Microfinance Software: India’s #1 Digital Lending Platform for NBFCs, MFIs & Modern Lenders

The Future of Microfinance Software Is Here

The microfinance and digital lending industry in India is undergoing a seismic transformation. As financial inclusion becomes a national priority and the demand for small-ticket loans, personal credit, and business financing surges across tier-2 and tier-3 cities, lenders need technology that is fast, compliant, intelligent, and scalable. Roopya — built by GeoAlgo Technologies Private Limited — has emerged as India’s most powerful and comprehensive digital lending platform, purpose-built for modern financial institutions including NBFCs, Banks, Microfinance Institutions (MFIs), and Loan Service Providers.

At its core, Roopya is a No-Code, AI-First, Cloud-Native lending infrastructure that transforms the entire lending lifecycle — from the moment a borrower submits an application to the final repayment and beyond. Unlike traditional legacy lending software that requires weeks of setup, heavy IT infrastructure, and enormous upfront costs, Roopya empowers lenders to go live in as little as one day — without writing a single line of code.

This article explores everything you need to know about Roopya’s microfinance software: its features, modules, AI capabilities, integrations, compliance tools, and why it is rapidly becoming the platform of choice for modern lenders across India.

Start Free Trial

Why Microfinance Institutions Need Modern Software

Before diving into Roopya’s capabilities, it is important to understand the problem it solves. Microfinance institutions and NBFCs in India have historically relied on disconnected, paper-heavy processes or outdated software that was never designed for the scale and speed that digital lending demands today.

The consequences are significant: slow loan processing, high operational costs, rising fraud rates, poor borrower experiences, and regulatory non-compliance. In a market where borrowers can access credit from multiple platforms in minutes, lenders cannot afford inefficiency.

Modern microfinance software must be able to:

- Process applications digitally at scale, across web and mobile channels

- Automate credit decisioning using bureau data and AI-powered scoring

- Manage the full loan lifecycle from origination to collections

- Integrate seamlessly with payment gateways, KYC providers, and banking APIs

- Generate regulatory reports compliant with RBI and other governing bodies

- Detect and prevent fraud using machine learning models

- Operate on the cloud with high availability, security, and zero downtime

Roopya was built to address every one of these requirements — and then go further.

Roopya Platform Overview: One Platform, Entire Lending Lifecycle

Roopya’s platform is a unified lending infrastructure that covers six core modules, each designed to work seamlessly together while also being independently powerful.

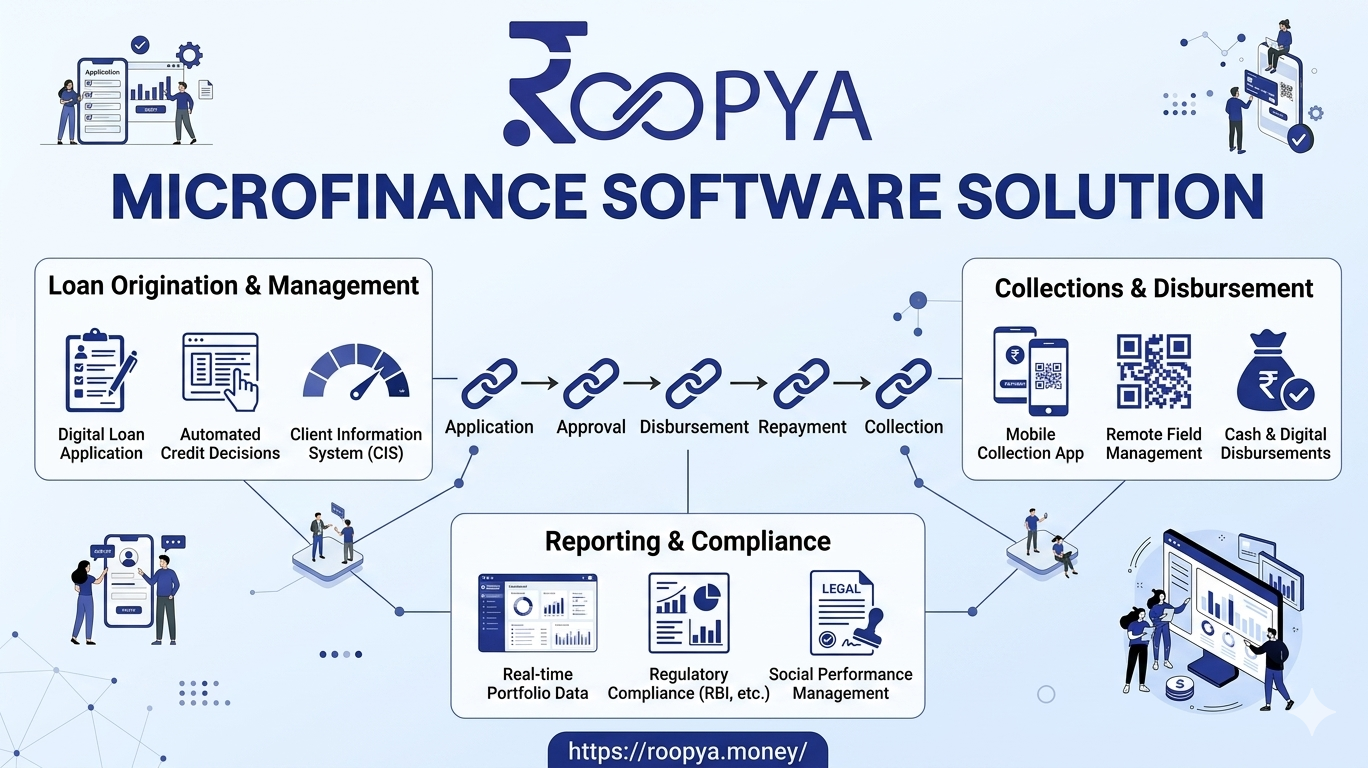

1. Loan Origination System (LOS)

The Loan Origination System is where a borrower’s journey begins. Roopya’s LOS is built to handle the entire application process — from initial inquiry to disbursement — with maximum automation and minimum manual intervention.

Digital Application Processing is at the heart of the LOS. Lenders can capture applications across multiple channels including web portals, mobile apps, and direct API integrations. Smart form pre-filling with real-time data validation reduces errors and drop-offs, while digital signature and e-KYC integration ensures a fully paperless process.

The Credit Decisioning Engine is what truly sets Roopya apart. Rather than relying on a single bureau score, Roopya integrates with all four major credit bureaus in India — CIBIL, Experian, Equifax, and CRIF — and combines bureau data with AI-powered credit scoring models and alternative data analytics. Lenders can build custom scorecards without any coding using the visual scorecard builder, and automated approval workflows reduce underwriting time from days to seconds.

Document Management is fully automated. OCR (Optical Character Recognition) technology extracts data from uploaded documents, classifies them automatically, and stores them in a centralized, encrypted repository with a complete audit trail and version control.

For microfinance institutions dealing with high application volumes and diverse borrower profiles, this level of automation is a game-changer. Applications that once took days to process can now be approved or declined in real time, dramatically improving both operational efficiency and borrower satisfaction.

2. Loan Management System (LMS)

Once a loan is disbursed, the Loan Management System takes over. Roopya’s LMS provides comprehensive control over the entire loan portfolio, handling everything from EMI scheduling to prepayments, loan restructuring, and customer communication.

Account Management features include complete loan lifecycle tracking, EMI scheduling and amortization calculations, interest accrual, prepayment and foreclosure handling, and even co-lending and loan syndication support. This makes Roopya suitable not just for small MFIs but also for larger NBFCs and banks engaged in complex lending structures.

The Payment Processing module integrates with leading payment gateways including Razorpay, PayU, and CCAvenue, and supports NACH/eNACH mandate management for automated EMI deductions. Real-time payment tracking and automated reconciliation eliminate the manual effort traditionally associated with payment management, while the refund and reversal processing module ensures smooth handling of exceptions.

Borrowers benefit from a Self-Service Customer Portal where they can view their account dashboard, make EMI payments, download statements, raise service requests, upload documents, and generate NOC certificates and other critical documents — all without calling a customer support agent. This reduces the operational load on lenders while significantly enhancing the borrower experience.

3. Collections & Recovery System

Delinquency management is one of the most critical — and challenging — aspects of microfinance operations. Roopya’s Collections System uses AI and automation to optimize recovery rates while maintaining positive borrower relationships.

The Smart Collections engine uses AI to determine the best strategy for each delinquent account, considering the borrower’s history, payment behavior, and communication preferences. Automated reminders are sent via SMS, email, and WhatsApp at optimal times, significantly reducing the cost of collections while improving response rates.

The system includes Collection Bucket Management, agent assignment and tracking, payment promise tracking, and field visit management for ground-level collections. For severely delinquent accounts, the Delinquency Management module handles DPD (Days Past Due) tracking, provisioning calculations, write-off processing, legal case management, and settlement negotiation tools.

For microfinance institutions with large borrower bases in rural and semi-urban areas, having a collections system that can operate across digital and field channels simultaneously is invaluable.

4. Early Warning System (EWS)

Prevention is better than cure, and Roopya’s Early Warning System embodies this philosophy. The EWS uses predictive analytics and behavioral data to identify loans that are at risk of default before they actually default.

By analyzing patterns in payment behavior, communication response rates, and external economic signals, the platform generates risk alerts and triggers proactive intervention workflows. Lenders can reach out to at-risk borrowers with restructuring options, top-up offers, or counseling before the situation becomes a non-performing asset.

This proactive approach to portfolio risk management is increasingly important in microfinance, where borrowers may not have the financial cushion to recover from unexpected income disruptions. Roopya’s EWS gives lenders the tools to identify vulnerabilities early and act decisively.

5. Lending Analytics

Data is the lifeblood of modern lending. Roopya’s Lending Analytics module transforms raw loan data into actionable intelligence through real-time dashboards, KPI monitoring, vintage analysis, cohort tracking, and custom report building.

The platform’s analytics capabilities extend into Credit Risk Analytics, including Credit Scorecard Development, Application Scorecard Development, Exposure at Default (EAD), Loss Given Default (LGD), Expected Credit Loss (ECL) calculations, and Loan Pricing Analytics. These are sophisticated risk management tools that are typically only available to large banks — Roopya makes them accessible to NBFCs and MFIs of all sizes.

Lenders can also use Roopya’s analytics to monitor approval and rejection patterns, identify operational bottlenecks, track collections efficiency, and benchmark portfolio performance against industry standards.

6. Advanced Reporting & Regulatory Compliance

Regulatory compliance is non-negotiable in the lending industry, and Roopya takes it seriously. The platform is continuously updated to reflect the latest RBI guidelines and regulatory changes, ensuring that lenders are always compliant without having to manually track and implement regulatory updates.

The reporting module covers RBI reporting (NPA classification, ALM reports, CRR/SLR), GST and TDS calculations, Fair Practices Code compliance, NBFC and bank-specific regulatory reports, and credit bureau reporting. A comprehensive audit trail logs every action taken on the platform, providing the transparency required for regulatory inspections and internal audits.

Custom dashboards allow lenders to monitor the metrics that matter most to their business, while scheduled reports can be automatically generated and distributed to key stakeholders — saving hours of manual reporting effort every month.

The AI Advantage: How Roopya Brings Intelligence to Lending

Artificial intelligence is not a buzzword at Roopya — it is the foundational layer that makes the entire platform more powerful, more accurate, and more efficient. Here is how AI is embedded throughout the Roopya ecosystem:

AI-Powered Document Analysis

Roopya’s advanced OCR and NLP systems can automatically extract, verify, and analyze documents with over 99% accuracy. Whether it is an Aadhaar card, PAN card, bank statement, income tax return, or salary slip — the platform processes documents in seconds, flags anomalies, and detects potential fraud without human intervention. This capability is especially valuable for microfinance institutions that process thousands of applications daily.

AI-Enhanced Business Rule Engine (BRE)

The No-Code Business Rule Engine is one of Roopya’s most powerful features. Lenders can configure complex credit policies, approval hierarchies, and lending rules through a visual, drag-and-drop interface. But Roopya goes a step further: the BRE uses machine learning to analyze historical data, suggest rule optimizations, identify patterns in approvals and rejections, and automatically adapt to changing market conditions — all while maintaining complete human oversight.

Intelligent Credit Decisioning

Traditional credit scoring relies heavily on CIBIL scores, which excludes a significant portion of India’s population — particularly in rural and semi-urban areas where microfinance institutions are most active. Roopya’s AI-powered credit scoring models go beyond the bureau score, analyzing thousands of alternative data points including mobile data patterns, transaction histories, and behavioral signals. This enables lenders to serve thin-file and new-to-credit borrowers responsibly and profitably, expanding financial inclusion while managing risk.

The result is real-time credit decisions in milliseconds with higher accuracy and lower default rates compared to traditional methods.

AI-Driven Analytics & Reporting

Roopya’s natural language processing capabilities allow business users to ask questions in plain English and receive detailed analytical responses instantly. The platform automatically identifies trends in portfolio data, generates predictive insights about future performance, and produces executive summaries — replacing hours of manual analysis with instant, always-available intelligence.

Measurable AI Impact

Roopya’s AI capabilities deliver concrete, measurable outcomes:

- 10x faster processing — document verification reduced from hours to seconds

- 40% better accuracy — ML-powered credit scoring outperforms traditional methods

- 80% fraud reduction — AI fraud detection across all applications

- 60% better collections — AI-driven collection strategies based on borrower behavior

- 95% conversational accuracy — AI handles borrower interactions with contextual understanding

- 24/7 continuous learning — models improve automatically with every transaction

300+ Pre-Integrated APIs: The Ecosystem Advantage

One of Roopya’s most significant competitive advantages is its pre-integrated ecosystem of over 300 APIs. For microfinance institutions and NBFCs, building and maintaining these integrations independently would require enormous time, cost, and technical resources. Roopya provides them all out of the box.

The integration ecosystem includes:

- Credit Bureaus: CIBIL, Experian, Equifax, CRIF

- Payment Gateways: Razorpay, PayU, CCAvenue

- Banking APIs: ICICI, HDFC, Axis, NPCI

- KYC Providers: DigiLocker, UIDAI (Aadhaar)

- Accounting Systems: Tally, SAP, Oracle

- Communication Channels: SMS, Email, WhatsApp

- Document Verification: PAN, GST, MCA, Income Tax

This pre-integrated ecosystem means lenders can connect to the services they need in hours rather than months, dramatically reducing time-to-market and integration costs.

20+ Pre-Configured Loan Products: Launch Faster

Roopya comes pre-configured with over 20 ready-to-use loan product templates covering:

- Personal Loans

- Payday / Salary Advance Loans

- Gold Loans

- Business and SME Loans

- Home Loans

- Auto / Vehicle Loans

- Microfinance Group Loans

- Agricultural Loans

Each product template includes pre-built workflows, document checklists, eligibility criteria, and customer journeys. Lenders can customize these templates to match their specific product requirements using the no-code configuration interface, and launch new loan products in hours rather than weeks.

This is particularly valuable for microfinance institutions looking to diversify their product offerings or quickly respond to market demand.

Implementation in Days, Not Months

Traditional lending software implementations can take months of painful, expensive IT projects before a single loan is processed. Roopya has completely reimagined the implementation experience.

Day 1: Sign up, entity verification, sandbox provisioning — done in 2-4 hours.

Days 2-3: Configure loan products, interest rates, approval workflows, document checklists, user roles, and communication templates — all through the no-code interface.

Days 3-4: Integrate payment gateways, credit bureaus, KYC providers, and banking APIs — fully supported by Roopya’s technical team.

Days 4-5: Team training, user acceptance testing, and performance testing.

Days 5-7: Production go-live with 24/7 dedicated support for the first week.

This implementation timeline — measured in days, not months — is made possible by Roopya’s plug-and-play architecture, pre-built integrations, and no-code configuration. Every lender is assigned a dedicated implementation manager who guides them through each step.

Pricing: Pay As You Use

Roopya’s pricing model is designed to be accessible to lenders of all sizes. There are no heavy upfront costs, no long-term lock-ins, and no expensive license fees. Lenders pay based on actual usage — meaning that whether you are a small MFI processing a few hundred loans per month or a large NBFC processing thousands, the pricing scales proportionally with your business.

This pay-as-you-use model democratizes access to enterprise-grade lending technology, making it possible for even early-stage NBFCs and growing microfinance institutions to compete with larger, more established players.

Security, Compliance & Data Privacy

Roopya takes security and data privacy with the utmost seriousness. The platform operates on an ISO 27001 certified infrastructure with end-to-end data encryption — both at rest and in transit. Enterprise-grade security features include role-based access control (RBAC), multi-factor authentication, IP whitelisting, VPN support, and regular penetration testing and security audits.

On the data privacy front, Roopya is compliant with GDPR and Indian data protection regulations, including PII data masking, consent management, data retention policies, and the right-to-be-forgotten implementation. Comprehensive disaster recovery and data backup systems ensure business continuity even in the event of infrastructure failures.

For microfinance institutions handling sensitive financial and personal data of millions of borrowers, this level of security is not optional — it is essential.

Who Should Use Roopya?

Roopya is designed for a wide range of lending institutions:

NBFCs (Non-Banking Financial Companies): Whether you are a consumer lending NBFC, a business lending NBFC, or a housing finance company, Roopya’s platform can handle your full lending lifecycle with regulatory compliance built in.

Microfinance Institutions (MFIs): From group lending to individual microloans, Roopya’s flexible product configuration and AI-powered decisioning help MFIs serve underbanked borrowers efficiently and profitably.

Banks: Roopya’s open API architecture and enterprise-grade security make it suitable for banks looking to digitize their lending operations or launch new digital lending products quickly.

Loan Service Providers (LSPs): LSPs and fintech companies acting as distribution partners can use Roopya’s embedded finance capabilities to integrate lending products into their own platforms.

Fintech Startups: For new entrants looking to launch a digital lending business, Roopya’s 1-day setup, pay-as-you-use pricing, and no-code platform remove the traditional barriers to entry.

Trusted by Modern Lenders Across India

Roopya is already trusted by a growing portfolio of modern lenders including IndiaKaLoan, QuickFinShop, Recapita, Findoc, EazyCredit, and LoanSeva — institutions that have chosen Roopya for its speed, reliability, and intelligence. These are lenders who understand that the future of microfinance and digital lending belongs to those who leverage the best technology.

Conclusion: Transform Your Lending Operations with Roopya

The microfinance and digital lending landscape in India is evolving faster than ever before. Borrowers expect instant decisions, seamless digital experiences, and flexible repayment options. Regulators demand transparency, compliance, and data security. Investors expect efficient operations, low default rates, and scalable growth.

Roopya delivers on all of these expectations — and more.

With its no-code platform, AI-powered intelligence, 300+ pre-integrated APIs, 20+ loan products, rapid implementation, and pay-as-you-use pricing, Roopya is not just a software solution — it is a competitive advantage.

Whether you are an established NBFC looking to modernize your technology stack, an MFI looking to scale your operations, or a fintech startup ready to disrupt the lending market, Roopya gives you the infrastructure to move faster, lend smarter, and grow confidently.

Visit roopya.money to request a demo and go live in just one day.