Video KYC Compliance for NBFCs: What Your Digital Lending Platform Must Support in 2026

The Indian lending ecosystem is rapidly transforming. Non-Banking Financial Companies (NBFCs), fintech lenders, microfinance institutions, and digital banks are moving away from branch-based onboarding toward fully digital customer acquisition. At the center of this transformation lies Video KYC (Know Your Customer), a technology-enabled process that allows lenders to verify borrower identities remotely while remaining compliant with RBI regulations.

Start Free Trial

As digital lending scales in India, compliance is no longer just a legal requirement — it has become a competitive advantage. Borrowers expect instant onboarding, paperless verification, faster approvals, and real-time loan decisions. Meanwhile, regulators expect strict adherence to KYC norms, fraud prevention measures, audit trails, and data security standards.

This is where modern lending platforms such as Roopya are redefining the industry by combining Video KYC, AI-driven underwriting, analytics, and credit risk automation into one unified lending infrastructure.

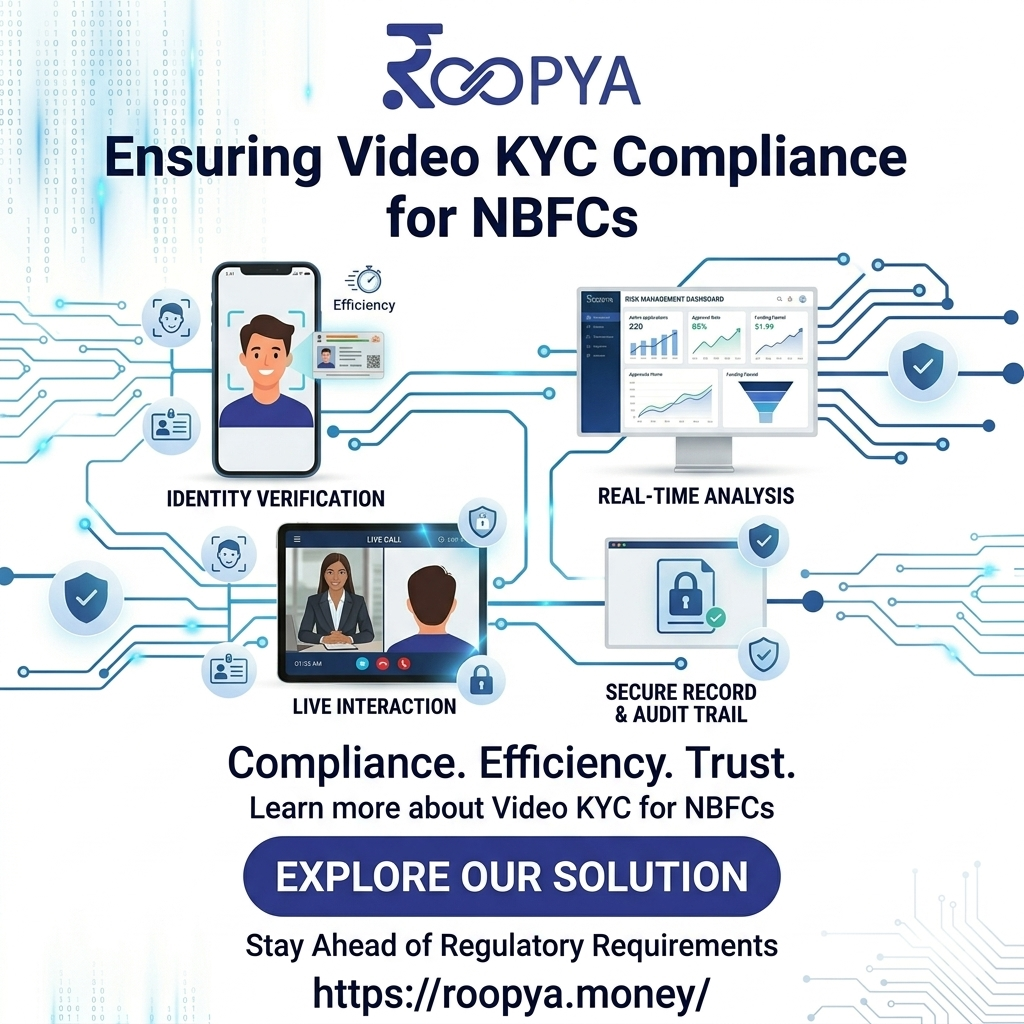

What is Video KYC for NBFCs?

Video KYC, also called V-CIP (Video-based Customer Identification Process), is a remote identity verification process approved by the Reserve Bank of India (RBI). It allows financial institutions to complete borrower onboarding through secure live video interaction instead of requiring physical branch visits.

Through Video KYC, NBFCs can:

- Verify borrower identity remotely

- Authenticate PAN and Aadhaar information

- Capture geo-location and live images

- Detect fraud and impersonation

- Reduce onboarding turnaround time

- Maintain digital compliance records

For lenders operating in high-volume digital lending environments, Video KYC is now a critical operational requirement rather than an optional feature.

Why Video KYC Matters More Than Ever in 2026

India’s digital lending market is growing at an unprecedented rate. Customers increasingly prefer instant loan approvals through mobile-first platforms. At the same time, fraud attempts, identity theft, synthetic identities, and fake documentation are also rising rapidly.

Several public discussions and customer complaints across India have highlighted how weak KYC processes can result in fraud, CIBIL disputes, and identity misuse.

This creates a massive challenge for NBFCs:

- How do you scale loan disbursement quickly?

- How do you maintain RBI compliance?

- How do you prevent fraud without slowing approvals?

- How do you automate onboarding while maintaining customer trust?

The answer lies in combining:

- Video KYC

- AI-powered verification

- Automated credit underwriting

- Real-time analytics

- Risk monitoring systems

- Fraud detection engines

Platforms like Roopya integrate all these capabilities into a single cloud-native lending ecosystem.

RBI Compliance Requirements for Video KYC

NBFCs must ensure their Video KYC process follows RBI’s digital onboarding framework and KYC master directions.

A compliant Video KYC platform should support:

1. Live Video Interaction

The system must conduct real-time video verification between the customer and authorized verification personnel.

The platform should include:

- Real-time video streaming

- Session recording

- Timestamping

- Geo-tagging

- Image capture

- Face verification

2. Identity Verification

The system should validate:

- PAN verification

- Aadhaar verification

- CKYC records

- DigiLocker integration

- OCR-based document extraction

Modern AI-enabled OCR systems can extract and verify borrower data within seconds. Roopya’s AI-powered OCR and document verification engine reportedly achieves over 99% extraction accuracy.

3. Fraud Detection Mechanisms

A compliant platform must detect:

- Deepfake attempts

- Screen replay attacks

- Face mismatch

- Multiple applications

- Synthetic identities

- Edited documents

AI-based fraud analytics are becoming essential because manual verification alone cannot scale with high application volumes.

4. Audit Trails and Data Storage

Every Video KYC session must maintain:

- Complete recording logs

- User activity trails

- Consent capture

- Device information

- Verification metadata

Audit readiness is now mandatory for regulatory inspections.

5. Data Security and Encryption

Borrower data must remain protected through:

- End-to-end encryption

- Secure cloud hosting

- Role-based access control

- Compliance logging

- Data retention policies

Roopya emphasizes bank-grade security, encrypted storage, and compliance-ready infrastructure for Indian lenders.

Key Features Every Digital Lending Platform Must Support

A modern NBFC lending platform must go beyond basic KYC workflows. The future belongs to intelligent lending infrastructure powered by automation, analytics, and AI.

Below are the essential features every platform must support in 2026.

1. AI-Powered Video KYC Automation

Manual verification processes are expensive and slow.

AI-driven Video KYC can automate:

- Face matching

- Liveness detection

- Identity validation

- Document OCR

- Signature verification

- Fraud detection

This dramatically reduces onboarding turnaround time while improving compliance accuracy.

According to industry discussions, AI adoption in digital lending is accelerating because lenders require faster approvals without compromising risk controls.

2. Automated Credit Risk Assessment

Video KYC alone is not enough.

The lending platform must integrate with:

- CIBIL

- Experian

- Equifax

- CRIF High Mark

- Account Aggregators

- GST systems

- Banking APIs

This enables instant underwriting decisions using:

- Bureau scores

- Banking behavior

- GST cashflows

- Transaction analysis

- Alternative data models

Roopya integrates with all major Indian credit bureaus and alternative financial data systems for AI-enhanced credit decisioning.

3. AI-Based Fraud Prevention

Fraud management has become mission critical for NBFCs.

Modern fraud engines should detect:

- Identity duplication

- Device fingerprint mismatch

- Geo-location anomalies

- Fake documents

- Application velocity risks

- Behavioral inconsistencies

AI-powered fraud systems can reportedly reduce fraudulent disbursements significantly.

4. Real-Time Lending Analytics

NBFCs require complete visibility into their lending operations.

A modern analytics engine should provide:

- Approval ratios

- Rejection trends

- Portfolio segmentation

- Risk concentration

- Collection efficiency

- Delinquency prediction

- Customer acquisition metrics

- TAT analysis

Roopya’s lending analytics suite offers portfolio-level intelligence and predictive delinquency monitoring.

5. Business Rule Engine (BRE)

Every lender has different underwriting policies.

A no-code BRE allows teams to configure:

- Eligibility criteria

- Bureau score thresholds

- Income requirements

- Risk segmentation

- Loan limits

- Approval hierarchies

This removes dependency on development teams and enables faster operational changes.

6. Omnichannel Borrower Onboarding

Borrowers today expect seamless onboarding across:

- Mobile apps

- Websites

- DSA portals

- API integrations

- WhatsApp journeys

The platform should maintain a consistent onboarding experience regardless of channel.

7. Integrated E-Sign and Agreement Management

Once KYC and underwriting are completed, the borrower journey should continue seamlessly.

Required features include:

- Digital sanction letters

- E-sign integration

- Loan agreement automation

- Consent management

- Digital document vaults

This enables fully paperless lending operations.

8. Early Warning Systems (EWS)

Risk management does not end after disbursement.

Modern lending platforms must support:

- AI-driven delinquency prediction

- Risk alerts

- Portfolio health monitoring

- Behavioral analytics

- Collections prioritization

Roopya’s Early Warning System uses predictive models to identify high-risk accounts before default occurs.

How AI is Transforming Video KYC and Credit Risk

Artificial Intelligence is fundamentally reshaping lending operations.

Traditional underwriting relied heavily on:

- Bureau scores

- Income proofs

- Manual verification

However, AI-driven systems now evaluate:

- Banking behavior

- GST patterns

- Device intelligence

- Transaction trends

- Employment stability

- Digital footprints

- Cashflow analytics

This allows lenders to underwrite borrowers with thin credit files more accurately.

Roopya highlights how AI models improve approval quality, reduce defaults, and accelerate decision-making across the lending lifecycle.

Benefits of AI-Powered Video KYC for NBFCs

Faster Loan Processing

AI automation can reduce onboarding times from days to minutes.

Reduced Operational Costs

Manual verification teams become smaller while productivity increases significantly.

Better Fraud Prevention

AI engines can detect anomalies far faster than manual reviewers.

Higher Customer Conversion

Faster onboarding reduces drop-offs during loan applications.

Improved Compliance

Automated audit trails simplify regulatory reporting and inspections.

Smarter Credit Decisions

Alternative data and AI models help identify good borrowers beyond traditional bureau metrics.

Challenges NBFCs Face Without Modern Video KYC Systems

NBFCs still relying on outdated onboarding processes face serious operational challenges.

These include:

- Manual processing delays

- Compliance gaps

- Higher fraud exposure

- Customer drop-offs

- Poor scalability

- Increased operational costs

- Limited risk visibility

As competition intensifies, legacy systems will struggle to keep pace with digital-first lenders.

Why Cloud-Native Lending Platforms Are the Future

Cloud-native infrastructure offers major advantages for modern lenders:

- Faster deployment

- Scalability

- API integrations

- Real-time updates

- Lower infrastructure costs

- Better uptime

- Continuous compliance upgrades

Roopya positions itself as a cloud-native, no-code lending platform that allows lenders to go live rapidly while integrating Video KYC, LOS, LMS, analytics, and collections into one ecosystem.

The Role of Account Aggregators in Credit Risk

The Account Aggregator (AA) ecosystem is transforming underwriting in India.

With borrower consent, lenders can access:

- Banking transactions

- Cashflow data

- Income behavior

- Financial patterns

This provides a more accurate view of borrower risk than bureau scores alone.

Modern lending platforms must integrate seamlessly with the AA framework to remain competitive.

Video KYC and Customer Experience

Compliance should never come at the cost of user experience.

The best Video KYC journeys are:

- Mobile-first

- Multilingual

- Fast-loading

- Low-bandwidth optimized

- Intuitive

- Paperless

A frictionless onboarding experience directly improves conversion rates and customer satisfaction.

Future Trends in Video KYC and Digital Lending

The future of digital lending will be driven by:

AI-Based Underwriting

Machine learning models will increasingly replace rule-based underwriting.

Hyper-Personalized Loan Offers

Platforms will tailor credit products dynamically based on borrower behavior.

Real-Time Risk Monitoring

Continuous monitoring will replace static underwriting models.

Voice AI and Conversational Onboarding

AI agents will assist borrowers during KYC and loan application flows.

Advanced Fraud Intelligence

Behavioral biometrics and deepfake detection will become standard.

Why Roopya is Built for Modern NBFC Lending

Roopya provides a unified lending infrastructure designed specifically for Indian NBFCs, fintech lenders, MFIs, and banks.

Key capabilities include:

- Loan Origination System (LOS)

- Loan Management System (LMS)

- AI-powered underwriting

- Video KYC support

- OCR verification

- Business Rule Engine

- Lending analytics

- Fraud detection

- Early Warning Systems

- Bureau integrations

- Account Aggregator integrations

- E-sign workflows

- Collections management

The platform is designed to help lenders automate onboarding, accelerate approvals, improve compliance, and reduce credit risk.

Video KYC compliance is no longer just a regulatory checkbox for NBFCs. It is the foundation of scalable, secure, and intelligent digital lending.

As fraud risks rise and borrower expectations evolve, lenders need platforms that combine:

- RBI-compliant Video KYC

- AI-driven underwriting

- Real-time analytics

- Fraud prevention

- Credit risk automation

- Cloud-native scalability

The lenders that succeed in 2026 will be the ones that can balance compliance, customer experience, and intelligent automation simultaneously.

Platforms like Roopya are enabling NBFCs to modernize their entire lending lifecycle — from borrower onboarding to collections — using AI-powered digital lending infrastructure built for India’s rapidly evolving financial ecosystem.