How to Choose a Loan Origination System in India

The Digital Lending Revolution in India

A Comprehensive Guide for NBFCs and Fintech Startups.Strategic Framework for Digital Lending Transformation

India’s lending landscape has undergone a seismic transformation over the past decade. With the rise of digital financial services, Non-Banking Financial Companies (NBFCs) and Fintech startups are no longer competing solely on interest rates or branch networks. Today, the speed of credit decisioning, the quality of borrower experience, and the sophistication of risk management are the true battlegrounds for market leadership.

Start Free Trial

At the heart of this transformation lies the Loan Origination System (LOS) — the technology platform that manages the entire lifecycle of a loan application, from the moment a borrower submits a request to the final disbursement of funds. Choosing the right LOS is arguably one of the most consequential technology decisions an NBFC or Fintech startup will ever make. A well-chosen platform can compress loan processing timelines from days to minutes, dramatically reduce operational costs, improve regulatory compliance, and deliver a borrower experience that generates loyalty and referrals.

Conversely, a poor LOS choice can create operational nightmares — rigid workflows that cannot adapt to changing products, compliance gaps that attract regulatory scrutiny, and integration failures that slow down growth. In a sector where agility and scale are non-negotiable, the wrong platform can be a company-threatening mistake.

This guide is designed to help decision-makers at NBFCs and Fintech startups navigate the complex landscape of LOS solutions available in India. Whether you are a new entrant building your first lending platform or an established player looking to upgrade legacy infrastructure, this document provides a structured framework for evaluation, selection, and implementation.

2. Understanding What a Loan Origination System Does

Before diving into selection criteria, it is essential to understand exactly what a modern Loan Origination System encompasses. Many organizations make the mistake of evaluating LOS platforms based on a narrow understanding of their function, only to discover significant gaps after deployment.

2.1 The Core Functions of a Loan Origination System

A comprehensive LOS manages the following stages of the loan lifecycle:

- Lead Capture and Application Management: Receiving loan applications across multiple channels — web portals, mobile apps, branch systems, DSAs, and aggregators — and consolidating them into a single workflow.

- Document Collection and Verification: Digitally collecting KYC documents, income proofs, bank statements, and property documents, and verifying them through integrations with government databases, bureaus, and third-party data providers.

- Credit Underwriting and Decisioning: Running automated credit models, bureau checks, bank statement analysis, and risk scoring algorithms to arrive at a credit decision — approve, reject, or refer to manual underwriting.

- Loan Structuring and Offer Generation: Configuring loan terms including amount, tenure, interest rate, fees, and repayment schedule based on the credit assessment and product rules.

- Legal and Compliance Workflows: Generating loan agreements, collecting e-signatures, recording customer consent, and maintaining audit trails required under RBI and other regulatory guidelines.

- Disbursement Integration: Triggering fund transfers through integrations with core banking systems or payment gateways, and recording disbursement details.

- Reporting and Analytics: Providing operational dashboards, underwriting performance reports, TAT (Turn Around Time) analytics, and regulatory reports.

2.2 Why a Generic Software Solution is Not Enough

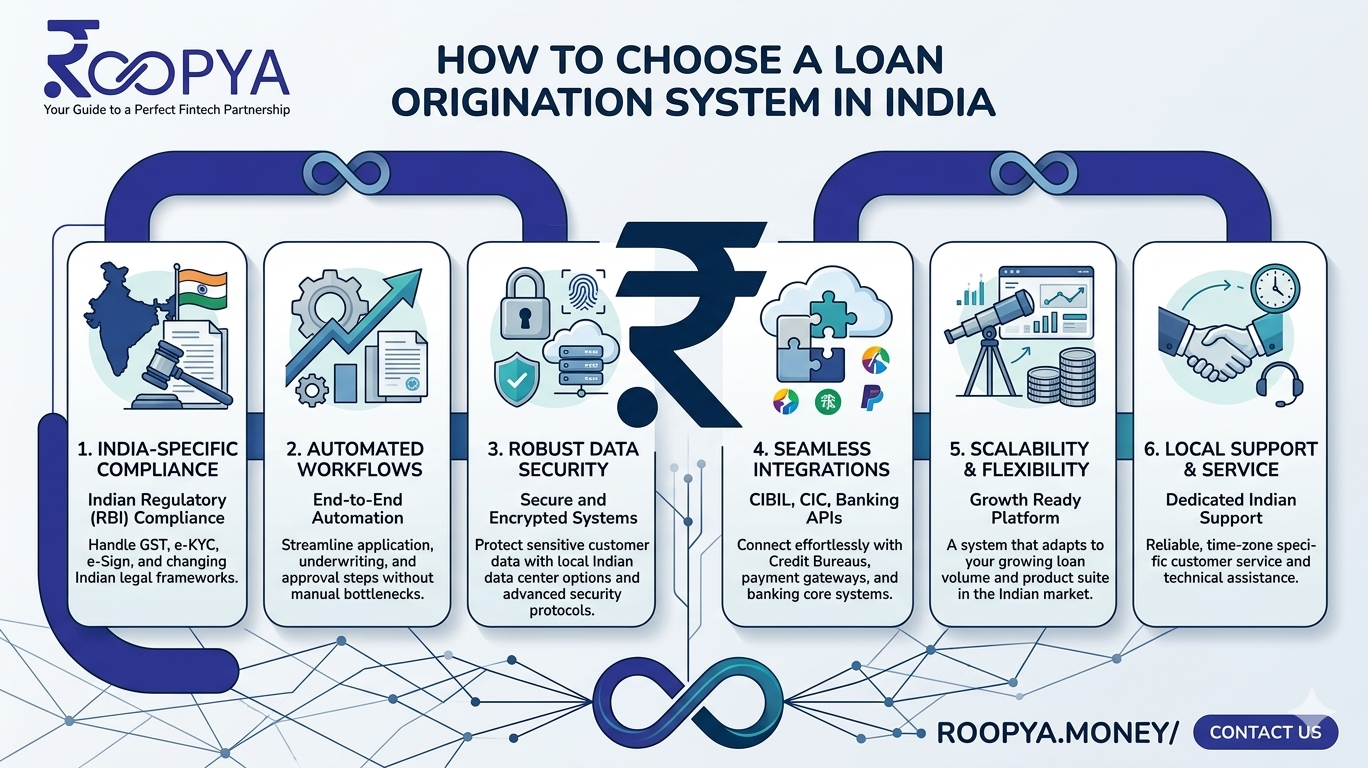

Many early-stage Fintechs attempt to build loan origination workflows on generic CRM platforms, spreadsheets, or basic workflow tools. While this may work for very small volumes, it quickly becomes untenable as the business scales. The Indian lending market has unique requirements — CKYC integration, RBI-mandated audit trails, bureau integrations with CIBIL, Experian, CRIF, and Equifax, and GST-linked income verification — that require purpose-built LOS solutions with India-specific compliance embedded from the ground up.

3. The Regulatory Context: What India’s Lending Laws Demand of Your LOS

Operating as an NBFC or Fintech lender in India means operating under a complex and evolving regulatory environment. The Reserve Bank of India (RBI) has significantly tightened its oversight of digital lending over the past few years, and your LOS must be capable of supporting compliance without manual workarounds.

3.1 Key Regulatory Requirements Your LOS Must Support

| Regulatory Requirement | LOS Capability Required |

| RBI Digital Lending Guidelines 2022 | Loan Service Provider (LSP) disclosure, Key Fact Statement (KFS) generation, borrower consent recording |

| CKYC / KYC Compliance | Integration with CKYC registry, Aadhaar-based eKYC, Video KYC (VKYC) support |

| Fair Practices Code | Transparent communication logs, standardized rejection letters, grievance redressal tracking |

| Data Localization | All borrower data stored on India-based servers |

| Credit Information Bureau Integration | Real-time CIBIL, Experian, CRIF, Equifax pulls with consent management |

| GST / ITR Verification | Integration with GSTN and ITD portals for income verification |

| E-sign and e-NACH | Support for Aadhaar-based e-sign and eNACH mandate registration |

| Audit Trail | Immutable logs of all decisions, data accesses, and changes |

Any LOS that cannot natively support these requirements — or cannot be configured to do so through APIs — should be disqualified at the outset. Regulatory compliance is not optional, and building workarounds around a non-compliant platform is a costly and risky path.

4. Key Evaluation Criteria for Choosing Your LOS

4.1 Configurability and Product Flexibility

India’s lending market is characterized by extraordinary product diversity — personal loans, MSME loans, gold loans, two-wheeler loans, agricultural loans, Buy Now Pay Later (BNPL), and more. Your LOS must be capable of supporting multiple loan products with different eligibility rules, document requirements, credit decisioning logic, and repayment structures.

Critically, you need to be able to configure new products and modify existing ones without deep software development work. Look for platforms that offer:

- No-code or low-code product configurators for loan parameters, fees, and eligibility rules.

- Visual workflow builders that allow operations teams to modify underwriting processes without developer intervention.

- Rule engine frameworks where credit policy changes can be deployed rapidly, even daily if needed.

- Multi-product support on a single platform to avoid the fragmentation of running separate systems for each loan type.

4.2 Credit Decisioning and Underwriting Capabilities

The sophistication of a platform’s underwriting engine is often what separates a good LOS from a great one. Modern LOS solutions in India have moved far beyond simple bureau score cutoffs. Evaluate the following:

- Bureau Integration Depth: Does the platform pull data from all four major bureaus (CIBIL, Experian, CRIF, Equifax) and parse the full bureau report, including trade-line level details, inquiry history, and derived attributes?

- Alternative Data Sources: Can the platform integrate with GST APIs, Account Aggregator (AA) framework, payroll platforms, e-commerce transaction data, and telecom data providers for thin-file customers?

- Bank Statement Analysis: Does the platform offer automated bank statement analysis using machine learning to extract income, obligations, spending patterns, and fraud signals?

- Custom Scorecard Support: Can your data science team deploy custom credit scorecards and update them without vendor dependency?

- Decision Explainability: For regulatory compliance and customer communication, can the platform generate human-readable explanations for credit decisions?

4.3 Integration Ecosystem and API Architecture

Your LOS does not operate in isolation. It must connect seamlessly with a wide ecosystem of data providers, banking partners, payment systems, and internal tools. Evaluate the platform’s integration capabilities rigorously:

- Pre-built Integrations: Does the vendor offer pre-built connectors for India’s major data providers — CIBIL, Experian, CRIF, Equifax, MCA, GSTN, ITD, DigiLocker, Aadhaar, and Account Aggregator?

- API-First Architecture: Is the LOS built on modern REST APIs that allow your engineering team to connect any data source or internal system?

- Core Banking Connectivity: Can the platform connect to your core banking system (CBS) or partner bank’s CBS for account opening, disbursement triggering, and repayment reconciliation?

- Payment Gateway Integration: Does it support integration with NPCI systems, NACH, eNACH, UPI AutoPay, and payment aggregators?

- Webhook Support: Can the platform send real-time event notifications to downstream systems for workflow automation?

4.4 Scalability and Performance

One of the biggest mistakes Fintech startups make is choosing a platform that works perfectly at their current volume but crumbles under scale. Before signing any contract, stress-test the vendor’s scalability claims:

- Cloud-Native Architecture: Is the platform built on a cloud-native architecture (preferably on AWS, Azure, or GCP) with microservices, containerization, and auto-scaling?

- Throughput Benchmarks: What is the platform’s tested throughput in terms of concurrent loan applications, bureau pulls per minute, and decision API response time?

- Multi-Tenancy: If you plan to operate multiple business lines or co-lending arrangements, does the platform support multi-tenancy with strict data segregation?

- Disaster Recovery: What are the vendor’s RTO (Recovery Time Objective) and RPO (Recovery Point Objective) commitments? Is there a geographically redundant deployment?

4.5 User Experience for Borrowers and Operations Teams

An LOS must serve two very different user groups — borrowers applying for loans and your internal operations team processing them. Both experiences matter:

- Borrower Journey: Does the platform support a mobile-first, low-friction application experience? Can it handle vernacular language support for tier-2 and tier-3 markets?

- Underwriter Interface: Is the credit officer’s interface intuitive, with all relevant data consolidated in a single screen? Poorly designed underwriter interfaces are a major source of processing delays and errors.

- Operations Dashboard: Can branch managers and operations leads monitor pipeline health, TAT compliance, and team productivity in real time?

- Customer Communication: Does the platform automate borrower communication — application status updates, document request reminders, offer letters, sanction letters — through SMS, email, and WhatsApp?

4.6 Security and Data Privacy

In an environment of increasing cyber threats and strict data privacy expectations, your LOS must meet the highest security standards:

- Data Encryption: Are data at rest and in transit encrypted using industry-standard protocols (AES-256, TLS 1.2+)?

- Role-Based Access Control: Can you define granular access controls so that underwriters, managers, and auditors see only the data they need?

- Personal Data Handling: Is the platform aligned with India’s Digital Personal Data Protection Act (DPDPA) 2023 requirements, including consent management and data principal rights?

- Penetration Testing: Does the vendor conduct regular third-party penetration testing and share reports?

- ISO and SOC Certifications: Is the vendor ISO 27001 certified and SOC 2 Type II compliant?

5. Build vs. Buy vs. SaaS: The Strategic Decision Framework

5.1 Building an In-House LOS

Some well-funded Fintechs choose to build a proprietary LOS. This offers maximum customization and competitive differentiation but comes with significant drawbacks for most organizations.

- Pros: Complete control over product roadmap; no vendor dependency; deep alignment with proprietary credit models.

- Cons: 12–24 months to build a production-grade system; requires a large, experienced engineering team; ongoing maintenance burden diverts resources from core business development.

Building in-house is typically justifiable only for very large players with distinctive technological requirements that no vendor can meet.

5.2 Licensed On-Premise Software

Traditional enterprise LOS vendors offer licensed software deployed on the lender’s own infrastructure. While this gives data control, it comes with high upfront costs, long implementation timelines, and the operational burden of managing infrastructure.

5.3 Cloud-Based SaaS LOS

For most NBFCs and Fintech startups in India today, a cloud-based SaaS LOS represents the optimal choice. It offers faster time-to-market (typically 8–16 weeks for deployment), predictable subscription-based costs, automatic upgrades, and the ability to scale usage as loan volumes grow. The SaaS model also aligns vendor incentives with customer success, as vendors earn more when their clients grow.

6. Navigating the Indian LOS Vendor Landscape

The Indian market for Loan Origination Systems has matured significantly, with a mix of global platforms, established Indian software vendors, and new-generation cloud-native Fintech infrastructure providers.

6.1 Categories of Vendors to Evaluate

- Global Enterprise Vendors: International players with India-adapted solutions, typically better suited for large NBFCs with complex requirements and the budget to match.

- Established Indian Software Companies: Domestic players with deep India-specific integrations, strong compliance track records, and significant deployments across Indian banks and NBFCs.

- New-Generation Cloud-Native Providers: API-first, microservices-based platforms built specifically for the Fintech era, offering rapid deployment and modern architecture. Often preferred by Fintech startups.

- Vertical-Specific Platforms: LOS solutions designed specifically for particular loan types such as MSME lending, agricultural credit, or vehicle financing.

6.2 Evaluation Red Flags

During vendor evaluation, watch for the following warning signs:

- Inability to share customer references from organizations of similar scale and loan product complexity.

- Vague answers about data localization — all India lending data must be stored on India-based servers.

- No roadmap for Account Aggregator (AA) framework integration, which is rapidly becoming essential for income verification.

- Vendors who cannot demonstrate their RBI Digital Lending Guidelines compliance in the platform with specific feature walkthroughs.

- Unusually long customization timelines for standard configurations — this suggests a rigid, non-configurable core.

7. Implementation Best Practices for NBFCs and Fintechs

7.1 Phased Implementation Approach

Rather than attempting a big-bang deployment, successful organizations adopt a phased approach:

Phase 1 (Weeks 1–8): Core origination workflow for the primary loan product, essential bureau integrations, basic underwriting rules, and disbursement connectivity.

Phase 2 (Weeks 9–16): Additional loan products, advanced scoring models, alternative data integrations, and automated customer communications.

Phase 3 (Weeks 17–24): Advanced analytics, co-lending configurations, DSA portal, and full API marketplace connectivity.

7.2 Data Migration Considerations

For organizations migrating from legacy systems, data migration is often the most underestimated challenge. Ensure the vendor has a proven data migration methodology and that your team allocates sufficient time for data cleansing, validation, and parallel running before decommissioning the old system.

7.3 Change Management

Technology is only one part of a successful LOS implementation. Equally important is ensuring your credit, operations, and sales teams embrace the new system. Invest in comprehensive training, designate internal champions for each department, and plan for a managed transition period where old and new processes run in parallel.

8. Understanding Total Cost of Ownership

When evaluating LOS platforms, many organizations focus on the headline subscription or license fee and underestimate the true total cost of ownership (TCO). A complete TCO analysis must include:

- Platform subscription or license fees (typically per-user, per-application, or transaction-based pricing).

- Implementation and integration services — often 30–50% of the first-year platform cost.

- Data provider costs — bureau pulls, GST verification, and Account Aggregator calls are typically billed separately.

- Internal engineering time for integration, configuration, and ongoing maintenance.

- Training and change management costs.

- Infrastructure costs if not fully SaaS.

When comparing vendors, always request a five-year TCO projection that includes all of the above components, not just the platform fee.

9. Structuring Your RFP and Vendor Selection Process

A structured Request for Proposal (RFP) process protects your organization from making an emotionally driven or inadequately researched decision. Recommended process:

- Step 1 — Internal Requirements Workshop (2 weeks): Gather requirements from credit, operations, technology, compliance, and business development teams. Document must-have, should-have, and nice-to-have features.

- Step 2 — Longlist (1 week): Identify 8–10 vendors based on market research, analyst reports, peer recommendations, and industry events.

- Step 3 — RFP Distribution (2 weeks): Send a detailed RFP to longlisted vendors. Include functional requirements, technical architecture requirements, security requirements, and a request for pricing.

- Step 4 — Shortlisting (1 week): Evaluate RFP responses and shortlist 3–4 vendors for detailed demonstrations.

- Step 5 — Product Demonstrations (2–3 weeks): Request scenario-based demonstrations using your actual loan products and workflows — not generic sales demos.

- Step 6 — Reference Checks: Speak to at least three existing customers of similar size and complexity for each shortlisted vendor.

- Step 7 — Proof of Concept (optional): For complex or large deployments, consider a paid 4–6 week proof of concept with 1–2 finalists.

- Step 8 — Commercial Negotiation and Contracting: Negotiate pricing, SLAs, data ownership, exit provisions, and upgrade roadmap commitments.

10. Conclusion: Your LOS as a Strategic Asset

A Loan Origination System is not merely an operational tool — it is a strategic asset that will define the speed, quality, and scalability of your lending business for years to come. In India’s intensely competitive and rapidly evolving lending market, organizations that make a thoughtful, well-informed LOS decision gain a compounding advantage: faster decisions, better risk management, lower costs, and superior borrower experiences.

The right LOS for your organization depends on the unique combination of your loan products, target customer segments, regulatory obligations, technology philosophy, and growth ambitions. There is no universal answer, but there is a rigorous process for finding your answer — and this guide has laid out that process.

Invest the time upfront in requirements gathering, vendor evaluation, and reference checks. The cost of making the right decision today is a fraction of the cost of migrating away from the wrong platform eighteen months from now. In the digital lending era, your technology choices are your competitive choices. Choose wisely.