Loan Origination System (LOS) & Business Rule Engine (BRE) The Future of Intelligent Digital Lending

In today’s rapidly evolving lending landscape, financial institutions, NBFCs, fintech companies, banks, and digital lenders are under immense pressure to deliver faster loan approvals while maintaining strong risk controls. Customers expect instant decisions, seamless onboarding, and a completely digital borrowing experience. At the same time, lenders must ensure compliance, reduce operational costs, and improve portfolio quality.

This is where a modern Loan Origination System (LOS) combined with a powerful Business Rule Engine (BRE) becomes a game-changer.

For CTOs, Heads of Product, and Chief Credit Officers, investing in a scalable lending technology platform is no longer optional. It has become a strategic necessity for staying competitive in the digital lending ecosystem.

Start Free Trial

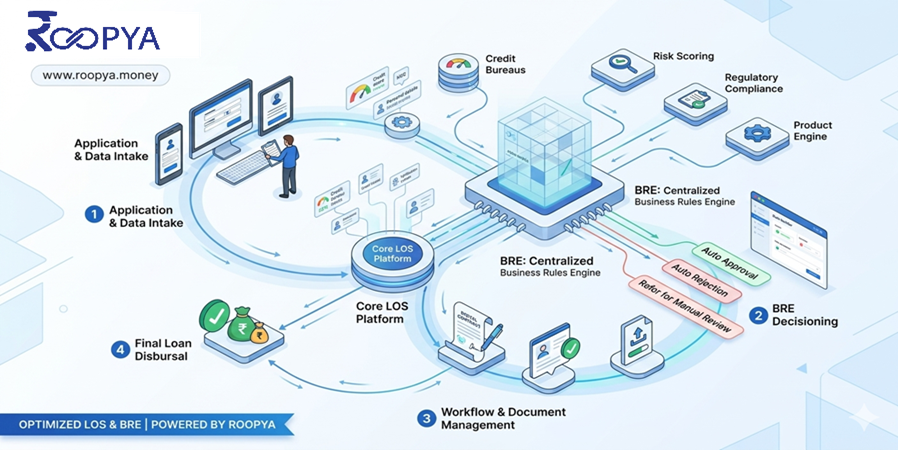

Roopya’s Loan Origination System (LOS) and customizable Business Rule Engine (BRE) empower lenders to automate customer onboarding, document verification, credit assessment, underwriting, risk evaluation, and loan approvals through a unified digital platform.

What is a Loan Origination System (LOS)?

A Loan Origination System is a technology platform that manages the complete lifecycle of a loan application from borrower onboarding to loan disbursement.

A modern LOS helps lenders automate:

- Customer onboarding

- KYC verification

- Document collection

- Credit bureau checks

- Bank statement analysis

- Income verification

- Risk assessment

- Underwriting decisions

- Loan approval workflows

- Loan disbursement

Instead of relying on spreadsheets, emails, and manual operations, lenders can process thousands of applications through a centralized workflow engine.

Why Modern Lenders Need a Business Rule Engine (BRE)

A Business Rule Engine acts as the intelligence layer of a lending platform.

The BRE automatically evaluates borrower eligibility using predefined credit policies and lending rules.

For example:

- Minimum credit score requirements

- Income thresholds

- Debt-to-income ratio limits

- Industry restrictions

- Geographic restrictions

- Employment verification criteria

- Bank statement conditions

Using a customizable business rule engine BRE for digital lending, lenders can automate decision-making without requiring engineering teams to rewrite code every time credit policies change.

This flexibility enables organizations to respond quickly to changing market conditions and regulatory requirements.

The Rise of No-Code Loan Origination Systems

Traditional lending platforms often require extensive software development whenever new products or underwriting rules are introduced.

A no code loan origination system with multi bureau integration eliminates these challenges.

Business users can:

- Configure workflows

- Modify underwriting rules

- Launch new loan products

- Create approval matrices

- Define risk policies

without writing a single line of code.

Benefits include:

Faster Product Launches

New lending products can be deployed in days instead of months.

Reduced IT Dependency

Credit teams gain control over lending policies.

Improved Agility

Organizations can adapt quickly to changing borrower behavior.

Lower Operational Costs

Automation reduces manual processing efforts.

Automated Financial Document Analyzer Using OCR for Loan Onboarding

Document verification remains one of the biggest bottlenecks in lending operations.

Borrowers typically submit:

- Bank statements

- Income documents

- GST filings

- Financial statements

- Tax returns

- Business registrations

Manual verification consumes significant time and introduces human error.

An automated financial document analyzer using OCR for loan onboarding solves this problem.

How OCR Technology Works

OCR (Optical Character Recognition) extracts information from uploaded documents and converts it into structured digital data.

The system automatically captures:

- Customer information

- Financial metrics

- Transaction details

- Income data

- Business performance indicators

This data becomes immediately available for underwriting and risk assessment.

Key Benefits

Faster Processing

Loan applications can be processed within minutes.

Improved Accuracy

Automated extraction reduces manual errors.

Better Customer Experience

Borrowers upload documents once without repeated requests.

Increased Scalability

Lenders can process higher application volumes.

Instant Bank Statement Analyzer Tool for Credit Underwriting

Bank statements contain valuable insights into borrower behavior.

However, manual analysis is time-consuming and inconsistent.

An instant bank statement analyzer tool for credit underwriting automates this process.

The platform evaluates:

- Monthly cash flow

- Income consistency

- Expense patterns

- Average balances

- Existing loan obligations

- EMI commitments

- Bounce history

- Financial stability

Key Underwriting Advantages

Faster Credit Decisions

Applications move quickly through underwriting.

Reduced Risk

Potential red flags are identified early.

Improved Portfolio Quality

Data-driven decisions improve loan performance.

Better Fraud Detection

Unusual transaction patterns are flagged automatically.

Multi-Bureau Integration for Comprehensive Risk Assessment

Credit bureau data remains critical for lending decisions.

A no code loan origination system with multi bureau integration enables lenders to access multiple credit bureaus through a single platform.

Benefits include:

- Better borrower visibility

- Comprehensive risk evaluation

- Faster credit checks

- Improved approval accuracy

- Reduced operational complexity

Lenders can combine bureau insights with bank statement analysis, OCR data, and internal scoring models for superior decision-making.

End-to-End Digital Onboarding Platform for MSME Lending

MSME lending presents unique challenges due to limited financial documentation and varying business profiles.

An end to end digital onboarding platform for MSME lending addresses these challenges through automated workflows.

The platform integrates:

Digital KYC

Instant identity verification.

GST Analysis

Business turnover evaluation.

Banking Data

Cash flow assessment.

Credit Bureau Checks

Creditworthiness evaluation.

OCR-Based Document Processing

Automated document extraction.

Automated Underwriting

Instant eligibility assessment.

This enables lenders to serve MSMEs faster while maintaining strong risk controls.

Key Features of Roopya’s LOS & BRE Platform

Workflow Automation

Automate every stage of loan origination.

Rule-Based Decisioning

Configure lending policies without coding.

API Integrations

Connect with bureaus, banks, KYC providers, and third-party systems.

OCR-Powered Document Processing

Automate document verification and extraction.

Bank Statement Analytics

Generate instant underwriting insights.

Fraud Detection

Identify suspicious applications early.

Risk Scoring

Create customized risk models.

Real-Time Dashboards

Track operational and portfolio performance.

Benefits for CTOs

For CTOs, the primary focus is scalability, security, and system performance.

Roopya’s platform provides:

- API-first architecture

- Cloud scalability

- Enterprise-grade security

- Easy integration capabilities

- Configurable workflows

- Reduced technical debt

Benefits for Heads of Product

Product leaders can launch lending products faster.

Advantages include:

- No-code configuration

- Rapid experimentation

- Faster go-to-market

- Better customer experiences

- Continuous optimization

Benefits for Chief Credit Officers

Credit leaders gain:

- Consistent underwriting

- Improved risk management

- Automated policy enforcement

- Better portfolio quality

- Reduced NPAs

- Enhanced compliance

The Future of Digital Lending

The future belongs to lenders that can combine automation, intelligence, and customer-centric experiences.

A Loan Origination System integrated with a powerful Business Rule Engine creates a scalable foundation for growth.

By leveraging:

- Automated financial document analyzer using OCR for loan onboarding

- Instant bank statement analyzer tool for credit underwriting

- No code loan origination system with multi bureau integration

- End to end digital onboarding platform for MSME lending

- Customizable business rule engine BRE for digital lending

financial institutions can accelerate loan approvals, reduce operational costs, improve portfolio performance, and deliver superior customer experiences.

For lenders looking to scale efficiently while maintaining strong credit controls, Roopya’s LOS and BRE platform offers the technology foundation needed to succeed in the next generation of digital lending.