No-Code LOS: How to Launch a New Loan Product in 7 Days Without Developers

The lending industry is evolving faster than ever. NBFCs, fintech lenders, microfinance institutions, banks, and digital lending startups are constantly under pressure to launch new loan products quickly. Whether it is a personal loan, MSME loan, BNPL product, gold loan, education loan, or embedded finance offering, speed-to-market has become one of the biggest competitive advantages.

Traditionally, launching a new loan product required months of development work. Lenders had to depend heavily on software developers, IT vendors, integration teams, and lengthy implementation cycles. Even a small change in underwriting rules or workflow configurations often required coding, testing, deployment, and approvals.

Today, things have changed dramatically.

Modern no-code Loan Origination Systems (LOS) like Roopya allow lenders to launch fully digital lending products in as little as 7 days — without writing a single line of code. These platforms empower business teams, credit managers, and operations teams to configure workflows, underwriting rules, customer journeys, KYC flows, bureau integrations, and approval logic directly from a visual interface.

This shift is transforming how financial institutions innovate in lending.

Start Free Trial

What Is a No-Code Loan Origination System (LOS)?

A no-code Loan Origination System is a digital lending platform that allows lenders to create, configure, and manage loan products without software development.

Instead of relying on developers for every modification, users can configure:

- Loan application journeys

- Eligibility rules

- Credit policies

- Bureau score conditions

- KYC workflows

- Risk assessment logic

- Approval matrices

- Document verification flows

- Loan disbursement rules

- Customer onboarding processes

through a drag-and-drop or visual interface.

Platforms like Roopya LOS Platform provide automated workflows, configurable pipelines, third-party integrations, BRE (Business Rule Engine), underwriting automation, and customer onboarding capabilities that significantly reduce deployment time.

Why Traditional LOS Deployments Take Too Long

Most legacy lending systems were not designed for rapid innovation. Traditional implementations usually involve:

1. Heavy Dependency on Developers

Every change requires coding:

- Adding a new field

- Updating eligibility rules

- Modifying workflows

- Integrating APIs

- Changing EMI calculations

This slows product launches significantly.

2. Long Testing Cycles

Even small changes require:

- QA testing

- UAT approvals

- Deployment validation

- Regression testing

The process can take weeks or months.

3. Rigid System Architecture

Legacy systems are difficult to customize. Many lenders struggle with:

- Fixed workflows

- Hardcoded underwriting logic

- Limited integrations

- Poor scalability

4. Delayed Market Response

When competitors launch products faster, traditional lenders lose opportunities in:

- Embedded finance

- BNPL

- MSME lending

- Co-lending

- Consumer durable financing

Why No-Code LOS Is the Future of Digital Lending

Modern lenders need flexibility, agility, and faster execution.

According to industry discussions around lending technology, configurability and rapid product deployment have become more important than traditional feature-heavy systems.

A no-code LOS solves this challenge by enabling:

- Faster go-live

- Instant product changes

- Reduced IT dependency

- Lower operational costs

- Faster compliance updates

- Better customer experience

- Easier scaling

Platforms like Roopya Digital Lending Software are designed specifically for modern NBFCs and fintech lenders looking to automate the entire lending lifecycle from origination to collections.

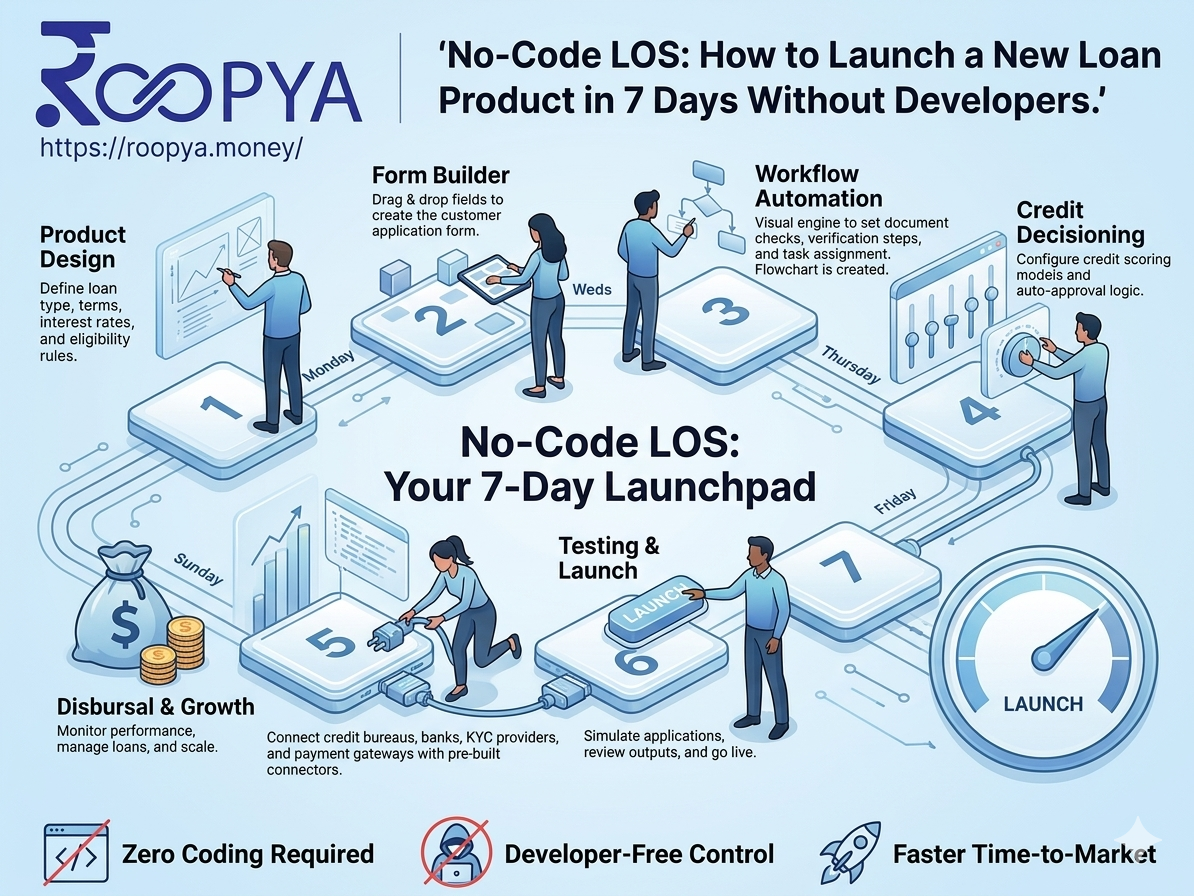

How to Launch a New Loan Product in 7 Days Using No-Code LOS

Day 1: Define Your Loan Product

The first step is to finalize the product structure.

You need to define:

- Loan type

- Ticket size

- Interest rate

- Tenure

- Eligibility criteria

- Target customer segment

- Repayment frequency

- Risk policies

Example:

- Personal Loan

- ₹25,000 to ₹5,00,000

- 12–36 months tenure

- Salaried professionals

- Minimum CIBIL score 700

With a no-code LOS, these parameters can be configured directly from the admin panel.

Day 2: Configure Customer Journey

Modern LOS platforms allow lenders to build custom onboarding journeys visually.

You can configure:

- Mobile-first applications

- Web journeys

- Partner journeys

- Assisted onboarding

- Embedded finance journeys

Roopya enables lenders to create custom customer onboarding journeys for different loan products without development work.

Common Journey Stages

- Lead Capture

- Mobile OTP Verification

- PAN Verification

- Aadhaar KYC

- Bank Statement Analysis

- Bureau Check

- Eligibility Decision

- E-sign

- Disbursement

Automated Workflow Creation

A no-code LOS allows lenders to configure workflows using visual process builders.

Example Workflow

Lead Received → KYC Verification → Bureau Pull → Risk Analysis → Underwriting → Approval → Disbursement

This eliminates the need for developers to manually code workflows.

Day 3: Configure Business Rules Engine (BRE)

The BRE is the heart of automated underwriting.

Using no-code configuration, lenders can define rules such as:

Eligibility Rules

- Age between 21–60

- Monthly income above ₹25,000

- Minimum bureau score 700

Risk Rules

- Reject if DPD > 30

- Reject if FOIR > 50%

- Auto-approve low-risk profiles

Fraud Rules

- Mobile mismatch detection

- Device risk checks

- Duplicate application checks

Roopya supports automated decision-making and configurable underwriting logic through its rule engines and scorecards.

Day 4: Enable API Integrations

Digital lending requires seamless integrations.

A modern no-code LOS typically supports plug-and-play integrations with:

- CKYC

- DigiLocker

- Aadhaar eKYC

- PAN Verification

- Credit Bureaus

- Account Aggregator

- Bank Statement Analyzers

- Payment Gateways

- eSign Providers

- SMS Gateways

- WhatsApp APIs

Roopya offers ready third-party integrations and API-first infrastructure for lenders.

Day 5: Configure Credit Underwriting

Traditional underwriting takes time because it depends heavily on manual assessment.

A no-code LOS automates:

- Credit scoring

- Risk segmentation

- Income estimation

- Alternate data analysis

- Fraud checks

Roopya provides AI-driven analytics and alternative data assessment capabilities to improve underwriting decisions.

Day 6: Test and Simulate Loan Journeys

Before launch, lenders can simulate:

- Application journeys

- Approval flows

- Rejection scenarios

- EMI schedules

- Disbursement processes

Testing ensures:

- Accurate underwriting

- Proper workflow execution

- Compliance validation

- Faster production deployment

Because the system is configurable, changes can be made instantly without waiting for development cycles.

Day 7: Go Live

After testing, the product can be deployed immediately.

Modern no-code platforms significantly reduce implementation timelines. Roopya states that lenders can go live quickly using plug-and-play infrastructure and configurable workflows.

Key Features of a No-Code LOS

1. Drag-and-Drop Workflow Builder

Business users can configure journeys without coding.

2. Dynamic Application Forms

Create product-specific application forms instantly.

3. Automated Underwriting

Reduce manual approvals using AI and rule-based decisioning.

4. Multi-Product Management

Manage multiple lending products from a single dashboard.

Roopya supports multiple loan product pipelines and configurable workflows.

5. Bureau Integrations

Connect with:

- CIBIL

- Experian

- Equifax

- CRIF

6. Real-Time Decisioning

Enable instant loan approvals.

7. Compliance Automation

Ensure RBI-compliant lending operations.

Benefits of No-Code LOS for NBFCs

Faster Product Launches

Launch new products within days instead of months.

Reduced IT Costs

No large development teams required.

Better Customer Experience

Digital onboarding improves conversion rates.

Improved Operational Efficiency

Automation reduces manual work and errors.

Faster Underwriting

AI-driven underwriting accelerates approvals.

Scalability

Expand into new lending categories quickly.

Use Cases of No-Code LOS

Personal Loans

Launch fully digital unsecured lending products.

MSME Loans

Automate business loan underwriting.

Gold Loans

Digitize onboarding and valuation workflows.

BNPL

Enable embedded finance journeys.

Co-Lending

Support multi-lender workflows and reconciliation.

Education Loans

Create student-focused onboarding journeys.

Why NBFCs Prefer No-Code Lending Platforms

Indian NBFCs face intense competition from:

- Fintech startups

- Neo banks

- Embedded finance providers

- Digital lending apps

To stay competitive, lenders need:

- Faster innovation

- Lower operational costs

- Better compliance

- Rapid product deployment

Industry discussions increasingly highlight no-code configurability as a critical advantage for modern lending platforms.

RBI Compliance and Digital Lending

The RBI digital lending guidelines emphasize:

- Transparent lending

- Secure borrower data

- Direct disbursement

- Regulatory compliance

- Grievance management

Modern LOS platforms help lenders remain compliant through:

- Audit trails

- Consent management

- Secure APIs

- Data governance

- Rule-based compliance

Challenges Solved by No-Code LOS

| Traditional Challenge | No-Code LOS Solution |

|---|---|

| Long implementation cycles | Faster deployment |

| Developer dependency | Business-led configuration |

| Manual underwriting | Automated decisioning |

| Slow integrations | Pre-built APIs |

| Limited scalability | Flexible workflows |

| High operational costs | Automation-driven efficiency |

| Delayed product launches | Rapid go-live |

How Roopya Helps Launch Loan Products Faster

Roopya LOS Platform provides:

- No-code lending workflows

- Automated underwriting

- Multi-product pipelines

- API-first infrastructure

- BRE configuration

- AI-driven analytics

- Customer onboarding

- Bureau integrations

- KYC automation

- Digital disbursement workflows

The platform is designed to help NBFCs, fintechs, and lenders rapidly scale digital lending operations while reducing operational complexity.

Future of No-Code Lending Infrastructure

The future of lending will be driven by:

- AI-powered underwriting

- Embedded finance

- Hyper-personalized lending

- Account Aggregator ecosystems

- Real-time credit decisioning

- API banking

- Automated collections

No-code infrastructure will become essential because lenders need the ability to launch and modify products rapidly without depending on developers.

Financial institutions that adopt configurable digital lending systems today will gain a significant competitive advantage tomorrow.

Launching a new loan product no longer requires months of development effort, expensive IT projects, or complex implementation cycles.

With modern no-code Loan Origination Systems like Roopya, lenders can:

- Configure workflows

- Automate underwriting

- Integrate KYC and bureaus

- Build customer journeys

- Ensure compliance

- Deploy products rapidly

all without writing code.

In a highly competitive lending market, speed, flexibility, and automation are now essential. A no-code LOS empowers NBFCs and fintech lenders to innovate faster, reduce operational costs, improve customer experience, and scale digital lending efficiently.