AI in Loan Origination Process: How Roopya is Redefining Digital Lending in India

The Indian lending landscape is undergoing a fundamental transformation. For decades, loan origination was a manual, paper-heavy, time-consuming process that frustrated borrowers and burdened lenders alike. A typical loan application involved mountains of paperwork, days of waiting, and multiple rounds of manual verification — all of which led to high operational costs, slow disbursals, and significant fraud exposure.

Today, Artificial Intelligence (AI) is rewriting that story. From the moment a borrower submits an application to the final approval decision, AI is embedded at every stage of the loan origination process — making it faster, smarter, and more accurate than ever before. At Roopya, we have built India’s most advanced AI-powered Loan Origination System (LOS) specifically for NBFCs, banks, microfinance institutions, and modern lending businesses.

Ready to experience AI-powered loan origination? Request a demo at roopya.money and see what next-generation lending looks like.

Start Free Trial

This guide breaks down exactly how AI is changing the loan origination process, what it means for your business, and how platforms like Roopya are enabling lenders to go live in just one day with full AI infrastructure already in place.

What Is Loan Origination?

Loan origination refers to the end-to-end process a borrower undergoes from the initial loan application to the final disbursement of funds. It is the front door of any lending business, and it sets the tone for the entire loan lifecycle.

The traditional loan origination process typically involves the following stages:

- Application submission (paper forms or basic online forms)

- Document collection and manual verification

- Credit bureau checks and background verification

- Manual underwriting and credit decisioning

- Loan approval, rejection, or counteroffer

- Agreement signing and disbursement

Each of these steps, when done manually, can take anywhere from three to fifteen days and requires significant human resources. Errors, fraud, and biases are also common. AI fundamentally restructures this pipeline.

Why AI is Essential in the Loan Origination Process

Traditional loan origination processes were not built for the pace, scale, or complexity of modern lending. With millions of new-to-credit borrowers entering the formal financial system in India, lenders need tools that can assess risk quickly, accurately, and without bias — across massive volumes.

Here is why AI has become not just useful but essential:

- Speed: AI can evaluate a loan application in seconds, not days.

- Accuracy: Machine learning models analyse thousands of variables, far exceeding human capability.

- Scalability: AI handles 10,000 applications as easily as it handles 10.

- Fraud Detection: AI identifies suspicious patterns that humans routinely miss.

- Consistency: Every application is evaluated against the same rules, eliminating human bias.

- Cost Reduction: Automation drastically reduces the manpower required in credit operations.

For NBFCs and modern lenders in India, AI is the difference between being competitive and being obsolete.

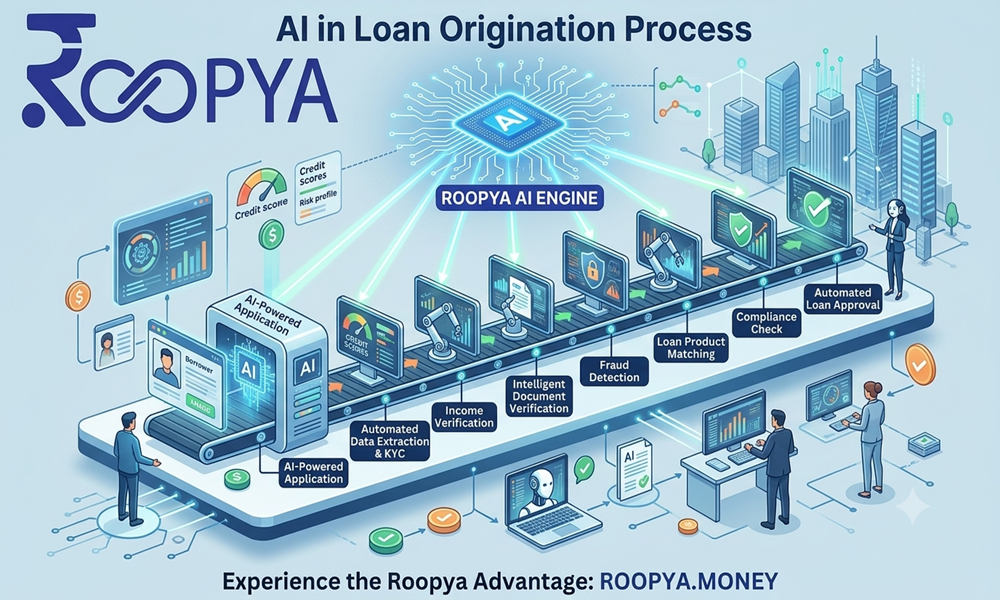

How AI Transforms Each Stage of the Loan Origination Process

1. AI-Powered Digital Application & Lead Capture

The first touchpoint in any loan journey is the application itself. AI enhances this stage through intelligent, dynamic digital forms that adapt based on the borrower’s profile. Instead of presenting every borrower with the same form, an AI-driven interface can pre-fill known data, ask relevant follow-up questions, and guide applicants to ensure completeness.

Roopya’s platform supports 20+ pre-configured loan products with automated customer loan journeys that are designed for zero friction. Borrowers can complete applications on mobile in minutes, and the system immediately flags incomplete or inconsistent data for review.

2. Automated Document Verification & KYC

One of the most time-consuming stages in traditional loan origination is document collection and verification. AI changes this dramatically through Optical Character Recognition (OCR) and Natural Language Processing (NLP).

Roopya’s AI document analysis module automatically extracts, validates, and cross-checks data from identity documents, bank statements, salary slips, GST filings, ITRs, and more — with 99%+ accuracy. Verification that previously took 2 to 3 days now happens in seconds. The system also flags potential document fraud through anomaly detection, protecting lenders from first-party and third-party fraud.

- Aadhaar & PAN verification via UIDAI and NSDL APIs

- Bank statement analysis using AI-powered PDF parsing

- GST and ITR data extraction for business loan applicants

- Liveness detection and facial recognition for identity confirmation

- Forgery and tampering detection using image analysis algorithms

3. AI-Enhanced Credit Scoring & Bureau Integration

Traditional credit scoring relies heavily on bureau scores such as CIBIL, Experian, CRIF, and Equifax. While these remain important, they tell an incomplete story — especially for new-to-credit (NTC) borrowers who lack formal credit histories. This is a massive challenge in India, where over 400 million adults are underbanked or credit-invisible.

AI-powered credit scoring models go far beyond bureau data. Roopya’s intelligent credit decisioning engine analyses alternative data sources to build a comprehensive borrower risk profile. These include:

- Bank transaction patterns and cash flow behaviour

- Mobile usage data (with consent) including app usage, recharge frequency

- Social and psychographic indicators

- GST filing consistency and business turnover trends

- Employment and employer quality scores

- Repayment behaviour on utility bills and digital payments

The result is a credit decision that is more accurate, more inclusive, and less prone to error than any traditional scoring model. Roopya’s ML-powered credit scoring delivers 40% better accuracy compared to conventional bureau-only approaches.

4. No-Code Business Rule Engine (BRE) Powered by AI

Every lender has unique credit policies — maximum loan-to-income ratios, sector exclusions, age limits, minimum FOIR requirements, and more. Traditionally, implementing these rules required extensive IT development cycles. With AI-enhanced Business Rule Engines, lenders can configure, test, and deploy complex lending rules in hours, not months.

Roopya’s intelligent BRE goes further. Our machine learning models continuously analyse historical approval and rejection data to suggest rule improvements, identify underperforming segments, and optimise credit policies automatically — while always keeping a human in the loop for final oversight.

This self-learning BRE means your credit policies get smarter with every application processed.

5. Instant Credit Decisioning & Automated Approval Workflows

This is where AI delivers its most visible impact. Once an application has been scored and all verifications are complete, the AI decisioning engine evaluates the application against all configured rules and risk models — producing a decision in milliseconds.

Roopya’s platform supports three types of decisions:

- Straight-Through Processing (STP): Fully automated approval for low-risk borrowers who meet all criteria.

- Conditional Approval: System approves with specific conditions such as a co-applicant, reduced loan amount, or additional document submission.

- Manual Review Queue: High-risk or edge-case applications are flagged and routed to underwriters with a detailed AI-generated risk summary.

This tiered approach allows lenders to automate 60 to 80% of decisions while ensuring human oversight for complex cases.

6. AI-Driven Fraud Detection & Risk Management

Loan fraud is one of the most significant challenges facing Indian lenders. From identity fraud and income manipulation to organised fraud rings, the threats are increasingly sophisticated. AI is uniquely positioned to combat this.

Roopya’s built-in fraud detection modules use ensemble machine learning models trained on millions of data points to identify suspicious patterns in real time. Key capabilities include:

- Device fingerprinting to identify multiple applications from the same device

- IP geolocation anomaly detection

- Network analysis to detect fraud rings and related-party fraud

- Velocity checks on PAN, Aadhaar, and mobile numbers

- Behavioural biometrics analysis during the application journey

Our AI fraud detection reduces fraud exposure by up to 80%, saving lenders crores in potential losses every year.

7. Loan Pricing Automation Using AI

AI is also reshaping how lenders price loans. Instead of applying uniform interest rates across borrower segments, AI-driven loan pricing models enable risk-based pricing — where each borrower receives an interest rate that accurately reflects their individual risk profile.

Roopya’s Loan Pricing Analytics module analyses portfolio data, risk scores, cost of funds, and competitive benchmarks to recommend optimal pricing for every loan. This maximises profitability while keeping interest rates competitive enough to win business.

The Business Impact of AI in Loan Origination

The numbers speak for themselves. Lenders who implement AI-powered loan origination systems see transformational improvements across key performance indicators:

| Metric | Improvement with AI (Roopya) |

| Loan Processing Time | 10x faster — hours to seconds |

| Credit Scoring Accuracy | 40% better than bureau-only models |

| Fraud Reduction | Up to 80% fewer fraud cases |

| Manual Review Volume | 60–80% reduction in manual underwriting |

| Customer Drop-off Rate | Significantly lower with streamlined digital journeys |

| Collections Recovery Rate | 60% improvement with AI-driven collection strategies |

| Go-Live Time | 1 day with Roopya’s pre-integrated platform |

Why Roopya is the Right AI-Powered LOS for Indian Lenders

Roopya is India’s most comprehensive digital lending platform — a truly no-code, unified lending infrastructure built from the ground up for NBFCs, banks, MFIs, and modern lending businesses. Our AI is not a bolt-on feature. It is the foundation of everything we build.

Here is what makes Roopya the preferred AI lending partner for modern Indian lenders:

- 1-Day Go Live: Our plug-and-play infrastructure means you start processing loans on day one.

- 300+ Pre-Integrated APIs: Credit bureaus, eKYC, payment gateways, accounting tools — all connected.

- 20+ Pre-Configured Loan Products: Personal, business, gold, home, auto, payday, and more.

- No-Code Configuration: Business users configure rules and workflows without writing a single line of code.

- Pay-As-You-Use Pricing: Zero upfront cost. Scale freely without financial risk.

- Always Compliant: Platform is continuously updated for RBI and regulatory compliance.

- AI That Learns: Every transaction makes our models smarter, benefiting your entire portfolio.

Whether you are an established NBFC looking to modernise, or a new lending startup going digital from day one, Roopya gives you the AI infrastructure that previously only the largest banks could afford.

The Future of AI in Loan Origination

The role of AI in loan origination will only deepen over the coming years. Here are the trends that will define the next generation of lending:

Conversational AI and Chatbots

AI-powered conversational agents will guide borrowers through the entire application process via WhatsApp, mobile apps, or web chat. Roopya’s conversational AI already handles borrower interactions with 95% contextual accuracy.

Embedded Finance and Co-Lending

AI will power seamless embedded lending journeys inside e-commerce platforms, ERP systems, and fintech apps. Roopya’s Embedded Finance module enables lenders to plug loan products directly into partner platforms.

Hyper-Personalised Loan Products

Rather than one-size-fits-all products, AI will enable lenders to offer dynamically priced and structured loans unique to each borrower — based on real-time risk assessment, purpose of loan, and repayment capacity.

Regulatory AI and Explainability

As regulators demand greater transparency, AI models will need to explain their decisions clearly. Explainable AI (XAI) frameworks will become standard in credit decisioning, ensuring lenders can justify every approval and rejection.

AI is no longer a technology of the future in loan origination — it is the operating standard of today. For Indian lenders competing in an increasingly digital, data-driven market, building AI capabilities into the loan origination process is no longer optional. It is the only way to stay competitive, manage risk effectively, and serve a new generation of borrowers at scale.

Roopya was built to give every lender — from an emerging NBFC to a large bank — access to enterprise-grade AI lending infrastructure at a fraction of the traditional cost. With a one-day setup, zero upfront cost, and 300+ pre-integrated APIs, we make going digital simple, fast, and profitable.