What is Scorecard Development and How to Build Credit Scorecard on Application, Behavioural and Collection

What is a Scorecard?

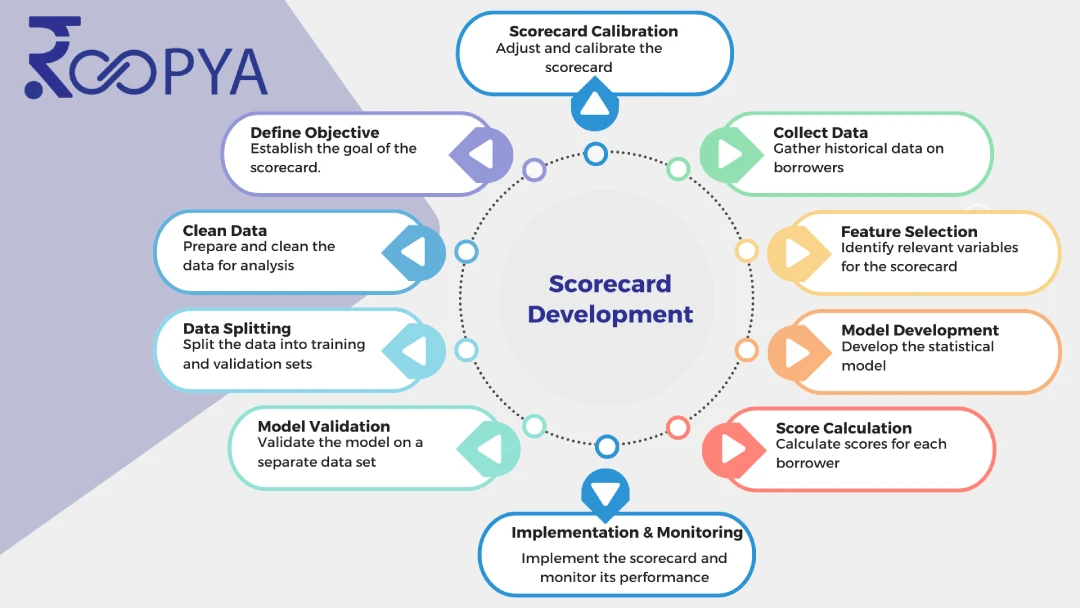

A scorecard in credit risk modelling is a statistical model used by lenders to evaluate the creditworthiness of potential borrowers. It helps in predicting the likelihood of whether a borrower will repay a loan or not. The scorecard is developed through the analysis of historical data on borrowers and their loan repayment behaviour. This model assigns scores to various attributes or characteristics of the borrower, such as income level, employment history, credit history, debts, and other financial indicators.

Start Free Trial

For example, a simple credit scorecard might assign points based on factors like:

- Credit History: The number of years you’ve had credit, the types of credit accounts (credit cards, mortgages, car loans, etc.), your payment history, and any defaults or late payments. A longer, positive credit history might score higher than a short or negative history.

- Debt Levels: Your current debt levels, including credit card balances, student loans, and other debts compared to your income, known as your debt-to-income ratio. Lower ratios generally score higher.

- Income and Employment: Stable employment and a higher income can contribute positively to your score, reflecting your ability to repay.

- New Credit and Inquiries: The number of recent credit account applications and new credit accounts. Applying for many new accounts in a short period can lower your score.

- Use of Credit: How much of your available credit you’re using, particularly on revolving accounts like credit cards. Lower utilization rates are usually better for your score.

Each factor is weighted differently depending on how predictive it is of future default. For instance, credit history and debt levels might be weighted more heavily than new credit inquiries.

Lenders use credit scorecards to make lending decisions, set interest rates, and establish credit limits. They can be customized for different types of credit products and for specific risk appetites of the lender. Credit scorecards are a critical tool in the financial industry for managing credit risk, ensuring responsible lending, and helping consumers access credit.