Loan Origination Software Automation Platform: The Smart Way to Lend Faster, Safer, and at Scale

The lending landscape in India is undergoing a fundamental shift. The days of paper-heavy, branch-dependent loan processing are giving way to fully digital, automated journeys that serve borrowers in minutes — not weeks. At the heart of this transformation is a Loan Origination Software Automation Platform: a technology layer that replaces slow, manual lending workflows with intelligent, rules-driven, and real-time decision-making systems.

Roopya is India’s first fully automated, no-code Loan Origination Software Platform — purpose-built for modern lenders including NBFCs, banks, microfinance institutions (MFIs), and fintech companies. Whether you’re originating personal loans, business loans, or small-ticket credit, Roopya gives you the infrastructure to launch, scale, and comply — all without writing a single line of code.

Start Free Trial

What Is a Loan Origination Software Automation Platform?

A Loan Origination Software Automation Platform (often called a LOS — Loan Origination System) is a cloud-based software solution that digitizes and automates every step of the loan lifecycle — from the moment a borrower applies for credit to the point the loan is approved, sanctioned, and disbursed.

Traditional loan origination involved multiple disconnected steps: manual form collection, physical document verification, telephonic credit checks, in-person underwriting reviews, and branch-level approvals. Each of these steps consumed time, introduced human error, and increased the cost per loan originated.

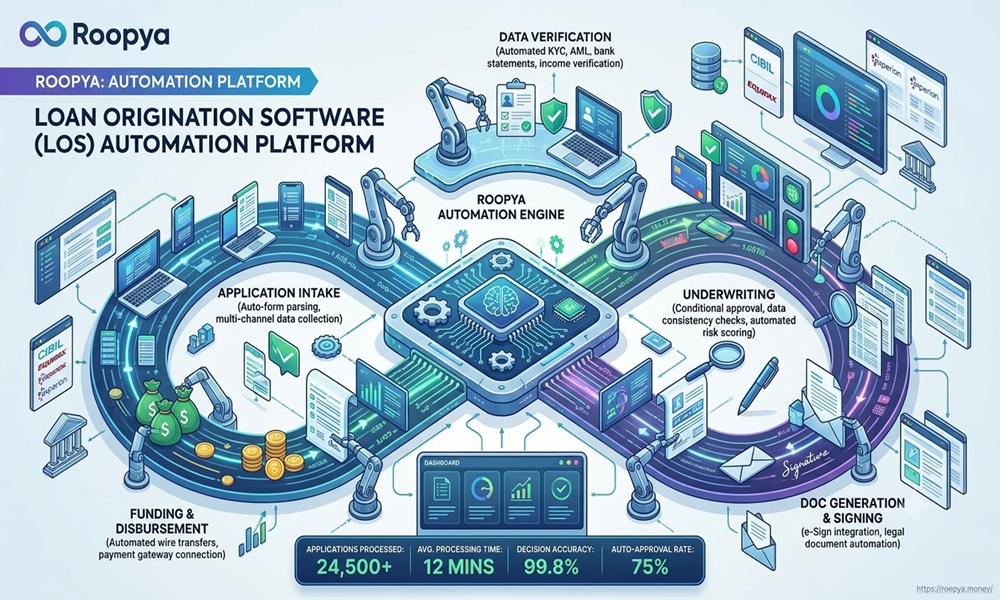

An automated platform collapses these steps into a seamless digital pipeline:

- A borrower submits their application digitally

- Identity is verified instantly via eKYC and Aadhaar-based authentication

- Bank statements, income proofs, and financial data are fetched and analyzed automatically

- Credit bureau data is pulled in real time from CIBIL, Experian, CRIF, or Equifax

- A scorecard and Business Rule Engine (BRE) assess creditworthiness instantly

- A loan decision — approved, referred, or declined — is generated in seconds

- Upon approval, the loan agreement is e-signed and disbursement is triggered

This is what Roopya delivers: a unified, end-to-end loan origination automation platform that powers your lending operations from day one — with zero upfront cost and a go-live timeline of just one day.

The Core Loan Origination Process — Automated

Roopya’s platform automates every stage of the loan origination process. Here’s how each phase transforms under automation:

1. Digital Loan Application

The borrower journey begins with a fully digital application form — accessible via web, mobile app, or embedded within a partner’s platform. Roopya supports 20+ pre-configured loan product templates (personal loans, business loans, payday loans, gold loans, home loans, vehicle loans, and more), each with customizable fields that can be configured without coding by your business team.

Borrowers complete their application in minutes. Dynamic form logic ensures they only see fields relevant to their profile, reducing drop-off and improving data quality from the start.

2. Automated KYC and Identity Verification

Upon submission, Roopya triggers automated KYC workflows. This includes:

- Aadhaar-based eKYC for instant identity verification

- PAN verification via government database APIs

- Facial recognition and liveness detection for biometric confirmation

- Video KYC for higher-value loan products where in-person verification is mandated

- Digilocker integration to fetch government-issued documents automatically

All of this happens in real time, without a human agent reviewing a single document manually. Roopya’s AI-powered OCR and NLP engines extract and verify information with 99%+ accuracy, flagging anomalies or fraud signals instantly.

3. Document Management and Automated Analysis

Once identity is confirmed, Roopya’s document management engine takes over. Borrowers upload supporting documents — bank statements, salary slips, ITR filings, GST returns, property papers — which are stored in a secure, centralized document vault.

Roopya’s AI then analyzes these documents automatically:

- Bank statement analyzers extract income patterns, EMI obligations, and cash flow health

- Income documents are cross-verified against bureau data and application inputs

- Fraudulent or tampered documents are flagged using AI-based anomaly detection

The result is a complete, verified financial picture of the borrower — assembled in seconds, not days.

4. Multi-Bureau Credit Pull and Assessment

Roopya is pre-integrated with India’s leading credit bureaus — CIBIL, Experian, CRIF Highmark, and Equifax. The platform pulls credit reports automatically upon application submission or at a configurable trigger point in the workflow.

The credit data is structured and fed into:

- Credit scoring models (including custom application scorecards built on Roopya’s analytics platform)

- Delinquency history analysis

- Debt-to-income ratio computation

- Credit utilization assessment

- Negative list checks (fraud blacklists, defaulter lists, PEP databases)

All of this happens through pre-integrated API calls — no manual credit officer review required for standard applications.

5. No-Code Business Rule Engine (BRE) for Automated Decisioning

At the core of Roopya’s loan origination automation platform is a powerful, self-configurable Business Rule Engine (BRE). This is where your credit policy lives — and it’s 100% configurable by your business team through an intuitive visual interface.

Your credit team can define:

- Eligibility rules (minimum income, minimum credit score, employment type, geography)

- Rejection triggers (high DPD history, written-off accounts, excessive inquiries)

- Loan amount and tenor calculation logic

- Interest rate assignment rules based on risk tier

- Waiver and exception workflows for referred cases

- Conditional logic for different loan products or borrower segments

The BRE evaluates each application against your configured rules and generates a real-time decision: Auto-Approve, Auto-Decline, or Refer to Underwriter. This dramatically reduces the manual underwriting burden while maintaining your credit policy discipline.

6. Automated Underwriting and Risk Assessment

For applications that require human review, Roopya’s platform routes them to your underwriting team with a fully assembled credit package: verified documents, bureau data, income analysis, scorecard output, and BRE recommendation — all in one screen.

Underwriters are not starting from scratch. They are reviewing a pre-analyzed, pre-verified application and making a final judgment call — which typically takes minutes, not hours.

For lenders using Roopya’s AI-powered credit decisioning module, even the underwriting step can be partially or fully automated using machine learning models that analyze thousands of data points — including alternative data signals — to produce accurate, explainable credit decisions.

7. Loan Sanctioning, Agreement Generation, and E-Sign

Once a loan is approved, Roopya automatically generates the loan sanction letter and loan agreement using pre-built templates that can be customized to your institution’s branding and legal requirements.

The borrower receives the agreement digitally and completes the e-signing process — fully compliant with India’s IT Act — without visiting a branch. Execution of agreements typically takes under two minutes.

8. Disbursement Triggering

Upon e-sign completion, Roopya’s platform triggers disbursement through pre-integrated payment gateways and banking APIs. This can be done via IMPS, NEFT, UPI, or direct bank transfer — depending on your disbursement preferences and the borrower’s bank details.

The entire journey — from application submission to disbursement trigger — can be completed in under 10 minutes for a fully automated, rule-compliant application.

Why NBFCs and Banks Choose Roopya’s Loan Origination Automation Platform

1-Day Go-Live

Roopya’s plug-and-play infrastructure means you don’t need months of IT implementation. Most lenders go live within a single day — with pre-configured loan products, pre-integrated APIs, and ready-to-use workflows that can be activated and customized immediately.

Zero Upfront Cost — Pay As You Use

Unlike traditional loan origination software that demands large licensing fees and infrastructure investments, Roopya operates on a flexible, usage-based pricing model. You pay only for what you process — making it the ideal choice for growing NBFCs that want to scale without financial risk.

300+ Pre-Integrated APIs

Building API integrations from scratch can take months and cost crores. Roopya comes with 300+ pre-integrated APIs covering:

- Credit bureaus (CIBIL, Experian, CRIF, Equifax)

- KYC services (Aadhaar, PAN, eKYC providers)

- Bank statement analyzers (Perfios, Karza, Finbox, etc.)

- NACH and payment gateways (Razorpay, Cashfree, PayU)

- eSign and video KYC providers

- GST and ITR verification services

- Fraud detection and negative list databases

All integrations are pre-built, pre-tested, and configurable — ready to activate from your dashboard.

Truly No-Code Platform

Business users — not just developers — can configure loan products, define credit rules, design workflows, and set up notification templates. There is no dependency on a technical team for routine changes to your origination process. This gives lenders unprecedented agility to respond to market changes and competitive pressures.

Advanced Fraud Detection

Roopya’s built-in AI fraud detection modules protect your origination pipeline from:

- Identity fraud and synthetic identity creation

- Document tampering and forgery

- Device fingerprinting anomalies

- Velocity-based fraud patterns (multiple applications from same device or address)

- PEP and watchlist matching

Fraud signals are flagged in real time and integrated into the BRE decision logic — ensuring fraudulent applications never reach your approval queue.

Regulatory Compliance Built-In

Roopya’s platform is continuously updated to remain compliant with the latest RBI guidelines, IRDAI requirements, and data protection norms (including India’s DPDP Act). From mandatory KYC standards to fair practice codes and disclosure requirements, compliance is embedded into your origination workflows — not bolted on as an afterthought.

Multi-Product and Multi-Segment Support

Roopya supports 20+ loan products out of the box. Whether you’re originating:

- Personal loans and salary advances

- Business loans and SME credit

- Gold loans and asset-backed lending

- Home loans and mortgage products

- Vehicle and auto loans

- Microfinance and group lending products

…the platform adapts to your product structure, borrower journey, and underwriting logic.

LSP and DSA Channel Management

Beyond direct borrower journeys, Roopya supports Loan Service Provider (LSP) and Direct Selling Agent (DSA) onboarding and management — enabling lenders to run multi-channel origination with full visibility into channel partner performance, source-of-business tracking, and agent-level incentive management.

Who Should Use Roopya’s Loan Origination Automation Platform?

Roopya is designed for any institution that originates loans and wants to do it faster, cheaper, and at scale. The platform is particularly suited for:

NBFCs (Non-Banking Financial Companies): Whether you’re a recently registered NBFC or an established one looking to modernize, Roopya gives you enterprise-grade origination infrastructure without enterprise-grade complexity or cost.

Banks and SFBs: Scheduled commercial banks and small finance banks can deploy Roopya’s automation layer to accelerate retail and SME loan processing, reduce turnaround time, and improve credit officer productivity.

Microfinance Institutions (MFIs): Roopya’s group lending and small-ticket loan configurations make it ideal for MFIs originating high volumes of small loans across rural and semi-urban geographies.

Fintech Lenders and Digital NBFCs: For tech-first lenders, Roopya’s open API architecture enables deep integration with existing mobile apps, marketplaces, and digital ecosystems — powering fully embedded lending journeys.

Co-Lending Partners: For institutions operating co-lending models with banks, Roopya provides the origination, data-sharing, and compliance infrastructure needed to manage joint origination workflows efficiently.

Roopya vs. Traditional Loan Origination: The Numbers Tell the Story

| Parameter | Traditional LOS | Roopya Automation Platform |

|---|---|---|

| Go-Live Time | 3–6 months | 1 Day |

| Upfront Cost | ₹20–50 Lakhs+ | Zero |

| Integration Effort | High (months) | 300+ APIs pre-integrated |

| Loan Processing Speed | 3–7 days | Under 10 minutes |

| Manual Touchpoints | 15–20 per application | 0–2 (exceptions only) |

| Fraud Detection | Manual review | AI-powered, real-time |

| Compliance Updates | Manual patch cycle | Continuous, automatic |

| Coding Required | Yes | Zero |

| Scalability | Limited by infra | Unlimited, cloud-native |

The Roopya Advantage: AI-Powered Origination at Scale

Roopya doesn’t just automate what humans used to do manually — it makes the origination process smarter through embedded artificial intelligence.

AI Document Analysis extracts and verifies data from documents with 99%+ accuracy in seconds. Whether it’s a handwritten loan application, a scanned bank statement, or an ITR PDF, Roopya’s intelligent OCR and NLP systems process it instantly.

Machine Learning Credit Scoring goes beyond bureau scores. Roopya’s ML models evaluate alternative data — digital footprints, spending behavior, cash flow patterns — to provide more accurate, inclusive credit assessments. This is particularly powerful for thin-file borrowers who may not have a strong traditional credit history.

Self-Learning Business Rules enable Roopya’s BRE to identify patterns in approval and rejection outcomes, suggesting rule optimizations that improve both portfolio quality and approval rates over time.

AI-Driven Fraud Detection catches fraud patterns that manual review would miss — synthesizing signals across thousands of concurrent applications in real time.

The result is a loan origination process that is not just faster and cheaper — but genuinely smarter.

Integrating Roopya Into Your Existing Ecosystem

Roopya’s open API architecture makes integration with your existing systems straightforward. Whether you run a core banking solution, an ERP, a CRM, or a collections platform, Roopya connects seamlessly:

- CRM Integration: Sync borrower application data with Salesforce, Zoho, or your proprietary CRM

- Core Banking Connectivity: Push disbursement and repayment data to your CBS in real time

- Collections Handoff: Automatically transfer matured loan accounts to Roopya’s LMS and collections engine

- Reporting and BI Tools: Export portfolio data to your analytics stack via API or scheduled reports

- Marketplace and Embedded Finance: Deploy Roopya’s loan origination APIs within your app, website, or partner marketplace for fully embedded lending

Getting Started with Roopya in 3 Steps

Step 1 — Schedule a Demo Connect with Roopya’s lending experts to understand how the platform maps to your specific loan products, borrower segments, and operational requirements.

Step 2 — Configure and Go Live Your business team configures loan products, credit rules, and workflows through Roopya’s intuitive no-code dashboard. With 300+ APIs pre-integrated, you activate only what you need. Go live in 1 day.

Step 3 — Scale With Confidence As your loan volumes grow, Roopya scales with you — no infrastructure upgrades, no additional licensing fees. Pay only for what you process, and let Roopya’s continuously updated platform handle compliance, fraud, and performance at scale.