NBFC Software for Loan Origination: The Complete Guide to Automating Your Lending Operations

The Indian NBFC (Non-Banking Financial Company) sector is undergoing one of the most significant digital transformations in its history. With over 10,000 registered NBFCs operating across the country and the RBI tightening compliance norms, the pressure to modernise lending operations has never been greater. At the heart of this transformation is a single critical technology: NBFC software for loan origination.

Whether you are a newly registered NBFC looking to launch your first loan product or an established MFI managing thousands of loan accounts, the right Loan Origination System (LOS) can be the difference between scaling profitably and drowning in operational inefficiency. This comprehensive guide explores everything you need to know about NBFC loan origination software — what it is, how it works, what features to look for, and how Roopya’s platform is redefining the standard.

Start Free Trial

What Is NBFC Software for Loan Origination?

NBFC software for loan origination is a specialised digital platform that automates and streamlines the entire process of accepting, evaluating, approving, and disbursing loans. Unlike generic CRM tools or spreadsheet-based systems, a dedicated Loan Origination System (LOS) is purpose-built for the complexities of financial lending — credit risk assessment, regulatory compliance, KYC verification, and multi-stage approval workflows.

In traditional NBFC operations, loan origination is a highly manual process involving paper applications, physical document verification, branch-level credit assessments, and lengthy approval chains. This approach is not only slow — often taking 7 to 21 days per loan — but is also prone to human error, inconsistent credit decisions, and significant operational costs. NBFC loan origination software eliminates these inefficiencies by digitising and automating every step of the journey.

A modern LOS for NBFCs typically covers:

- Digital borrower onboarding and KYC

- Automated credit bureau checks (CIBIL, Experian, Equifax, CRIF)

- Document upload, OCR extraction, and verification

- Rule-based and AI-powered credit decisioning

- Multi-stage approval workflows

- eSign and digital agreement generation

- Loan disbursal coordination

- Seamless handoff to Loan Management System (LMS)

Why Is Loan Origination Software Critical for NBFCs in India?

India’s lending landscape is unique. NBFCs serve a wide spectrum of borrowers — from salaried urban professionals to self-employed traders and rural microfinance customers. Each segment demands a different loan product, risk framework, and operational approach. Manual systems simply cannot scale across these segments efficiently.

Here are the core reasons why investing in dedicated NBFC loan origination software is no longer optional — it’s existential:

1. Speed as a Competitive Advantage

Fintech lenders have fundamentally reset borrower expectations. Customers now expect loan decisions within minutes, not days. NBFCs that cannot match this speed lose business to digital-first competitors. A robust LOS enables straight-through processing for low-risk profiles, reducing turnaround time from days to hours or even minutes.

2. Regulatory Compliance and Audit Trails

The RBI’s evolving guidelines — from the digital lending guidelines of 2022 to the Account Aggregator framework — require NBFCs to maintain clear digital audit trails of every credit decision. Modern LOS platforms are built with compliance-first architecture, automatically generating the documentation and logs required for regulatory scrutiny.

3. Scalability Without Proportional Cost Increase

Hiring more loan officers to handle volume is expensive and introduces inconsistency. NBFC software for loan origination allows you to process 10x the loan applications with the same team by automating repetitive tasks — data entry, document verification, bureau checks, and preliminary scoring — freeing your team to focus on complex cases and customer relationships.

4. Consistent Credit Decisioning

Manual credit assessment introduces subjectivity and bias. A configurable Business Rule Engine (BRE) within a LOS enforces your credit policy consistently across every single application, regardless of the officer handling it. This consistency reduces both NPAs and the risk of discriminatory lending practices.

5. Data-Driven Insights

Every loan application passing through your LOS generates valuable data — conversion rates, drop-off points, rejection reasons, bureau score distributions. This data, when analysed through lending analytics, helps you refine your product, pricing, and credit policy continuously.

Key Features to Look for in NBFC Loan Origination Software

Not all LOS platforms are created equal. When evaluating NBFC software for loan origination, here is the feature checklist that separates enterprise-grade platforms from basic digital forms:

1. No-Code Loan Product Configuration

Your business team should be able to launch a new loan product — personal loan, MSME loan, gold loan, or LAP — without writing a single line of code. Look for platforms with intuitive product configurators that allow you to define tenure, interest rate bands, processing fees, eligibility criteria, and repayment schedules through a visual interface.

2. Digital KYC and e-KYC Integration

A compliant and seamless KYC process is foundational to digital lending. Your LOS should support Aadhaar-based eKYC, video KYC (VKYC), PAN verification, and facial recognition — all integrated natively or via pre-built API connectors to providers like NSDL, IDfy, Signzy, and others.

3. Credit Bureau Integration

Real-time integration with all four credit bureaus — CIBIL TransUnion, Experian, Equifax, and CRIF High Mark — is non-negotiable. The LOS should pull bureau reports automatically during the application process, extract key signals (credit score, DPD history, active loans, inquiries), and feed them into the decisioning engine without manual intervention.

4. Configurable Business Rule Engine (BRE)

The BRE is the brain of your loan origination system. It should allow your credit team to define complex eligibility and approval rules — across dozens of variables — using a no-code interface. Rules should be version-controlled, testable in a sandbox environment, and deployable without system downtime.

5. AI-Powered Credit Scoring

Beyond bureau scores, modern LOS platforms use machine learning models trained on alternative data — bank statement analysis, GST returns, utility payments, and behavioural signals — to generate proprietary credit scores. This is particularly valuable for thin-file borrowers who lack formal credit histories.

6. Automated Document Processing (OCR/AI)

Manual document review is one of the biggest bottlenecks in loan processing. AI-powered OCR (Optical Character Recognition) automatically extracts data from identity documents, bank statements, salary slips, and ITRs — populating application fields instantly and flagging anomalies or potential fraud.

7. Multi-Stage Workflow and Role-Based Access

Loan approval in an NBFC involves multiple stakeholders — credit analysts, underwriters, legal teams, and approving authorities. A good LOS provides configurable multi-stage workflows with role-based access control, SLA tracking, escalation rules, and a complete audit trail of every action taken on each application.

8. eSign and Loan Agreement Generation

Once a loan is approved, the agreement execution process should be entirely digital. Your LOS should auto-generate loan agreements populated with borrower-specific data and route them for eSign via Aadhaar-based or OTP-based electronic signatures, eliminating paper completely.

9. API-First Architecture

Your LOS should not operate as a silo. It must integrate seamlessly with your existing CRM, accounting software, payment gateways, collections systems, and third-party data providers through well-documented REST APIs. An open API architecture future-proofs your technology stack.

10. Embedded Compliance and Reporting

Regulatory reporting — from RBI’s CRILC reporting to internal credit risk reports — should be automated within the platform. Look for built-in templates for statutory compliance reports and the ability to generate custom dashboards for management review.

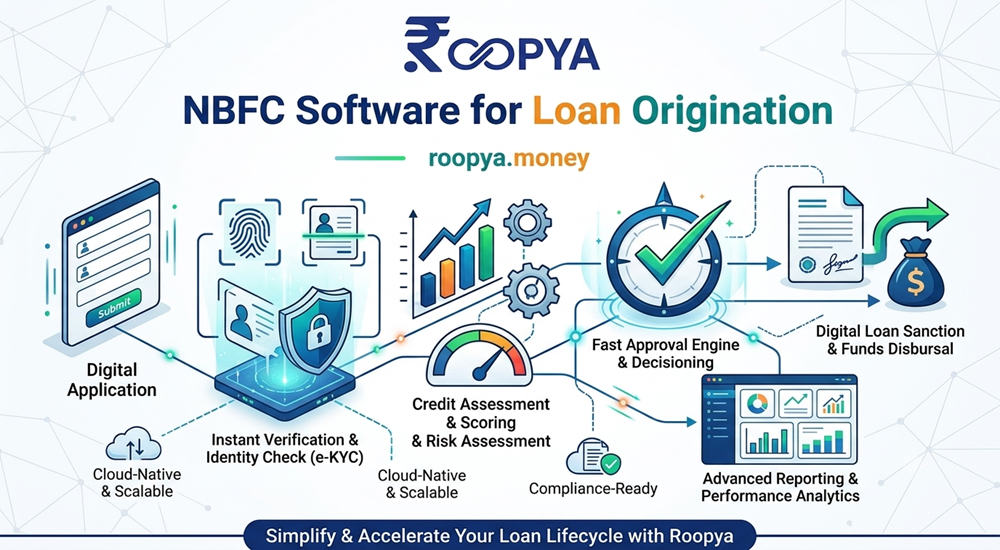

How Roopya’s NBFC Loan Origination Software Works

Roopya is a next-generation, no-code digital lending infrastructure platform purpose-built for NBFCs, Banks, and MFIs operating in India. The platform’s Loan Origination System is designed to take a borrower from application submission to loan disbursal with minimal manual intervention. Here is how it works:

Step 1: Digital Application Intake

Borrowers apply through a fully digital, mobile-responsive application form — accessible via web, mobile app, or embedded in your partner’s platform through Roopya’s embedded finance capabilities. The form is pre-configured for your specific loan product and captures all required information in a structured, validated format.

Step 2: Instant Identity Verification

As soon as the application is submitted, Roopya’s LOS triggers automated KYC verification — Aadhaar eKYC, PAN verification, facial liveness detection — through its library of 300+ pre-integrated APIs. The entire verification process completes in seconds, providing an instant first-level confirmation of the borrower’s identity.

Step 3: Automated Bureau Pull and Analysis

Simultaneously, the system pulls credit bureau reports from one or multiple bureaus as per your credit policy configuration. Roopya’s AI engine analyses the bureau report — extracting the credit score, repayment history, outstanding obligations, and derogatory marks — and generates a structured credit summary for the underwriter.

Step 4: Document Collection and AI Processing

Borrowers upload required documents — bank statements, salary slips, ITRs, or GST returns — directly on the platform. Roopya’s AI-powered document processing engine extracts key financial data points automatically, with 99%+ accuracy, and flags discrepancies or potential fraud indicators.

Step 5: Business Rule Engine Evaluation

The application, along with all enriched data points, is run through Roopya’s configurable Business Rule Engine. Your credit policy — eligibility criteria, risk bands, loan-to-income ratios, FOIR limits, geographic restrictions — is evaluated automatically in milliseconds. Applications are classified as auto-approved, referred for manual review, or auto-rejected with documented reasons.

Step 6: AI Credit Scoring

For borderline cases or thin-file borrowers, Roopya’s ML-powered credit scoring engine analyses alternative data sources — account aggregator data, bank statement cash flows, GST filing patterns — to generate a supplementary risk score, helping your underwriters make more informed decisions.

Step 7: Underwriter Review Dashboard

Applications requiring manual review land in a clean, intelligent underwriter dashboard. The underwriter sees a consolidated view of the borrower’s profile — bureau data, AI score, document analysis, bank statement summary, and BRE output — all in one place, enabling faster and better-informed decisions.

Step 8: Digital Agreement and eSign

Upon approval, Roopya auto-generates the loan agreement with all borrower-specific terms pre-populated. The agreement is sent to the borrower for eSign — Aadhaar-based or OTP-based — completing the entire documentation process without physical paperwork.

Step 9: Disbursal and LMS Handoff

Once the agreement is signed, the loan is ready for disbursal. Roopya coordinates with your payment gateway or banking partner to execute disbursal. The loan account is simultaneously created in Roopya’s Loan Management System, ensuring a seamless transition from origination to servicing.

Types of Loan Products Supported by Roopya’s LOS

Roopya’s NBFC software for loan origination is product-agnostic — it supports the full spectrum of lending products that NBFCs offer:

- Personal Loans – Salaried and self-employed personal loan processing with income verification and bureau-based decisioning

- Business and SME Loans – GST-based underwriting, business vintage checks, and cash flow analysis for MSME lending

- Microfinance Loans (MFI) – Group lending workflows, JLG assessments, and rural borrower onboarding

- Gold Loans – Collateral valuation integration and LTV-based approval logic

- Home Loans and LAP – Complex underwriting with property valuation, legal verification, and multi-party workflows

- Payday and Salary Advance Loans – Real-time employer verification and instant disbursal for short-tenure products

- Vehicle and Auto Loans – RC verification, dealer integration, and hypothecation management

- Buy Now Pay Later (BNPL) – Embedded credit decisioning for merchant partner platforms

The ROI of Implementing NBFC Loan Origination Software

Investing in a digital LOS is not just a technology decision — it is a direct investment in your NBFC’s profitability. Here is the tangible return on investment that Roopya’s customers experience:

Faster Processing = More Loans Per Officer

When origination tasks are automated, each loan officer can handle significantly more applications per day. A process that previously took 3-4 hours per application can be reduced to under 30 minutes of actual human effort — a 6-8x improvement in officer productivity.

Reduced Operational Costs

Eliminating paper, courier services, physical storage, and data-entry resources generates immediate cost savings. NBFCs typically see a 40-60% reduction in per-loan processing costs within the first year of LOS implementation.

Lower NPA Rates

Consistent, rule-based credit decisioning eliminates subjective errors that lead to bad loans. Combined with AI credit scoring and alternative data analysis, NBFCs using Roopya report improved early-stage risk detection and materially lower NPA rates compared to manual underwriting.

Higher Conversion Rates

A frictionless borrower experience — digital application, instant KYC, quick decisions — significantly reduces application drop-offs. NBFCs that digitise their origination process see borrower conversion rates improve by 30-50%, directly impacting loan book growth.

Faster Geographic Expansion

With a cloud-native LOS, your NBFC is not constrained by branch infrastructure. New geographies and distribution channels — DSA networks, fintech partners, co-lending arrangements — can be onboarded on the same platform without additional technology investment.

Roopya vs Traditional NBFC Loan Origination Approaches

To understand the transformation Roopya delivers, it helps to compare it against the traditional approaches NBFCs have relied on:

- Traditional Manual Process: 10-21 day TAT | High error rate | No scalability | Zero data visibility

- Spreadsheet + Legacy Software: Partial automation | Siloed data | High IT maintenance | Compliance risk

- Custom-Built Software: 12-18 month build time | High CapEx | Ongoing maintenance burden | Inflexible

- Roopya LOS: 1-day go-live | No-code configuration | Pay-as-you-use pricing | 300+ pre-integrated APIs | Full compliance | AI-powered decisioning

Security and Compliance Architecture

For NBFCs, data security and regulatory compliance are not features — they are fundamental requirements. Roopya’s platform is built with a security-first architecture:

- ISO 27001-aligned information security practices

- End-to-end encryption of all borrower data at rest and in transit

- RBI Digital Lending Guidelines 2022 compliant workflows

- Account Aggregator (AA) framework integration for consent-based financial data sharing

- Role-based access control with complete audit logs

- DPDP Act 2023 compliant data handling and consent management

- Automated regulatory report generation for RBI submissions

Getting Started with Roopya: The Fastest Path to a Live Loan Origination System

One of the most remarkable aspects of Roopya’s platform is its deployment speed. Traditional LOS implementations at NBFCs take 6-18 months of IT project work before a single loan can be processed. Roopya’s no-code, plug-and-play infrastructure is designed to get you live in a single day.

Here is what the onboarding journey looks like:

- Day 1: Sign up, configure your first loan product using Roopya’s product wizard, and integrate your existing KYC and bureau connectors

- Day 1-3: Configure your Business Rule Engine with your credit policy, set up approval workflows, and test in sandbox

- Day 3-7: Go live with a controlled pilot — process real applications, refine rules, and train your team on the dashboard

- Day 7+: Scale — add more loan products, onboard DSA partners, enable new bureau or data integrations, and leverage analytics

With zero upfront costs and a pay-as-you-use pricing model, Roopya is accessible to NBFCs at every stage — from newly registered entities processing their first loans to established players looking to modernise and scale.

Conclusion: The Future of NBFC Lending is Digital and It Starts with Origination

The loan origination process is where your NBFC’s relationship with a borrower begins. It sets the tone for the entire lending relationship — borrower experience, credit quality, operational efficiency, and regulatory compliance. Getting origination right is getting everything right.

Roopya’s NBFC software for loan origination gives you the technology infrastructure to compete in the modern lending landscape — not just surviving today’s challenges but positioning your NBFC to lead the next decade of India’s credit growth story.

From your first digital loan application to your ten-thousandth automated approval, Roopya is built to scale with you. Start today — go live tomorrow.