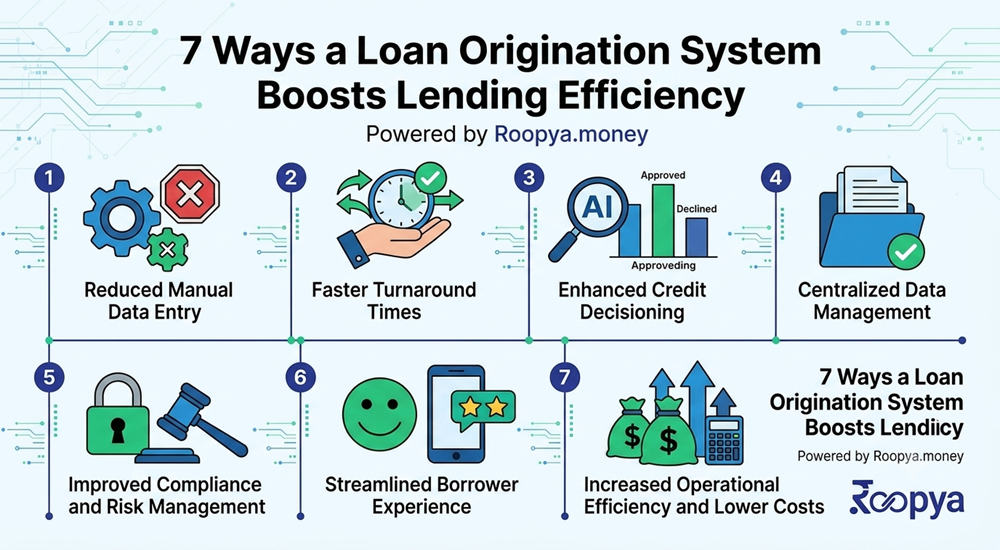

7 Ways a Loan Origination System Boosts Lending Efficiency

Every lending business faces the same fundamental challenge: how to process more loan applications, faster, with fewer errors, at lower cost — while maintaining tight risk controls and regulatory compliance. For decades, the answer was to hire more people, build more branches, and tolerate the inefficiency of paper-based workflows. That era is over.

The Loan Origination System (LOS) has emerged as the defining technology of modern lending. It is the digital infrastructure layer that transforms a slow, manual, error-prone origination process into a streamlined, automated, data-driven engine for growth. NBFCs, banks, microfinance institutions, and fintech lenders across India that have adopted a modern LOS are not just doing the same things faster — they are doing fundamentally different things that were simply impossible before.

In this Blog, we break down the seven most impactful ways a Loan Origination System boosts lending efficiency — and show exactly how Roopya, India’s leading no-code lending infrastructure platform, delivers each of these advantages to lenders of every size.

Start Free Trial

Whether you are a newly licensed NBFC looking to build your origination stack from scratch, or an established lender seeking to modernise a legacy process, this guide will give you a clear picture of what a world-class LOS can do for your business.

Way 1: Eliminating Paper-Based Processes and Manual Data Entry

The Problem with Manual Origination

In a traditional lending environment, a borrower fills out a physical application form. That form is then manually keyed into a system by an operations executive — introducing transcription errors at the very first step. Supporting documents are physically collected, physically sorted, physically filed, and then manually reviewed by a credit analyst who may spend 20–30 minutes on each application extracting key data points.

Consider the scale of waste this introduces. If an NBFC processes 500 applications per month and each manual entry takes 25 minutes, that is over 200 person-hours spent on data entry alone — before a single credit decision is made. Add in document filing, retrieval, re-keying into downstream systems, and error correction, and the true cost of manual origination becomes staggering.

How a Loan Origination System Solves This

A modern Loan Origination System eliminates manual data entry at every stage. Borrowers complete digital application forms that feed directly into the system — no re-keying, no transcription errors, no filing. AI-powered Optical Character Recognition (OCR) automatically extracts data from uploaded documents — PAN cards, Aadhaar cards, salary slips, bank statements, ITR documents — with accuracy exceeding 99%.

Roopya’s LOS takes this further with intelligent document processing that not only extracts data but cross-validates it against other inputs and bureau data, flagging inconsistencies automatically. A process that once required a trained analyst spending half an hour per file is completed in seconds — with higher accuracy and a full digital audit trail.

📊 Roopya lenders report 40–60% reduction in per-application processing costs after switching from manual workflows.

The Efficiency Gain

The result is not just speed — it is a fundamental reallocation of human capital. Your operations team stops spending time on data entry and document management and starts spending time on genuinely complex cases that require human judgment. The LOS handles the routine; your people handle the exceptional.

Way 2: Accelerating KYC and Identity Verification

Why KYC Is a Bottleneck in Traditional Lending

Know Your Customer (KYC) compliance is non-negotiable in Indian lending. Every borrower must be verified against Aadhaar, PAN, and other identity databases before a credit facility can be extended. In a traditional workflow, this means physically collecting identity documents, manually verifying them, sometimes dispatching a field agent for in-person verification, and waiting for confirmation — a process that can take one to three days per application.

For borrowers accustomed to digital experiences — instant food delivery, same-day e-commerce — a three-day KYC wait is not just inconvenient. It is a reason to abandon the application entirely and approach a faster competitor.

Instant Digital KYC Through LOS Integration

A Loan Origination System integrates directly with India’s digital identity infrastructure. When a borrower submits an application and provides consent, the LOS simultaneously triggers Aadhaar eKYC through UIDAI, PAN verification through NSDL, and Digilocker document retrieval — all in real time, with results returned in two to five seconds.

For cases requiring face-match verification, Roopya’s LOS integrates with Video KYC (VKYC) providers, enabling a fully compliant, remote face-match verification in under three minutes. For borrowers who prefer a fully asynchronous process, AI-powered face-match against Aadhaar photo is available as an alternative.

The entire KYC process — which once took days and required human intervention at every step — is now completed before the borrower has finished filling out their application. Roopya’s 300+ pre-integrated APIs include all major KYC service providers, meaning there is no custom development required to access this capability.

📊 KYC completion time reduced from 1–3 days to under 3 minutes with Roopya’s integrated LOS.

Compliance Without Compromise

Critically, digital KYC through a Loan Origination System is not a shortcut around compliance — it is compliance at higher quality. Every eKYC event generates a detailed audit log with timestamp, consent record, and verification outcome. RBI audit requirements are met automatically, and the risk of human error in manual KYC is eliminated entirely.

Way 3: Automating Credit Bureau Checks and Underwriting Data Collection

The Manual Bureau Pull Problem

Credit bureau data — from CIBIL, Experian, CRIF High Mark, or Equifax — is the foundation of retail credit underwriting in India. In a manual process, triggering a bureau pull requires an operations executive to log into a bureau portal, enter the borrower’s details manually, download the report, save it to a shared drive, and then physically hand it to the underwriter. Each of these steps takes time, introduces error risk, and creates gaps in the audit trail.

When an NBFC is processing hundreds of applications per week, the cumulative time spent on manual bureau pulls becomes a significant drag on throughput. And because bureau pulls are typically triggered only after initial data entry is complete, they add a sequential delay to the process — the underwriter cannot begin work until the bureau report arrives.

Automated, Simultaneous Bureau Pulls

A Loan Origination System integrates with all four major credit bureaus through pre-built API connections. The moment a borrower submits their application and provides digital consent, the LOS simultaneously triggers pulls from the configured bureaus — no human action required. Bureau reports are returned, parsed, and structured within the application record in real time.

Roopya’s LOS goes further by automatically extracting key underwriting data points from the bureau report — credit score, credit history length, number of open accounts, DPD (Days Past Due) history, enquiry count — and mapping them to the credit decisioning engine. Underwriters who previously spent 20 minutes reading and summarising bureau reports now see a clean, structured data panel with all relevant fields pre-extracted.

For complex cases involving multiple co-applicants or guarantors, the Roopya LOS triggers parallel bureau pulls for all parties simultaneously, cutting total turnaround time dramatically compared to sequential manual pulls.

📊 Bureau pull turnaround reduced from 15–20 minutes (manual) to under 10 seconds with Roopya’s LOS.

Multi-Bureau Waterfall Logic

Roopya’s LOS also supports waterfall bureau logic — where a primary bureau is queried first, and secondary bureaus are triggered automatically if the primary returns a thin file or no-hit result. This ensures maximum credit data coverage for new-to-credit and thin-file borrowers without requiring manual intervention.

Way 4: Enabling Real-Time, AI-Driven Credit Decisioning

The Cost of Slow Credit Decisions

In a competitive lending market, time-to-decision is a critical conversion metric. Research consistently shows that conversion rates drop sharply as application-to-decision time increases. A borrower who applies for a personal loan and receives a decision within five minutes is significantly more likely to accept the loan offer than one who is told to wait 24–48 hours for an answer.

Manual underwriting is inherently slow. Even an experienced credit analyst takes 30–60 minutes to properly review a complete application — bureau report, income documents, bank statement analysis, credit policy check — before reaching a decision. During peak periods, applications queue up and wait-times multiply. The business impact is direct: delayed decisions mean lower conversion, higher abandonment, and lost revenue.

No-Code Business Rule Engine and AI Scoring

A Loan Origination System replaces manual underwriting with a combination of automated rule-based decisioning and AI-powered credit scoring. The Business Rule Engine (BRE) — the heart of the LOS — encodes your credit policy as a set of configurable rules that are applied to every application automatically and consistently.

In Roopya’s LOS, the BRE is fully no-code — credit and risk managers can define, modify, and test decisioning rules through an intuitive visual interface, without writing a single line of code. Rules can reference any combination of application data, bureau outputs, income metrics, employment parameters, geographic factors, and product-specific eligibility criteria.

On top of rule-based decisioning, Roopya’s AI scoring models continuously learn from portfolio performance data, improving their predictive accuracy over time. Applications that pass rule-based filters are scored against these models, enabling nuanced, risk-adjusted decisioning that goes beyond simple cutoff-based logic.

📊 Decision turnaround time reduced from 24–48 hours to under 60 seconds for straight-through applications on Roopya’s LOS.

Three-Tier Decision Routing

Not every application can or should be decided automatically. Roopya’s LOS implements a three-tier routing logic: straight-through approval for clean profiles that meet all criteria; straight-through rejection for applications that breach hard cutoffs; and refer-to-manual-review for borderline cases where human judgment adds value. This triage ensures your underwriting team focuses only on cases where they can genuinely make a difference, while automation handles the rest.

Way 5: Streamlining Documentation, eSign, and Offer Management

The Documentation Drag in Traditional Lending

Once a credit decision is made, a traditional lending process enters its most paper-intensive phase: generating loan sanction letters, preparing loan agreements, coordinating physical signatures, managing courier logistics, and reconciling returned documents before disbursement. Each of these steps involves multiple handoffs between teams — credit, operations, legal, customer service — and each handoff is a potential delay point.

Physical documentation also creates significant compliance risk. Documents can be lost, damaged, or tampered with. Version control is difficult. And retrieval for audit purposes — which may be required years after the original transaction — is time-consuming and error-prone.

Digital Documentation and eSign Through LOS

A Loan Origination System automates the entire post-decision documentation workflow. When an application is approved, the LOS automatically generates the sanction letter and loan agreement, pre-populated with all relevant data from the application — no manual document preparation required. The borrower receives these documents digitally and can review, query, and sign them entirely within the digital platform.

Roopya’s LOS integrates with eSign providers that enable Aadhaar OTP-based digital signing — legally valid under the Information Technology Act, 2000, and accepted by all Indian regulators. The borrower signs from their smartphone in under two minutes, without printing a single page or visiting a branch.

Every signed document is stored securely in the digital record, with a complete version history, timestamp, and audit trail. Document retrieval for compliance, legal, or audit purposes takes seconds rather than hours.

Personalised Loan Offer Engine

Roopya’s LOS includes a sophisticated loan offer engine that generates personalised offers based on the borrower’s credit profile, product eligibility, and your current pricing strategy. Offers can include multiple tenure options, interest rate variants, and EMI scenarios — presented to the borrower in a clear, comparative format. Digital offer acceptance is captured instantly, with no manual paperwork.

📊 Documentation cycle time reduced from 3–5 days to under 2 hours with Roopya’s digital documentation and eSign integration.

Way 6: Providing End-to-End Visibility and Operational Analytics

The Blind Spots of Manual Origination

One of the most underappreciated costs of manual origination processes is the loss of data and visibility. When applications are tracked in spreadsheets, decisions are made verbally, and documents are filed in physical folders, there is no reliable way to answer basic operational questions: How many applications are currently in progress? What is the average time from application to disbursement? Which stage is causing the most delays? Which credit officer has the highest approval rate — and is that rate appropriate given their portfolio’s subsequent performance?

Without answers to these questions, management is flying blind. Process improvement is based on intuition rather than data. Problems compound quietly until they become crises.

Real-Time Dashboards and Pipeline Visibility

A Loan Origination System creates a complete, real-time data record of every application and every action taken on it. This data is surfaced through operational dashboards that give management instant visibility into the entire origination pipeline — how many applications are at each stage, what the average dwell time at each stage is, and where bottlenecks are forming.

Roopya’s LOS provides role-specific dashboards for every level of the organisation. Operations managers see pipeline health and team productivity. Risk managers see approval rates, rejection reason distribution, and policy exception frequency. Senior leadership sees portfolio-level metrics — average ticket size, product mix, channel performance, and geographic distribution — in real time.

Turnaround Time Analytics and SLA Management

Roopya’s LOS tracks Turnaround Time (TAT) at every stage of the origination process — from application receipt to KYC completion, from bureau pull to credit decision, from sanction to disbursement. SLA thresholds can be configured for each stage, with automatic alerts when applications breach SLA limits. This transforms TAT management from a reactive, exception-based activity to a proactive, data-driven discipline.

Credit Policy Performance Analytics

Beyond operational metrics, Roopya’s LOS provides credit policy performance analytics — tracking how specific rule combinations are performing in terms of approval rates, subsequent delinquency, and portfolio yield. This closes the feedback loop between credit policy and portfolio outcomes, enabling continuous, data-driven policy improvement.

📊 Lenders using Roopya’s analytics dashboard report 25–35% improvement in origination TAT within the first 90 days of implementation.

Way 7: Enabling Scalable, Multi-Channel, Multi-Product Origination

The Scaling Problem in Manual Lending

A manual origination process has a hard scaling ceiling. To process more applications, you need more people. To reach more borrowers through more channels, you need more infrastructure. To add a new loan product, you need to build new workflows from scratch. Each dimension of growth requires proportional investment in headcount, training, and operational overhead.

This is why traditional lenders struggle to scale into new geographies, new customer segments, or new product categories without massive upfront investment. The economics of manual origination do not improve with volume — they just get more expensive.

Horizontal Scaling Through LOS Architecture

A cloud-based Loan Origination System scales horizontally — handling increases in application volume without proportional increases in cost or headcount. The same system that processes 100 applications per month can process 100,000, with identical turnaround times and quality standards. Infrastructure scales automatically in response to demand, with no manual provisioning required.

Roopya’s LOS is built on a cloud-native, microservices architecture that has been stress-tested at enterprise scale. Whether you are an early-stage NBFC processing your first hundred applications or a mature lender handling thousands per day, the platform delivers consistent performance.

Multi-Channel Origination from a Single Platform

Modern borrowers come through multiple channels — direct website or app, DSA or agent networks, fintech partnerships, corporate tie-ups, and embedded finance integrations. Each channel may have different product offerings, interest rates, documentation requirements, and customer journeys. Managing these in a manual environment requires separate teams, separate processes, and constant reconciliation.

Roopya’s LOS manages all channels through a single, unified backend. Channel-specific application forms, pricing rules, and workflow configurations are maintained within the platform. A DSA-submitted application follows a different journey than a direct-digital application, but both are tracked, measured, and managed in the same system. Cross-channel analytics give management a unified view of origination performance.

Multi-Product Management Without Additional Complexity

Adding a new loan product — say, a gold loan or a supply chain finance facility — to a manual origination process means building new forms, training new staff, and creating new workflows from scratch. In Roopya’s LOS, new products are configured through the no-code interface in hours, not months. Pre-built product journey templates for 20+ loan types mean most configurations require minimal customisation.

Embedded Finance and API-First Origination

The future of lending is embedded — loan products delivered within the apps and platforms where borrowers already spend their time. Roopya’s LOS exposes a comprehensive API layer that allows partner platforms to originate loans on behalf of their users without redirecting them to a separate lender portal. The borrower experience is seamless; the credit decision, KYC, and disbursement happen invisibly in the background.

This API-first architecture also enables co-lending arrangements, buy-now-pay-later integrations, payroll-linked lending, and other emerging origination models — all managed within the same LOS without additional infrastructure.

📊 Roopya lenders have expanded to 3x more channels within 6 months of implementation without adding origination headcount.

The Roopya Advantage: All 7 Efficiency Gains in One Platform

Each of the seven efficiency gains described above can theoretically be achieved through a patchwork of separate tools — a KYC provider here, a bureau integration there, a document management system somewhere else. But this approach creates its own inefficiencies: integration complexity, data silos, multiple vendor relationships, inconsistent audit trails, and a fragmented borrower experience.

Roopya delivers all seven efficiency gains through a single, unified, no-code platform — purpose-built for the Indian lending market. Here is what that means in practice:

- Single integration, full capability: Connect once to Roopya and access 300+ pre-integrated APIs covering every aspect of the origination workflow — no individual integrations to build or maintain.

- No-code configuration: Every aspect of the origination workflow — application forms, KYC rules, bureau triggers, BRE logic, documentation templates, offer parameters, channel configurations — is configurable through an intuitive interface. Your business team owns the platform, not your IT department.

- 1-day go-live: Pre-configured product journeys for 20+ loan types mean you can launch a new product or channel in hours, not months.

- Pay-as-you-use pricing: No upfront licence fees, no capital expenditure. You pay based on actual origination volume, aligning Roopya’s commercial model with your growth.

- RBI compliance built in: Every regulatory requirement — KYC norms, PMLA compliance, data localisation, credit bureau reporting, CERSAI filing, Fair Practice Code — is addressed within the platform and continuously updated as regulations evolve.

- AI and ML throughout: Document intelligence, fraud detection, credit scoring, and policy analytics are all powered by AI that improves continuously as your portfolio data grows.

- Trusted by modern lenders: IndiaKaLoan, QuickFinShop, Recapita, Findoc, EazyCredit, and dozens of other leading NBFCs and fintechs run their origination operations on Roopya.

Is Your Origination Process Ready for a Loan Origination System?

If you are still relying on manual data entry, spreadsheet-based tracking, physical document management, or legacy core banking modules for origination, you are operating at a significant disadvantage to competitors who have already made the transition.

The question is not whether to adopt a Loan Origination System — the efficiency case is overwhelming. The question is which LOS to choose, and how quickly you can get it live. With Roopya, the answer to the second question is: tomorrow.

Roopya offers a full-featured demo and a no-obligation proof-of-concept implementation that lets you see the platform in action with your own loan products, your own credit policy, and your own borrower journey — before committing to a long-term deployment.

The lenders who are winning in India’s digital credit market today are not the ones with the largest branch networks or the biggest headcounts. They are the ones who invested early in the right technology infrastructure. A world-class Loan Origination System is that infrastructure. Roopya is that system.