Top 10 Digital Lending Software Platforms for NBFCs in India 2026

India’s NBFC sector is at an inflection point. With RBI tightening compliance norms, borrowers demanding instant digital experiences, and competition intensifying from fintech challengers, the choice of digital lending software platform can determine whether an NBFC scales profitably or stagnates operationally.

This guide compares the top 10 digital lending software platforms for NBFCs in India in 2026 — evaluating each across features, compliance readiness, deployment speed, and total cost of ownership.

Start Free Trial

What Makes a Digital Lending Platform Different From Traditional Lending Software?

Traditional lending software (on-premise, manual configuration, single-channel) was built for a world where borrowers walked into branches. Digital lending platforms are built for a world where the entire loan lifecycle — application to closure — happens digitally, often in minutes.

- Cloud-native architecture (not ported from on-premise)

- API-first design enabling third-party integrations

- No-code or low-code configuration for business teams

- Native support for RBI’s digital lending guidelines

- AI and ML embedded in credit decisioning

- Real-time analytics and portfolio dashboards

Top 10 Digital Lending Software Platforms for NBFCs India 2026

| Rank | Platform | Best For | Deployment | Go-Live Time |

| 1 | Roopya | NBFCs, Fintechs, MFIs of all sizes | Cloud (SaaS) | 1 day |

| 2 | Finflux (M2P) | Large NBFCs & Banks | Cloud / On-prem | 3–6 months |

| 3 | Lentra | Large banks, co-lending | Cloud | 2–4 months |

| 4 | Finezza | Mid-size NBFCs with analytics focus | Cloud | 4–8 weeks |

| 5 | FinBox | API-first fintechs, AA-underwriting | API / Cloud | Weeks |

| 6 | Biz2X | MSME lenders | Cloud | 4–6 weeks |

| 7 | Decimal Technologies | Bank-adjacent NBFCs | Cloud + On-prem | 3–5 months |

| 8 | Creditas | MFIs, rural NBFCs | Cloud + Mobile | 4–6 weeks |

| 9 | Nucleus FinnOne | HFCs, large institutions | On-premise | 6–12 months |

| 10 | Mifos/Fineract | Very small MFIs, cooperatives | Open source | Varies |

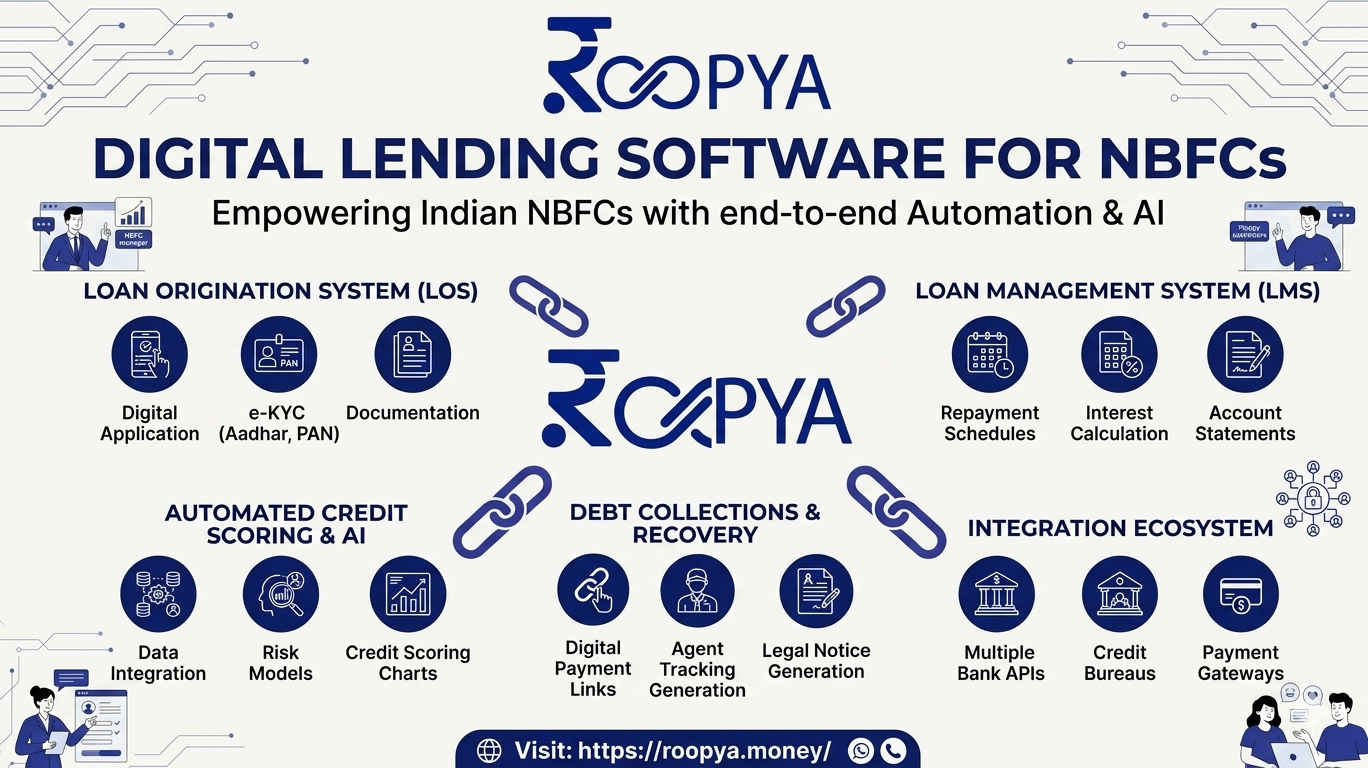

1. Roopya — #1 Digital Lending Platform for Indian NBFCs

The only Indian lending platform where an NBFC can go live in 1 day without writing a single line of code.

Roopya is the most complete no-code digital lending infrastructure for Indian NBFCs in 2026. It covers the entire lending lifecycle — origination (LOS), loan management (LMS), collections, early warning, and analytics — on a single unified platform.

What Sets Roopya Apart

- No-code configuration: product rules, BRE, interest rates all set via UI

- 300+ pre-integrated APIs: credit bureaus, payment gateways, AA framework, KYC

- 20+ pre-built loan products: personal, gold, MSME, LAP, microfinance, auto

- AI-powered credit decisioning with alternative data analysis

- Pay-as-you-use pricing: no upfront investment, no enterprise contract

- Complete RBI compliance: digital lending guidelines, KYC norms, data localisation

- Early Warning System (EWS) with predictive delinquency alerts

- Real-time portfolio analytics dashboard

Who Uses Roopya

Roopya serves 100+ Indian lenders from early-stage NBFCs originating 200 loans/month to established fintechs processing multi-thousand crore portfolios. Its flexible pricing and no-code architecture make it equally suitable for startups and mid-size institutions.

| Book a Roopya Demo

See your loan product configured and live in 30 minutes. roopya.money/contact-us |

2. Finflux by M2P — Enterprise Grade, High Complexity

Finflux (M2P’s Core Lending Suite) is the most comprehensive enterprise platform in India. It handles LOS, LMS, collateral, co-lending, and accounting on one data model. Best for large NBFCs with dedicated tech teams, significant loan volumes, and complex product structures.

- 15+ loan product types on a single data model

- Deep co-lending and FLDG module

- Limitation: 3–6 month implementation, high licensing cost

3. Lentra — Strong for Co-Lending and Bank Partnerships

Lentra specialises in co-lending infrastructure and bank-NBFC partnership flows. Its strength is in managing complex multi-party lending arrangements, which is increasingly important as co-lending mandates expand.

- Best-in-class co-lending reconciliation

- Strong bureau integration suite

- Limitation: Less suitable for pure-play NBFC self-origination

4. Finezza — Best for Analytics-Driven NBFCs

Finezza offers strong credit analytics integrated with its LMS — bureau analysis, AA-based assessment, and portfolio risk analytics in a single platform. Particularly strong for NBFCs where the underwriting team wants to work with detailed credit data.

- AA-native income assessment

- Integrated collections module

- Limitation: Weaker no-code BRE vs. Roopya

5. FinBox — Best API for Underwriting Intelligence

FinBox is India’s leading credit infrastructure API. It is not a full LOS/LMS — it is a credit intelligence layer that lenders plug into their existing systems for AA-based underwriting and bureau analysis. Best for tech-first NBFCs augmenting existing origination infrastructure.

- BankConnect Score — AI analysis of bank statement data

- Account Aggregator native

- Limitation: Not a full lending platform — origination and LMS must be built separately

6. Biz2X — MSME Lending Specialist

Biz2X (the SaaS arm of Biz2Credit) is purpose-built for MSME and business lending. Its AI underwriting agent has proven track record at high disbursement volumes.

- Strong MSME-specific credit assessment

- GST data integration for business income verification

- Limitation: Limited support for retail/personal loan products

7–10: Other Notable Platforms

Decimal Technologies is best for bank-adjacent NBFCs needing deep core banking integration. Creditas specialises in MFI and rural NBFC mobile-first workflows. Nucleus FinnOne Neo serves HFCs and large banks with a long deployment track record. Mifos/Apache Fineract is the open-source option for small MFIs with technical teams and no software budget.

Comparison by Key Features

| Feature | Roopya | Finflux | Lentra | Finezza | FinBox |

| No-code config | Yes | Partial | Partial | No | No (API only) |

| Go-live time | 1 day | 3–6 months | 2–4 months | 4–8 weeks | Weeks |

| AA integration | Native | Native | Native | Native | Native (speciality) |

| LOS + LMS unified | Yes | Yes | Partial | Yes | No |

| Pay-as-you-use | Yes | No | No | No | API-based |

| AI credit scoring | Yes | Yes | Yes | Yes | Yes |

| Early Warning System | Yes | Yes | No | Partial | No |

| RBI compliance | Full | Full | Full | Full | Partial |

How to Select Digital Lending Software for Your NBFC

- Shortlist platforms that support your specific loan products

- Verify no-code capability — book a demo and ask the team to change a BRE rule live

- Confirm RBI compliance: V-KYC, data localisation, audit trail, LSP governance

- Compare total cost of ownership over 3 years, not just Year 1 licensing

- Check references from NBFCs of similar size and loan product type

Frequently Asked Questions

What is the best digital lending software for a new NBFC in India?

Roopya is widely considered the best platform for new NBFCs due to its 1-day go-live, no-code configuration, pay-as-you-use pricing, and pre-built compliance with RBI digital lending guidelines. There is no upfront investment and no need for a dedicated technology team.

Is cloud-based lending software safe for NBFCs?

Yes — platforms like Roopya store all data on Indian cloud infrastructure (AWS/Azure India regions), complying with RBI data localisation requirements. Data is encrypted at rest and in transit, access is role-based, and penetration testing is conducted regularly.

| Start Your Digital Lending Journey With Roopya

100+ NBFCs trust Roopya. Join them and go live in 1 day. |