Loan Records

This usually indicates:

- Broken API retries

- Failed transaction handling

- Inconsistent borrower IDs

Duplicate records create massive downstream accounting issues.

Delayed Month-End Closures

If month-end reconciliation takes several days, your infrastructure likely lacks unified servicing integrity.

Co-lending operations become especially vulnerable here.

Multiple “Sources of Truth”

When different departments rely on different systems for the same data:

- Collections uses LMS

- Credit team uses LOS

- Finance uses Excel

- Analytics uses data warehouse snapshots

Then operational consistency disappears.

Why Unified LOS + LMS Architecture Matters

Modern lenders increasingly prefer unified lending infrastructure where:

- LOS and LMS share a common data model

- Product rules remain synchronized

- Borrower profiles stay centralized

- Repayment logic is consistent

- APIs remain native instead of patched together

This architecture eliminates many of the integration risks responsible for data corruption.

According to Roopya, their platform uses a unified data structure across origination and servicing to eliminate disbursal handover issues.

Unified systems reduce:

- Duplicate data entry

- Mapping complexity

- Middleware dependency

- Reconciliation effort

- Product configuration drift

They also improve:

- Real-time reporting

- Portfolio visibility

- Collection efficiency

- Compliance readiness

Best Practices to Prevent LOS-to-LMS Data Corruption

1. Use a Shared Data Model

The best lending platforms maintain a single borrower and loan architecture across:

- Origination

- Servicing

- Collections

- Reporting

This eliminates transformation errors.

2. Automate Validation at Every Stage

Validation should occur:

- During application intake

- During underwriting

- During disbursement

- During LMS account creation

- During repayment processing

Every critical field should be verified continuously.

3. Minimize Manual Operations

The more Excel-based workflows you maintain, the higher your corruption risk.

Lenders should automate:

- Account creation

- Repayment schedule generation

- Ledger updates

- Reconciliation

- Reporting

4. Maintain Product Configuration Governance

Every product update must synchronize across:

- LOS

- LMS

- Collections

- Analytics

Configuration drift is one of the largest hidden causes of servicing errors.

5. Use Real-Time Event Architecture

Modern lending infrastructure should support:

- Event-driven updates

- Real-time synchronization

- Transaction rollback protection

- Failure recovery logic

This prevents silent mismatches between systems.

6. Build Strong Audit Trails

Every data change should be:

- Timestamped

- Logged

- User-attributed

- Traceable

This improves:

- Compliance

- Root-cause analysis

- Operational accountability

7. Prioritize India-Native Lending Infrastructure

Indian lenders face unique operational complexity:

- NACH reconciliation

- Co-lending servicing

- Bureau integrations

- RBI reporting

- Daily EMI products

- Account Aggregator integrations

Infrastructure designed specifically for Indian lending environments handles these challenges more reliably.

The Future of Lending Infrastructure

The future of digital lending is moving toward:

- Unified platforms

- API-native ecosystems

- Real-time data synchronization

- AI-driven servicing automation

- Embedded compliance frameworks

Lenders no longer compete solely on:

- Distribution

- Interest rates

- Underwriting speed

Operational data integrity is becoming a major competitive advantage.

As lending portfolios scale into thousands or millions of active accounts, fragmented infrastructure becomes increasingly unsustainable.

The industry is moving away from disconnected LOS and LMS stacks toward unified lending operating systems capable of supporting the full loan lifecycle without data fragmentation.

How Roopya Helps Prevent LOS-to-LMS Data Corruption

Roopya LOS & LMS Platform provides a unified lending infrastructure platform designed for Indian lenders including:

- NBFCs

- Banks

- MFIs

- Fintech lenders

The platform combines:

- Loan Origination System (LOS)

- Loan Management System (LMS)

- Collections workflows

- Analytics

- Compliance operations

within a shared operational architecture.

Key capabilities include:

- Unified borrower data model

- Automated loan handover from LOS to LMS

- Real-time repayment synchronization

- Integrated NACH and payment workflows

- RBI-aligned servicing infrastructure

- No-code product configuration

- Automated audit trails

- Multi-channel servicing support

Because the origination and servicing layers operate within the same ecosystem, lenders reduce the integration gaps that typically create data corruption.

The transition from Loan Origination System to Loan Management System is one of the most critical points in the lending lifecycle. Unfortunately, it is also where many lenders unknowingly introduce operational risk.

Data corruption between origination and servicing creates:

- Financial losses

- Compliance exposure

- Customer dissatisfaction

- Collection inefficiencies

- Reconciliation breakdowns

As digital lending grows more complex in India, fragmented infrastructure becomes increasingly dangerous.

Modern lenders need:

- Unified data architecture

- Real-time synchronization

- Automated servicing workflows

- Integrated compliance frameworks

The future belongs to lending platforms that treat data consistency as a foundational operational priority rather than an afterthought.

For lenders planning to scale efficiently, the question is no longer whether LOS and LMS should work together.

The real question is whether your lending infrastructure can maintain a single source of truth across the entire borrower lifecycle.