What is a Loan Origination System? Complete Guide for Banks, NBFCs & Fintechs in India (2026)

If you work in banking, lending, or fintech in India — you’ve heard the term Loan Origination System more times than you can count. But what exactly is it? How does it work? And why does choosing the right one determine whether your lending business grows or stagnates?

India’s lending ecosystem is at an inflection point. With loan growth projected at 12%+ in FY2026, the RBI Digital Lending Directions now in effect, and an MSME credit— financial institutions no longer have the luxury of relying on slow, manual processes.

This guide answers every question you have about Loan Origination Systems: what they are, how they work, what features matter in 2026, and how to choose the right one for your institution. Whether you’re an NBFC, bank, MFI, or fintech — read this before you evaluate a single vendor.

Start Free Trial

What is a Loan Origination System (LOS)?

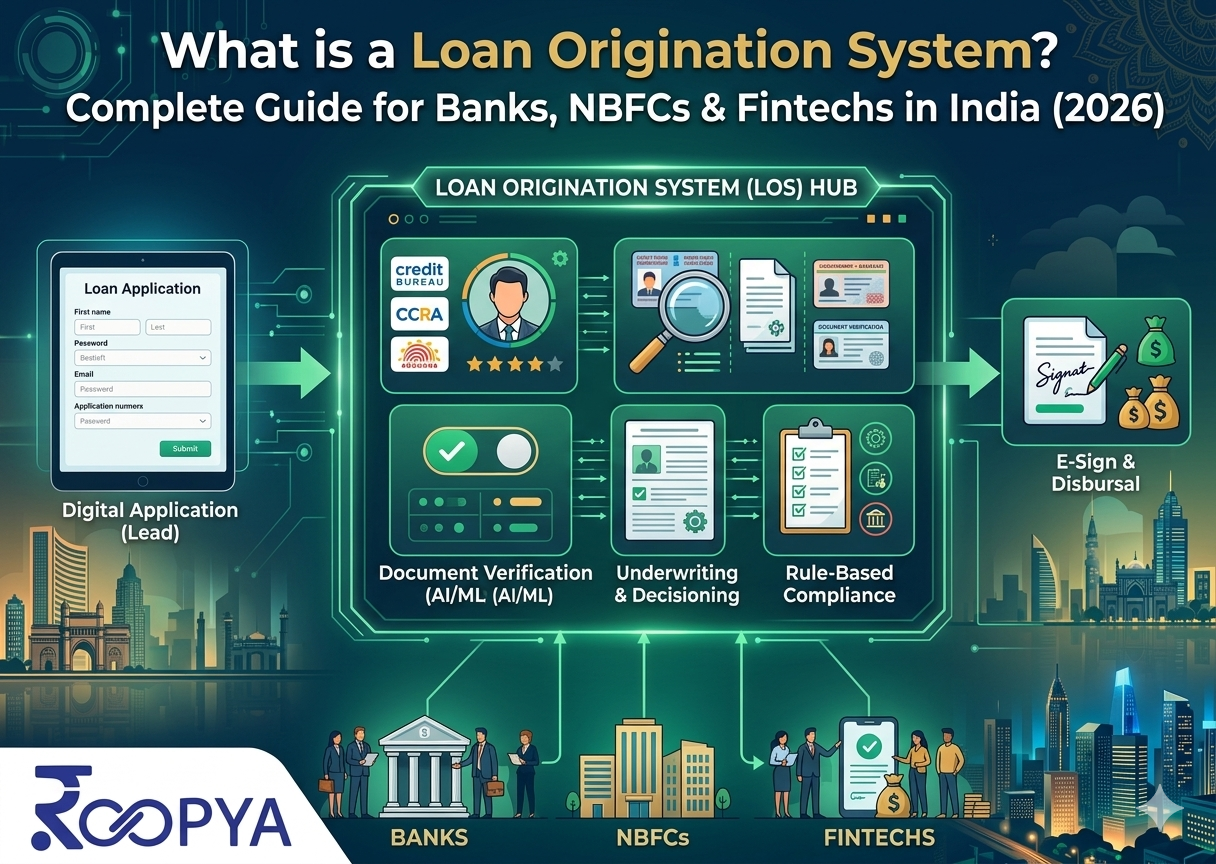

A Loan Origination System (LOS) is a digital software platform that manages and automates the entire front-end lending process — from the moment a borrower applies for a loan to the moment it is approved and ready for disbursement.

In simpler terms: a LOS replaces paperwork, manual checks, and siloed spreadsheets with automated, intelligent workflows. It captures borrower data, runs KYC and credit bureau checks, evaluates risk, applies your business rules, and routes applications through structured approval workflows — all without requiring manual intervention at every step.

Quick Definition: A Loan Origination System (LOS) is technology that automates the loan application, credit assessment, underwriting, and approval process for banks, NBFCs, and financial institutions.

Every lender — from a large public sector bank to a new-age NBFC — needs a LOS. The difference is in how fast, how smart, and how compliant that system is.

How Does a Loan Origination System Work?

A modern LOS manages the full origination lifecycle across eight key stages:

Stage 1: Lead Capture & Application Intake

The LOS captures loan applications from multiple channels — web portals, mobile apps, agent tablets, branch systems, or embedded finance integrations. Borrower data (personal, financial, employment) is collected digitally, eliminating paper forms and manual data entry.

Stage 2: Document Collection & KYC

The LOS prompts borrowers to upload required documents (ID proof, income statements, bank statements, GST filings) and runs automated KYC checks via Aadhaar-based e-KYC, CKYC, PAN verification, and Video KYC (V-CIP) — all as per RBI norms.

Stage 3: Credit Bureau Checks

The system pulls real-time credit reports from CIBIL, Experian, Equifax, and CRIF simultaneously. Bureau scores, repayment history, outstanding liabilities, and default flags are assessed automatically. No manual bureau pulls, no delays.

Stage 4: Alternate Data Analysis

Modern LOS platforms go beyond bureau scores. They analyze GST filing data, bank statement OCR, Account Aggregator (AA) data, utility payment records, and behavioral signals to build a complete risk picture — especially critical for MSME borrowers with thin credit files.

Stage 5: Credit Decisioning via Business Rule Engine (BRE)

The LOS applies your credit policy through a Business Rule Engine. Rules covering minimum income, FOIR (Fixed Obligation to Income Ratio), bureau score thresholds, geographic risk, product eligibility, and fraud flags are evaluated automatically. A configurable BRE means your credit team can update rules without raising IT tickets.

Stage 6: Fraud Detection & Risk Scoring

AI-powered fraud modules run in parallel — checking for duplicate applications, identity mismatches, watchlist hits (CIBIL defaulter list, PMLA lists), device fingerprinting, and application velocity. Risk scores are generated in real time.

Stage 7: Approval, Offer Generation & E-Signing

Based on decisioning outcomes, the LOS generates a customized loan offer, sanction letter, and loan agreement — automatically. The borrower reviews and e-signs digitally. No physical documentation, no courier delays.

Stage 8: Disbursement Trigger

Upon e-signing and final verification, the LOS triggers disbursement instructions to the payment system. Loan data is then handed off to the Loan Management System (LMS) for post-disbursement servicing.

The entire process — from application to disbursement trigger — can happen in under two minutes on a well-configured modern LOS.

Loan Origination System vs Loan Management System: What’s the Difference?

This is one of the most common questions in digital lending, and the confusion is understandable — both systems are part of the same lending lifecycle.

Here’s the definitive breakdown:

| Dimension | Loan Origination System (LOS) | Loan Management System (LMS) |

| Phase | Pre-disbursement (front-end) | Post-disbursement (back-end) |

| Core function | Application → Approval → Disbursement trigger | Repayment → Servicing → Closure |

| Primary users | Credit officers, underwriters, sales teams | Operations, collections, finance teams |

| Key processes | KYC, credit scoring, BRE, fraud detection | EMI schedules, NACH, NPA tracking, collections |

| Data managed | Applicant data, credit data, documents | Loan portfolio, payment history, dues |

| Customer interaction | Borrower-facing (application experience) | Ongoing borrower relationship |

| RBI compliance focus | Digital Lending Directions, KYC norms, credit model explainability | NPA classification, SARFAESI, co-lending reporting |

| When it activates | From lead capture to loan sanction | From first EMI to loan closure |

Do you need both?

Yes — and the best approach is to use a unified platform that combines LOS and LMS on a single data architecture. Separate systems create data silos: a borrower’s application data entered in the LOS must be re-entered or migrated to the LMS, causing errors, delays, and compliance gaps.

Platforms like Roopya unify LOS, LMS, Collections, Early Warning System, and Lending Analytics on one platform — eliminating all data migration and integration overhead between origination and servicing.

Why India’s Lending Market Needs a Modern LOS Right Now

-

The RBI Digital Lending Directions 2025 Are In Force

The RBI’s updated Digital Lending Directions (effective 2025) set strict requirements for lenders: explainable AI credit decisions (Model Risk Circular, August 2024), mandatory audit trails, KYC compliance via V-CIP, data localization in India, and structured co-lending architecture. An outdated LOS that cannot meet these requirements creates direct regulatory and reputational risk.

-

India’s MSME Credit Gap Is $380 Billion — And Growing

Between April 2025 and January 2026, public sector banks sanctioned over ₹52,300 crore in MSME loans using GST-based digital underwriting. Lenders who can analyze GST filings, bank statements, and Account Aggregator data at origination will capture this market. That requires a sophisticated LOS — not one built only for salaried borrowers with CIBIL scores.

-

Borrowers Expect 2-Minute Approvals — No Exceptions

Fintech lenders have permanently reset borrower expectations. If your LOS takes 24–48 hours to process a personal loan, you’re losing customers to competitors who do it in under two minutes. Speed is no longer a differentiator — it’s a baseline requirement.

-

Drop-Off Rates Are Killing Lenders With Outdated Systems

Studies show that digital loan application drop-off rates frequently exceed 60%. Poor UX, too many manual steps, and slow document verification cause borrowers to abandon applications mid-way. A modern LOS reduces friction at every stage, dramatically lowering drop-off rates.

-

The Indian LOS Market Is at $7.2 Billion and Growing at 20%+ CAGR

The loan origination software market in India is projected to reach USD 7.157 billion in 2026. The institutions investing in modern LOS infrastructure now are building a structural competitive advantage that compounds over the next five years.

Must-Have Features of a Loan Origination System in 2026

Not every LOS is built for the Indian lending environment. Here are the features that genuinely matter:

-

No-Code Business Rule Engine (BRE)

Your credit policy will evolve. Products will change. Regulations will update. A LOS that requires developer involvement every time you adjust a credit rule is a bottleneck that costs money and time. A true no-code BRE lets your credit and product teams configure, test, and deploy rules through a visual interface — without a single line of code.

What to ask vendors: “Can my business team add a new income-to-EMI rule without raising a tech ticket?” If the answer involves a sprint cycle, walk away.

-

Alternate Data Integration (GST, AA, Bank Statements)

Traditional bureau scores exclude millions of creditworthy borrowers — especially MSMEs, gig workers, and thin-file individuals. The best LOS platforms integrate:

- GST filing analysis — actual turnover, tax compliance, business health

- Account Aggregator (AA) data — RBI-approved financial data sharing

- Bank statement OCR — automated extraction of transaction patterns

- Behavioral data — app usage, repayment intent signals

-

Pre-Integrated API Ecosystem

Building API integrations from scratch takes months and costs lakhs. A LOS with a large library of pre-integrated APIs — covering credit bureaus, KYC providers, e-mandate, payment gateways, e-signature, and fraud databases — saves enormous time and reduces technical risk.

Roopya offers 300+ pre-integrated APIs covering the complete Indian lending infrastructure stack.

-

AI-Powered Fraud Detection

Fraud at origination is the fastest-growing risk for Indian NBFCs. A modern LOS should include: duplicate application detection, Aadhaar fraud checks, liveness detection in video KYC, device fingerprinting, application velocity monitoring, and watchlist screening against PMLA, CIBIL defaulter, and other regulatory lists.

-

Omnichannel Loan Application Experience

Borrowers don’t just apply on websites. They apply via:

- Mobile apps (self-service)

- Agent-assisted tablets (field collection)

- Branch systems (walk-in)

- WhatsApp / embedded widgets (assisted digital)

- Partner portals (DSA, connector networks)

Your LOS must deliver a consistent, seamless experience across all channels, including offline capability for agents in low-connectivity areas.

Sub-60-second decisions for standard consumer loans are now expected. This requires your LOS to simultaneously orchestrate bureau pulls, fraud checks, BRE evaluation, and offer generation — in parallel, not sequentially.

-

RBI-Compliant Audit Trails

Every credit decision must be logged with explainability: which data points were considered, what rules were applied, and why the application was approved or rejected. This is not just a compliance requirement — it’s also a risk management tool for portfolio review.

-

Configurable Loan Products Without Coding

Launching a new loan product (say, a GST-linked MSME overdraft or a digital gold loan) should not require months of development. A modern LOS lets you configure new loan products, workflows, and eligibility criteria through an intuitive dashboard — in hours, not months.

-

Co-Lending Architecture (RBI Co-Lending Directions 2025)

If you operate co-lending arrangements with banks, your LOS must support: dual NPA classification, partner-specific EMI splits, co-origination workflows, and month-end reconciliation as per the RBI’s updated Co-Lending Directions.

-

Integrated Collections & Early Warning

The best LOS platforms extend beyond origination to include early warning signals — behavioral indicators that predict default risk at 30, 60, or 90 DPD. Identifying at-risk accounts during the loan lifecycle (not after they’ve defaulted) dramatically improves collection outcomes.

Types of Loan Origination Systems

Not all LOS platforms are architecturally the same. Understanding the types helps you make the right choice:

Cloud-Based LOS vs On-Premise LOS

| Cloud-Based LOS | On-Premise LOS | |

| Deployment | Hosted on vendor’s cloud (AWS/Azure/GCP) | Installed on your own servers |

| Setup time | Days to weeks | Months to years |

| Cost model | Subscription / usage-based | Upfront license + hardware |

| Maintenance | Vendor managed | Internal IT team required |

| Scalability | Instant, elastic | Requires hardware upgrades |

| RBI compliance updates | Automatic | Manual patching |

| Best for | NBFCs, fintechs, growing lenders | Large banks with existing infrastructure |

Recommendation: For most Indian NBFCs and fintechs in 2026, a cloud-based LOS is the clear choice — faster go-live, lower cost, automatic compliance updates, and elastic scaling.

No-Code vs Low-Code vs Custom-Built LOS

No-Code LOS (e.g., Roopya): Business teams configure everything — products, rules, workflows, reports — without developer involvement. Fastest to go live. Best for NBFCs that want agility without a large tech team.

Low-Code LOS (e.g., Newgen): Requires some technical configuration but less than fully custom builds. Suitable for institutions with internal tech capability that want customization without starting from scratch.

Custom-Built LOS: Built from ground up by an internal tech team or outsourced to a software vendor. Full control, but typically 12–24 months to deploy and extremely expensive to maintain. Only suitable for the largest banks with deep technical resources.

Benefits of a Loan Origination System for NBFCs, Banks & Fintechs

Operational Benefits

- 10x faster loan processing — from days to minutes

- 60–70% reduction in processing time for standard applications

- Zero paper documentation — end-to-end digital origination

- Elimination of manual data entry errors — single source of truth

Financial Benefits

- Lower cost per loan — fewer FTEs required for processing

- Higher throughput — process 10x the volume with the same team

- Reduced fraud losses — AI detection at origination

- Better portfolio quality — more accurate credit decisions from the start

Compliance Benefits

- Always-current RBI compliance — cloud platforms update automatically

- Audit-ready credit decision logs — explainable AI as required by RBI

- Reduced regulatory penalties — no manual compliance gaps

Customer Experience Benefits

- Sub-2-minute approvals for digital loan products

- Paperless onboarding — borrowers complete everything on mobile

- Real-time status updates — no more “call us tomorrow”

- Higher satisfaction scores — faster, transparent, friction-free process

Growth Benefits

- Launch new loan products in days — not months

- Scale geographically — no physical infrastructure needed

- Serve new borrower segments — alternate data enables MSME and thin-file lending

- Expand distribution — DSA portals, embedded finance, WhatsApp origination

The Loan Origination Process in India: 8 Stages in Detail

Stage 1: Lead Management & Pre-Qualification

Digital leads from marketing campaigns, DSA referrals, and self-service portals enter the LOS. Pre-qualification checks (basic eligibility, product fit) filter out ineligible applications automatically, saving credit team bandwidth.

Stage 2: Digital Application & Data Capture

Borrowers complete a smart digital application form. Fields are pre-populated where possible (using Aadhaar data, bureau data). Required documents are prompted contextually based on loan product and borrower type.

Stage 3: KYC & Identity Verification

Aadhaar-based e-KYC or Video KYC (V-CIP) is conducted as per RBI guidelines. PAN verification, CKYC registry check, and face liveness detection run automatically. Identity fraud signals are flagged in real time.

Stage 4: Financial Document Analysis

Bank statements, salary slips, ITR filings, GST returns, and CA-certified financials are uploaded and analyzed by AI. OCR extracts financial data automatically. Bank statement analyzer identifies income patterns, obligations, and anomalies.

Stage 5: Credit Bureau & Alternate Data Pull

Multi-bureau credit reports are pulled simultaneously (CIBIL, Experian, Equifax, CRIF). Account Aggregator data is fetched with borrower consent. GST data is analyzed for MSME applicants. All data feeds into the credit scoring model.

Stage 6: Credit Decision via BRE

The Business Rule Engine applies your credit policy: minimum credit score, FOIR limits, geographic risk, product-specific rules, bureau derogatory checks. AI models supplement rule-based decisioning with predictive scores. Final decision — approve, decline, or refer to manual review — is generated in seconds.

Stage 7: Offer Generation & Legal Documentation

Approved applications receive automated loan offer letters with specific terms (amount, rate, tenure, EMI). Loan agreements and sanction letters are generated from pre-approved legal templates. E-signing is completed digitally via Aadhaar e-Sign or DSC.

Stage 8: Disbursement Trigger & LMS Handoff

Final sanction is confirmed. Disbursement instruction is triggered to the payment system (IMPS/NEFT/UPI). All loan data — borrower details, loan terms, documentation — is transferred to the LMS for servicing. The origination cycle is complete.

How to Choose the Right Loan Origination System: 7-Point Evaluation Framework

-

Define Your Loan Product Mix First

A personal loan LOS workflow is fundamentally different from an MSME LAP or a microfinance JLG product. Before evaluating any vendor, list every loan product you currently offer and plan to launch in the next 2 years. Eliminate platforms that cannot handle your full product spectrum without custom development.

-

Assess Your Technical Capacity

If you have a 5-person tech team, a complex enterprise platform requiring extensive configuration will stall for months. Be honest about your team’s technical capacity and prioritize platforms that match it. No-code platforms like Roopya are specifically designed for NBFCs that want agility without a large engineering team.

-

Map Every Compliance Requirement

Make a checklist of your specific RBI compliance requirements: V-CIP KYC, co-lending architecture, model explainability, credit information bureau integration, and so on. Ask every vendor to demonstrate compliance against each item — not just claim it.

-

Evaluate Implementation Timeline Rigorously

“Go live in 4 weeks” sounds great in a sales deck. Ask vendors: “Show me your last three customer implementations — actual days from contract signing to first live loan disbursement.” This one question reveals more than any feature demonstration.

-

Challenge the Pricing Model

Upfront licensing costs of ₹50 lakh to ₹5 crore can cripple a growing NBFC’s cash flow before the platform even generates ROI. Usage-based pricing (paying per loan disbursed or per active borrower) aligns vendor incentives with your growth. Roopya’s pay-per-use model is specifically designed for this reality.

-

Demand a Live Demo of Rule Configuration

Ask the vendor: “Please change this income threshold rule from 30% to 25% FOIR right now — without a developer.” If they can’t do it in your presence in under 5 minutes, your business team will be waiting on tech tickets every time your credit policy evolves.

-

Verify the Integration Ecosystem

List your required integrations: which credit bureaus, which KYC providers, which e-mandate provider, which e-signature vendor, which payment gateway. Ask the vendor which of these are pre-built vs require custom development. Custom integrations take weeks and cost money.

Roopya: India’s Fastest, Most Integrated Loan Origination System

Roopya is a unified no-code lending infrastructure platform built specifically for the realities of Indian lending in 2026.

What Makes Roopya Different

Go Live in 1 Day Roopya’s plug-and-play onboarding is the fastest in the Indian LOS market. From contract to first live loan disbursement in 24 hours. No 6-month implementation cycles. No armies of consultants.

Truly No-Code Platform Every configuration in Roopya — loan products, credit rules, approval workflows, reports, dashboards — is managed through an intuitive visual interface. Your credit manager can update a BRE rule without a developer. Your product team can launch a new loan product without a sprint cycle.

300+ Pre-Integrated APIs Roopya comes pre-integrated with the complete Indian lending API ecosystem:

- Credit bureaus: CIBIL, Experian, Equifax, CRIF

- KYC: Aadhaar e-KYC, Video KYC, CKYC, PAN

- Account Aggregator framework

- E-mandate (NACH, UPI AutoPay)

- Payment gateways & UPI

- E-signature: Aadhaar e-Sign, DSC

- Bank statement analyzers

- GST verification APIs

- 270+ more integrations ready to activate

Pay-As-You-Use — Zero Upfront Cost No licensing fees. No implementation costs. Pay only for what you actually process. This makes Roopya accessible to new NBFCs and growing lenders who want to go digital without tying up CapEx.

Unified LOS + LMS + Collections + Analytics Roopya is not just a LOS — it is a complete lending infrastructure platform. LOS, Loan Management System, Collections System, Early Warning System, and Lending Analytics all run on a single platform with a unified data layer. No data migration. No integration overhead. No silos between origination and servicing.

AI-Powered Lending at Every Stage

- AI document OCR — 99%+ accuracy on ID and financial documents

- AI credit scoring — 40% better accuracy vs traditional models

- AI fraud detection — 80% fraud reduction

- AI early warning — predict defaults before they happen

- AI analytics — natural language reporting and portfolio insights

RBI-Compliant by Design Roopya’s platform is continuously updated to reflect RBI’s evolving digital lending regulations — including the Digital Lending Directions, Model Risk Circular requirements, co-lending architecture, and KYC norms. Compliance updates happen automatically, not through expensive consulting engagements.

Trusted by India’s Modern Lenders IndiaKaLoan, QuickFinShop, Recapita, Findoc, EazyCredit, Loan Seva, and many more NBFCs and fintechs have built their digital lending operations on Roopya.

Schedule a Free Demo — Go Live Tomorrow →

A Loan Origination System is no longer optional infrastructure — it is the foundation of every competitive lending operation in India in 2026.

The right LOS reduces your cost per loan, improves portfolio quality, eliminates compliance risk, and enables you to launch new products at the speed the market demands. The wrong one creates bottlenecks that compound over years.

When evaluating a LOS, look beyond the feature checklist. Ask about implementation speed. Challenge pricing assumptions. Demand live demos of rule configuration. And make sure every integration you need is pre-built — not on a future roadmap.

Roopya is built for exactly this environment: India’s most regulated, most competitive, and fastest-growing lending market. Go live in 1 day. Pay only for what you use. Configure everything without code.