The OCEN API is a set of programming interfaces that allows developers to access the Open Credit Enablement Network (OCEN) platform's functionality and integrate it with other applications or services. The API provides a standard way for developers to interact with the OCEN platform and build innovative solutions that leverage its capabilities.

The OCEN API enables developers to access a range of services and data on the platform, including borrower information, loan application details, credit scores, and transaction history, among others. Developers can use the API to create new applications, such as loan management tools, credit scoring models, and fraud detection systems, among others.

The API is designed to be simple and easy to use, with clear documentation and code samples to help developers get started quickly. It adheres to modern web standards, such as RESTful architecture and JSON data format, which make it easy to integrate with other applications and services.

Overall, the OCEN API is an essential component of the platform, providing developers with the tools they need to build innovative solutions that leverage its capabilities and promote financial inclusion in India.

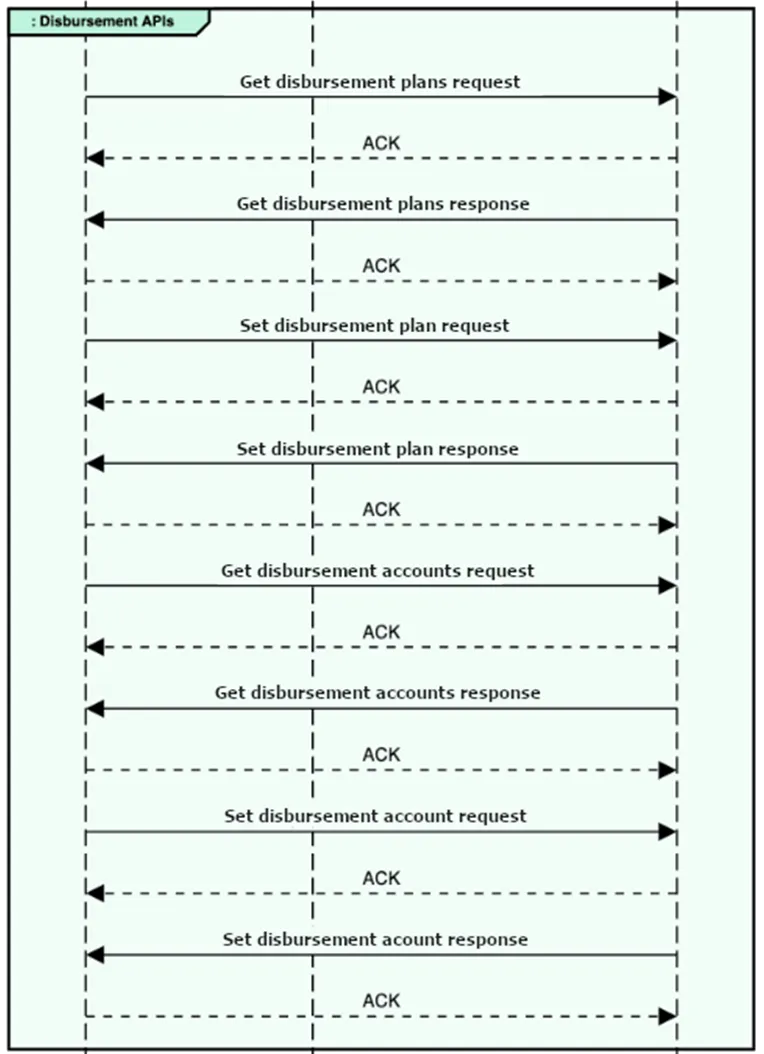

Here are some key APIs that are involved in OCEN transactions:

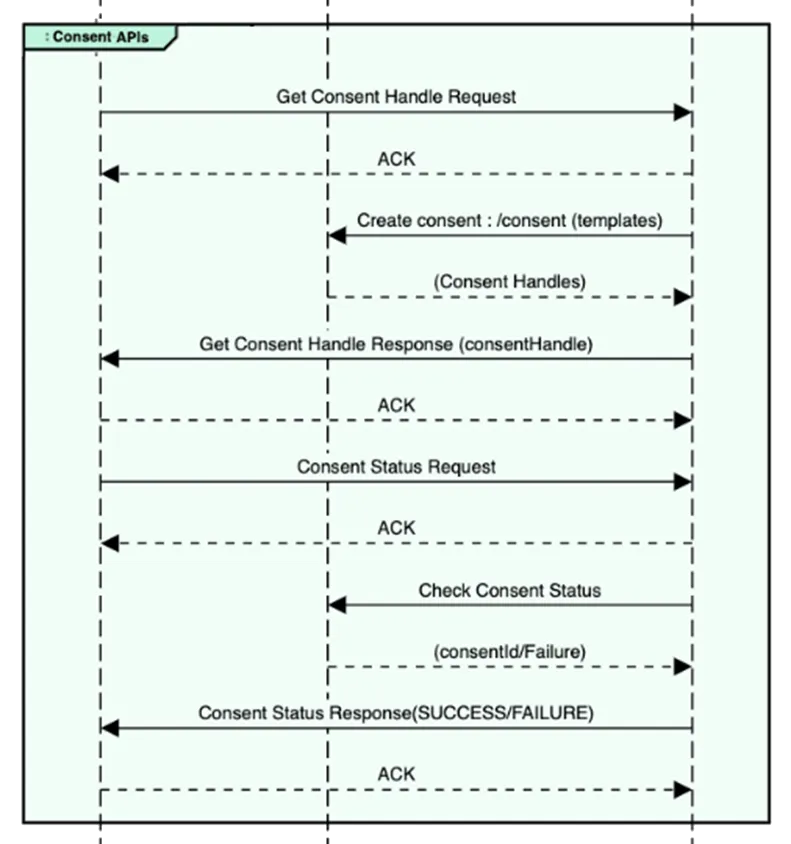

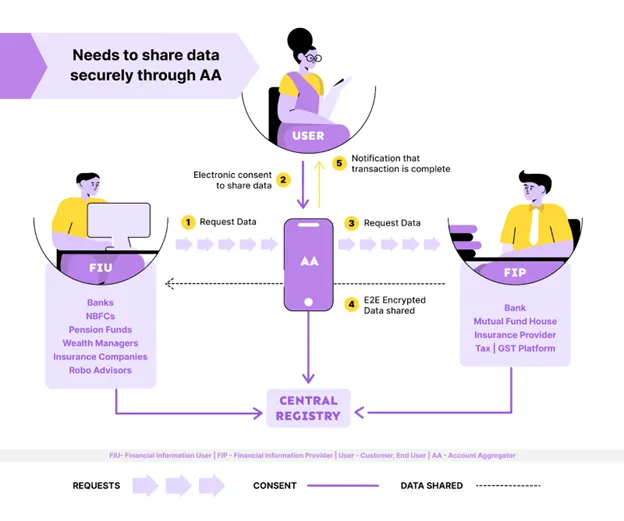

- KYC API: This API is used to perform Know Your Customer (KYC) verification for borrowers, which is a mandatory requirement for accessing credit on the OCEN platform.

- Credit Bureau API: This API is used to access credit scores and credit reports from credit bureaus, which are used to assess the creditworthiness of borrowers.

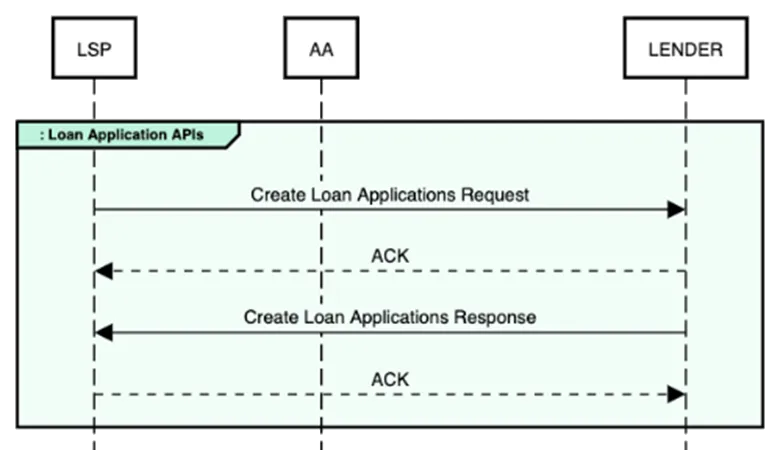

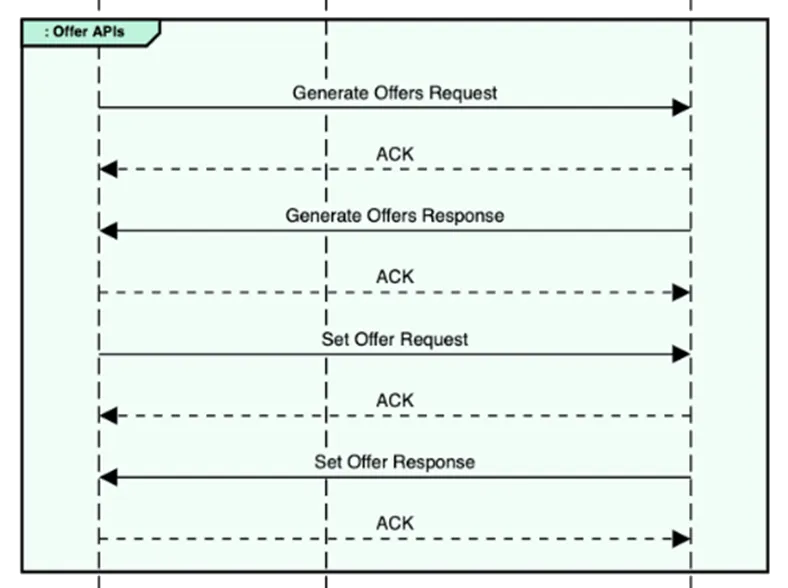

- Loan Origination API: This API is used to initiate loan applications on the OCEN platform, including capturing borrower details, loan amount, and repayment terms.

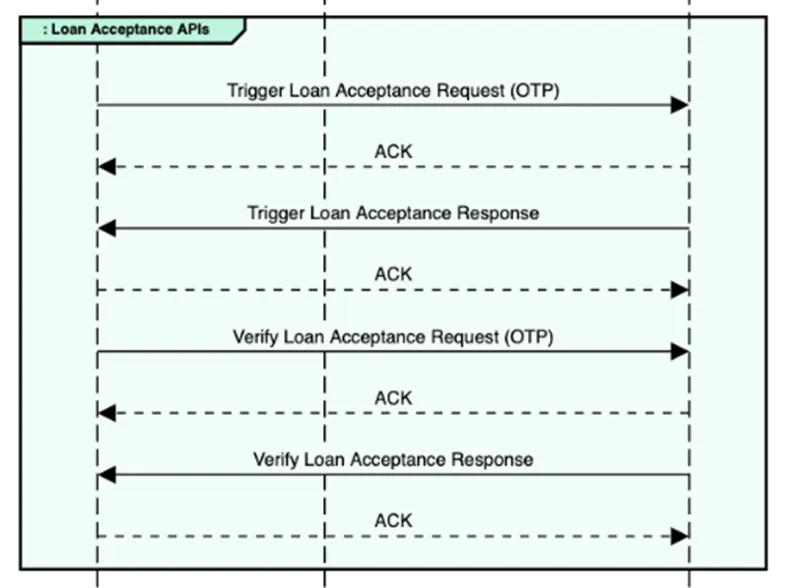

- Loan Servicing API: This API is used to manage loan servicing activities, such as disbursing funds, collecting payments, and managing delinquencies.

- Payment Gateway API: This API is used to process loan payments and manage transaction settlements between lenders and borrowers.

- Fraud Detection API: This API is used to detect and prevent fraud in loan applications and loan servicing activities.

- Analytics API: This API is used to access data analytics and reporting tools on the OCEN platform, which can be used to monitor loan performance, identify trends, and improve decision-making.

These are just some of the APIs that may be involved in OCEN transactions. The specific APIs used may vary depending on the needs of lenders, borrowers, and service providers on the platform.