Switch to Roopya: The Complete Guide to End-to-End Digital Lending Automation

There is a moment every lender reaches — a moment where the spreadsheets are no longer manageable, the manual KYC queue is three days long, the collections team is drowning in follow-up calls, and the credit team is making decisions based on incomplete data. It is the moment where a lending business, however successful it has been, realises that its infrastructure has become the ceiling on its growth.

If you are reading this, you have probably reached that moment. Or you are approaching it faster than you would like.

The good news is that switching to Roopya a modern, end-to-end digital lending automation platform does not have to be a six-month implementation nightmare. With Roopya, it is a one-day transformation. This guide explains what end-to-end digital lending automation actually means, what it costs your business to delay the switch, and exactly what you gain when you make the move to Roopya.

Start Free Trial

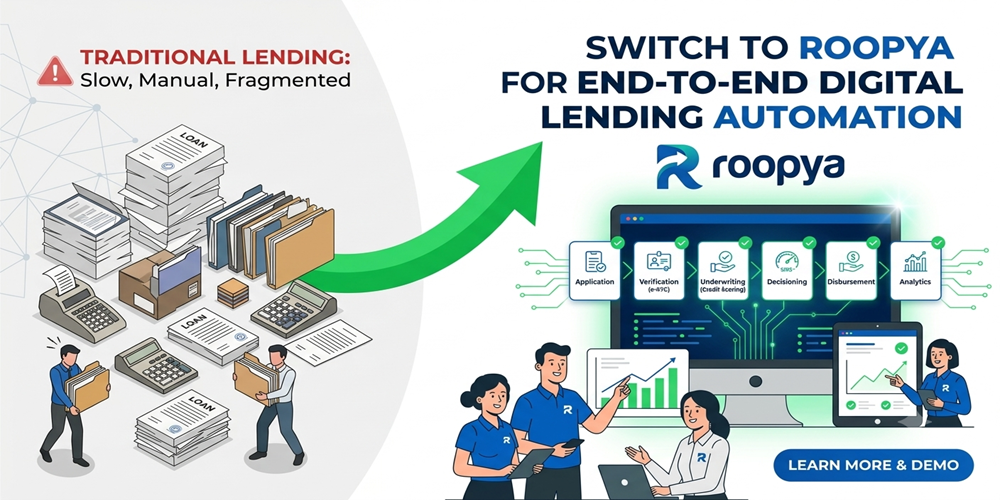

1. What Is End-to-End Digital Lending Automation?

End-to-end digital lending automation refers to the complete digitisation and automation of every stage of the lending lifecycle — from the moment a borrower submits an application to the final repayment and loan closure. It is not a single feature or a single software tool. It is a unified infrastructure that replaces every manual, fragmented, or paper-based process in your lending operation with a seamless, automated, data-driven workflow.

A truly end-to-end digital lending platform covers:

- Loan Origination: Digital application capture, automated KYC, credit bureau pulls, AI-powered document analysis, and real-time credit decisioning.

- Loan Management: Portfolio tracking, amortisation schedules, payment processing, customer portals, and account servicing.

- Collections: Automated payment reminders, intelligent collection workflows, agent management, payment plan configuration, and recovery optimisation.

- Early Warning and Risk Management: Predictive default detection, behavioural analytics, risk scoring, and proactive intervention triggers.

- Analytics and Reporting: Real-time portfolio dashboards, regulatory compliance reports, performance metrics, and AI-generated executive insights.

Most lenders today operate with some combination of disconnected tools — a legacy LOS from one vendor, a manual collections process, spreadsheet-based portfolio tracking, and a separate reporting tool that is always two days behind. End-to-end digital lending automation replaces all of this with a single, unified platform where data flows seamlessly between every stage of the loan lifecycle.

Roopya is that platform — purpose-built for Indian NBFCs, banks, MFIs, and modern fintech lenders who need to automate the entire lending operation, not just parts of it.

2. The Cost of Not Switching: What Legacy Processes Are Costing You Right Now

Before understanding the value of switching to Roopya, it is worth being honest about what staying on your current infrastructure is costing. These costs are often hidden, distributed across departments, and therefore easy to underestimate.

2.1 The Cost of Slow Loan Origination

Every day that a loan application sits in a queue is a day that a competitor could be disbursing to that borrower. In a market where digital-first lenders are offering sub-10-minute approvals, a process that takes two or three business days is not just inefficient — it is commercially devastating. Studies consistently show that loan application abandonment rates spike sharply after the first hour. A slow origination process is a direct revenue leak.

2.2 The Cost of Manual KYC and Document Processing

Consider what it costs to employ a team of people to manually verify Aadhaar documents, pull credit bureau reports, read and interpret bank statements, and manually enter data into your core system. Now consider that AI-powered document processing can do all of this in seconds, at a fraction of the cost, with higher accuracy. Manual document processing is one of the highest-cost, highest-error-rate activities in any lending operation. It is also the most unnecessary in 2025.

2.3 The Cost of Inconsistent Credit Decisions

When credit decisions are made manually — even by experienced underwriters — they are subject to human bias, inconsistency, fatigue, and error. The same application reviewed by two different team members on two different days may receive different outcomes. This inconsistency not only introduces risk into your portfolio but creates regulatory exposure. A configurable, automated Business Rule Engine eliminates this variability entirely.

2.4 The Cost of Poor Collections Efficiency

Collections is one of the highest-leverage activities in any lending business. A 1% improvement in collection rates on a ₹100 crore portfolio is ₹1 crore of direct bottom-line impact. Yet most lenders are running collections through a combination of spreadsheet-tracked calling lists and manual payment reconciliation. AI-driven collections platforms can increase recovery rates by up to 60% — not by working harder, but by contacting the right borrowers through the right channels at the right time.

2.5 The Cost of Fragmented Data and Poor Visibility

If your origination data lives in one system, your portfolio data in another, and your collections data in a third — or worse, in a spreadsheet — you have no real-time visibility into the health of your lending business. Decisions are made on stale data. Early warning signals are missed. Regulatory reports take days to compile. A unified platform with real-time analytics changes all of this fundamentally.

3. What Makes Roopya Different: The Case for Switching

There are dozens of lending software vendors in India. Many promise automation. Many claim to be comprehensive. Roopya is different in ways that matter specifically to the Indian lending market — and to lenders at every stage of growth.

3.1 Truly End-to-End, Not a Patchwork

Many so-called ‘complete’ lending platforms are actually a collection of modules acquired over the years through partnership agreements and integrations — modules that look unified on a sales deck but require significant custom work to actually connect. Roopya was built from a single, unified data architecture. Origination data flows seamlessly into loan management, which feeds collections, which connects to analytics. There are no data silos, no manual handoffs, and no synchronisation delays. Every team in your organisation operates from the same real-time view of every loan.

3.2 1-Day Go-Live — Not 6 Months

Traditional lending software implementations are notoriously painful. Vendor contracts, customisation specifications, system integration projects, user acceptance testing, staff training — the typical enterprise LOS implementation takes six to twelve months and costs tens of lakhs in services fees before you process a single live loan. Roopya’s pre-built loan product journeys, plug-and-play API integrations, and no-code configuration interface mean that a new lender can go live and begin processing real applications within 24 hours of onboarding. Existing lenders migrating from legacy systems can typically complete the transition in a matter of days, not months.

3.3 No-Code Configuration for Business Users

The most dangerous dependency in a legacy lending system is the vendor’s development team. Every time you need to change a credit policy rule, modify an application form field, add a new loan product, or adjust a collection workflow, you raise a ticket and wait — sometimes weeks. Roopya’s platform is built around the principle that business users should be able to configure everything themselves, without writing a single line of code. Credit managers configure underwriting rules. Product managers launch new loan products. Operations teams adjust collection strategies. No developer required, no vendor dependency, no waiting.

3.4 300+ Pre-Integrated APIs Out of the Box

Integration is one of the most expensive and time-consuming parts of any lending platform implementation. Building API connections to credit bureaus, KYC providers, eSign platforms, payment gateways, accounting software, and banking APIs typically requires months of development work. Roopya has done this work already. Over 300 APIs are pre-integrated and live — covering all four major credit bureaus (CIBIL, Experian, CRIF, Equifax), Aadhaar eKYC, PAN verification, Digilocker, VKYC, multiple eSign providers, NACH payment processing, IMPS and UPI disbursement, GST data providers, account aggregators, and more. You turn them on, not build them.

3.5 AI-Powered Intelligence at Every Stage

Artificial intelligence in Roopya is not a marketing claim or a future roadmap item. It is embedded and operational at every stage of the lending lifecycle today:

- Document Processing: AI-powered OCR and NLP extract, verify, and analyse documents with 99%+ accuracy. Bank statements, salary slips, ITRs, and GST returns are processed in seconds.

- Fraud Detection: Machine learning models identify anomalies, inconsistencies, and fraud signals across documents, application data, and behavioural patterns in real time.

- Credit Decisioning: ML-based credit scoring models analyse thousands of data points — bureau data, alternative data, behavioural signals, and financial indicators — to produce risk scores and credit decisions in milliseconds.

- Collections: AI-driven collection workflows identify the optimal contact time, channel, and message for each borrower, maximising recovery rates while minimising cost.

- Analytics: NLP-powered reporting allows your team to ask questions in plain English and receive instant insights. AI identifies portfolio trends, predicts performance, and flags early warning signals before they become NPAs.

3.6 Pay-As-You-Use Pricing — Zero Upfront Cost

Traditional lending software vendors typically demand large upfront licence fees, annual maintenance charges, and expensive implementation service agreements. These models make sense for the vendor but not for the lender — particularly for early-stage NBFCs, growing MFIs, and new fintech lenders who need enterprise-grade infrastructure but cannot afford enterprise-grade capital expenditure. Roopya’s pay-as-you-use model means you pay only for what you actually process. There are no minimum monthly fees, no upfront licence costs, and no long-term lock-in contracts. Your technology cost scales exactly with your business.

3.7 Continuous Regulatory Compliance

The RBI’s regulatory landscape for digital lending is evolving rapidly. Guidelines on digital lending, KYC norms, account aggregator integration, data localisation, and fair lending practices are updated regularly. Keeping a legacy system compliant typically requires expensive customisation work each time a new guideline is issued. Roopya’s platform is maintained and updated continuously by a dedicated compliance engineering team. When the RBI issues new guidelines, Roopya updates the platform — and your business stays compliant automatically.

4. The Complete Roopya Platform: What You Get When You Switch

4.1 Loan Origination System (LOS)

Roopya’s LOS covers the full origination lifecycle with pre-configured digital application forms, automated KYC triggers, instant credit bureau pulls, AI-powered document analysis, configurable underwriting rules, real-time credit decisioning, personalised offer generation, digital agreement execution via eSign, and automated disbursement triggers. With 20+ pre-configured loan product journeys — personal loans, business loans, MSME credit, gold loans, home loans, payday loans, auto loans, and microfinance — you can launch new products without building journeys from scratch.

4.2 Loan Management System (LMS)

Once a loan is disbursed, Roopya’s LMS takes over — managing the full post-disbursement lifecycle. This includes portfolio-level tracking and health monitoring, detailed amortisation schedule management, automated EMI processing and payment reconciliation, customer self-service portal, account statement generation, prepayment and foreclosure handling, and NACH mandate management. The LMS provides real-time visibility into every loan in your portfolio, with configurable alerts for missed payments, due date approaches, and portfolio health metrics.

4.3 Collections System

Roopya’s intelligent collections platform transforms recovery operations from reactive to proactive. AI-driven prioritisation identifies which borrowers to contact first, when, and through which channel — SMS, WhatsApp, email, or phone — for maximum recovery impact. Automated payment reminders are deployed at configurable intervals before and after due dates. Agent management dashboards track collector productivity, assignment queues, and resolution rates. Payment plan configuration allows flexible restructuring without manual paperwork. The result: collection efficiency improvements of up to 60% compared to manual processes.

4.4 Early Warning System (EWS)

Roopya’s Early Warning System uses predictive analytics to identify loans at risk of default before they actually miss a payment. Behavioural analytics — tracking payment patterns, account activity changes, and external data signals — generate risk scores that flag potential NPAs weeks or months before they materialise. Alert management workflows route high-risk cases to the appropriate team for proactive intervention. This allows lenders to offer restructuring, additional support, or targeted communication before a borrower falls into delinquency — dramatically improving both portfolio quality and borrower relationships.

4.5 Lending Analytics and Reporting

Roopya’s analytics layer provides real-time visibility into every dimension of your lending business. Pre-built dashboards cover portfolio performance, origination funnel analysis, credit quality distribution, collection efficiency, geographic concentration, and product-level profitability. Custom dashboard configuration allows every team — credit, operations, finance, risk, and executive management — to build the view they need. AI-generated narrative reports summarise complex data in plain English, saving hours of manual analysis each week. Regulatory reporting — for RBI, credit bureaus, and internal governance — is automated and always current.

5. How the Switch to Roopya Works: A Step-by-Step Migration Guide

Switching to a new lending platform sounds daunting. With Roopya, the process is structured, supported, and remarkably fast.

- Step 1 – Discovery and Demo (Day 0): Your team meets Roopya’s onboarding specialists. We understand your current lending products, credit policies, regulatory setup, and integration requirements. A customised demo shows exactly how Roopya will handle your specific use cases.

- Step 2 – Configuration (Day 0-1): Using Roopya’s no-code interface, your team configures your loan products, credit policy rules, application forms, and workflow parameters. Roopya’s specialists guide the process — most lenders complete this in a single day.

- Step 3 – API Connections (Day 1): Required integrations — credit bureaus, KYC providers, payment gateways, eSign platforms — are activated from Roopya’s pre-built library. No development work. Switch on and test.

- Step 4 – Data Migration (Day 1-2): Existing portfolio data is migrated to Roopya’s LMS in structured formats. Our data team handles the migration with full validation and reconciliation checks.

- Step 5 – Team Training (Day 2): Roopya’s training materials and live walkthrough sessions get your credit, operations, and collections teams productive on the platform quickly. The no-code interface means the learning curve is minimal.

- Step 6 – Go Live (Day 2-3): Your first live loan applications are processed on Roopya. Roopya’s support team provides hypercare coverage for the first two weeks, ensuring any configuration adjustments are handled immediately.

From first conversation to first live loan: typically 24 to 72 hours. No other lending platform in India comes close to this timeline.

6. Who Should Switch to Roopya?

Roopya is designed to serve the full spectrum of Indian lenders — from day-one NBFCs to established institutions looking to modernise:

New and Early-Stage NBFCs

If you have recently received your NBFC licence and are setting up your lending operations, Roopya is the most efficient path to market. Rather than building or procuring separate systems for origination, loan management, and collections — and spending months integrating them — Roopya gives you a complete, live, integrated lending operation in a single day. The pay-as-you-use model means your technology cost grows with your business, not ahead of it.

Growing NBFCs and MFIs Hitting Infrastructure Limits

If your current volume has outgrown your existing tools — if your team is spending more time managing spreadsheets than managing credit, or if your collections efficiency is deteriorating as your portfolio grows — it is time to switch. Roopya’s cloud infrastructure scales automatically with your volume. Whether you are processing 500 applications a month or 50,000, the platform performs without additional investment in hardware, software licences, or headcount.

Banks Modernising Retail Lending

Traditional banks are increasingly competing with digital-first NBFCs for personal loan, auto loan, and MSME lending market share. A bank’s legacy core banking system was not built for the speed, flexibility, or digital experience that modern borrowers demand. Roopya’s open API architecture allows banks to deploy a modern digital lending front-end — origination, decisioning, and customer experience — while maintaining connectivity to their existing core banking infrastructure.

Fintech Lenders Seeking Infrastructure Independence

Fintech lenders often begin with a highly customised, developer-built origination stack. This works until it doesn’t — when credit policy changes require development sprints, when new product launches take months, and when the technology team becomes a bottleneck to business decisions. Switching to Roopya gives fintech lenders a best-in-class, continuously updated, no-code lending infrastructure — freeing their development resources for product innovation rather than maintenance.

7. Real Results: What Lenders Experience After Switching to Roopya

- 10x Faster Loan Processing: Intelligent document processing reduces verification time from hours to seconds, collapsing the origination cycle dramatically.

- 40% Improvement in Credit Scoring Accuracy: ML-powered credit models outperform traditional rule-based scoring, reducing both false positives and false negatives in underwriting decisions.

- 80% Reduction in Fraud Losses: AI-powered fraud detection modules identify suspicious patterns and synthetic identities that manual review consistently misses.

- 60% Better Collection Efficiency: AI-driven collection workflows, optimal contact timing, and automated reminders maximise recovery rates with lower operational cost.

- 95% Borrower Satisfaction in Digital Interactions: Roopya’s conversational AI and seamless digital journey deliver borrower experience scores that rival the best consumer apps in India.

- Zero Compliance Incidents: Continuous regulatory updates, built-in audit trails, and automated regulatory reporting eliminate compliance gaps that plague manual processes.

8. Roopya vs. Your Current Solution: An Honest Comparison

Roopya vs. Legacy LOS/LMS Vendors

Legacy lending software vendors built their platforms for a pre-digital world. Their systems require lengthy implementations, expensive customisation for every change, annual licence fees regardless of usage, and slow update cycles that struggle to keep pace with regulatory change. Roopya is a cloud-native, API-first, AI-powered platform designed for the speed and flexibility of modern lending. The comparison is not about features on a checklist — it is about velocity, adaptability, and total cost of ownership.

Roopya vs. Building In-House

Some lenders, particularly well-funded fintechs, consider building their lending infrastructure in-house. This path offers maximum customisation but comes with enormous costs — a full lending platform requires six to twelve months of development, a team of ten or more engineers, ongoing maintenance investment, and the permanent risk of technical debt. Roopya delivers the same or better capabilities on day one, at a fraction of the cost, with the added advantage of continuous updates, pre-built integrations, and a dedicated support team. Building in-house is an option, but it is rarely the right one for lenders whose core expertise is credit, not software engineering.

Roopya vs. Spreadsheets and Manual Processes

If your current ‘system’ is primarily spreadsheets, shared drives, WhatsApp groups, and manual reconciliation, the comparison is straightforward. Every hour your team spends on manual data entry, document verification, or EMI reconciliation is an hour not spent on credit analysis, portfolio growth, or customer relationships. The cost of manual processes — in time, errors, compliance risk, and opportunity cost — far exceeds the cost of Roopya’s pay-as-you-use subscription.

9. The Roopya Ecosystem: Partners, Integrations, and Embedded Finance

Switching to Roopya does not mean working in isolation. Roopya’s open API architecture and growing partner ecosystem mean that your lending operation connects seamlessly with every tool your business depends on.

Credit bureau partners include CIBIL, Experian, CRIF, and Equifax — all pre-integrated and activated with a single switch. KYC infrastructure covers Aadhaar eKYC, PAN verification, Digilocker, VKYC, and video-based identification. Payment infrastructure includes NACH mandate processing, IMPS and UPI disbursement and collection, and reconciliation with all major payment processors. Account Aggregator connectivity enables consent-based financial data sharing for faster, richer underwriting. Open integration APIs allow Roopya to connect with your existing CRM, ERP, accounting platform, or core banking system without disruption.

For lenders building embedded finance products — integrating lending directly into partner platforms, e-commerce marketplaces, or employer payroll systems — Roopya’s Embedded Finance API suite enables white-label loan origination, instant decisioning, and seamless co-lending workflows. Your lending product, your brand, Roopya’s infrastructure.

10. Make the Switch Today: How to Get Started with Roopya

Getting started with Roopya requires nothing more than a conversation. There are no lengthy procurement processes, no minimum commitment requirements, and no technical prerequisites. The Roopya team works with your business to understand your products, configure your setup, activate your integrations, and get you live — in a single day.

Roopya is trusted by India’s modern lenders — IndiaKaLoan, QuickFinShop, Recapita, Findoc, EazyCredit, LoanSeva, and others — who have made the switch and are now processing loans faster, more accurately, and more profitably than ever before.

The question is not whether your lending business needs end-to-end digital automation. In 2025, that question has already been answered. The question is how quickly you can make the switch — and what it is costing you every day that you delay.

Request a free demo today at roopya.money. Go live tomorrow. Grow without limits.