Best Loan Origination Software: Complete Guide for NBFCs, Banks & Modern Lenders

Why Loan Origination Software Is No Longer Optional

The lending industry in India is undergoing one of the most transformative shifts in its history. With over 10,000 registered NBFCs, hundreds of cooperative banks, and a rapidly growing microfinance sector, the competition for quality borrowers has never been more intense. Yet the underlying processes at many lending institutions — manual credit checks, paper-based KYC, slow disbursal cycles — remain stuck in the past.

This is exactly where loan origination software (LOS) becomes a game-changer.

A modern loan origination system is far more than a digital application form. It is the nerve center of your entire lending workflow — from the moment a borrower expresses interest to the final disbursal of funds. The right LOS automates credit scoring, verifies documents in real time, enforces your credit policy through a configurable business rule engine, and connects seamlessly with credit bureaus, payment gateways, and KYC providers.

Start Free Trial

For NBFCs, banks, MFIs, and fintech lenders in India, choosing the best loan origination software can mean the difference between disbursing loans in minutes versus days — and between building a scalable lending operation versus one that drowns in manual work.

In this guide, we break down everything you need to know: what loan origination software is, what features matter most, how to evaluate vendors, and why Roopya stands out as one of India’s most powerful and flexible loan origination platforms.

What Is Loan Origination Software?

Loan origination software is a technology platform that manages the end-to-end process of creating a new loan — from lead capture and application, through underwriting and credit assessment, to approval and disbursal.

The “loan origination” process typically includes:

- Lead capture and borrower onboarding — Collecting applicant details via digital forms or partner channels

- KYC and identity verification — Aadhaar-based eKYC, PAN validation, video KYC (VKYC)

- Document collection and verification — Income proofs, bank statements, ITR, GST filings

- Credit bureau pulls — CIBIL, Equifax, Experian, CRIF High Mark checks

- Automated underwriting and credit scoring — Applying your credit policy and scorecards to assess creditworthiness

- Decision engine — Approve, reject, or refer to manual review based on rules

- Offer generation and acceptance — Presenting loan terms to the borrower

- Legal documentation and e-signing — Digital loan agreements via e-sign and e-stamp

- Disbursal — Transfer of funds to the borrower’s bank account

A strong LOS compresses what was once a 7–14 day process into a matter of minutes or hours.

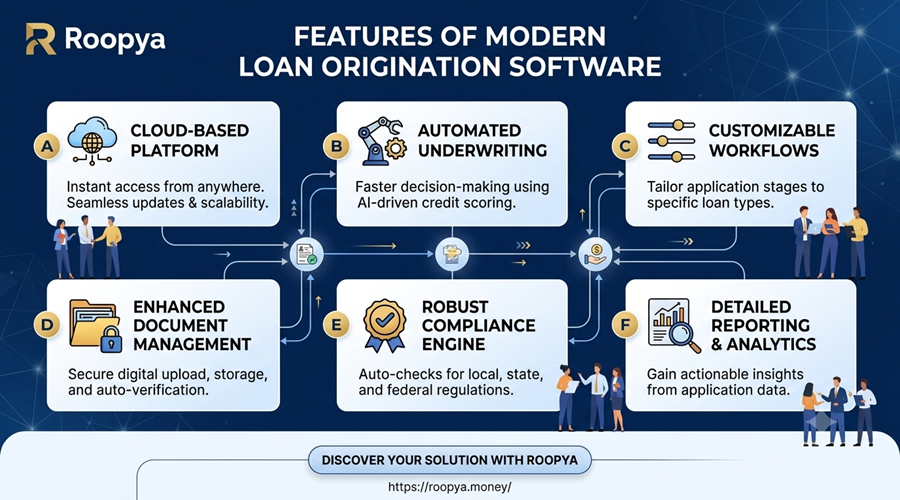

Key Features to Look for in the Best Loan Origination Software

Not all LOS platforms are created equal. When evaluating options, here are the critical capabilities that separate best-in-class systems from the rest:

1. No-Code Configurability

The best loan origination software lets your business team configure products, workflows, and credit rules — without writing code. This is essential because lending products evolve constantly. If every change requires a developer sprint, your institution will always be one step behind the market.

Look for platforms with a visual workflow builder, drag-and-drop rule configuration, and the ability to launch new loan products without IT involvement.

Roopya’s Advantage: Roopya is a truly no-code platform. Business users can configure loan products, credit policies, and customer journeys entirely through an intuitive visual interface — zero coding required.

2. Business Rule Engine (BRE)

The Business Rule Engine is the policy enforcement layer of your LOS. It applies your credit policy automatically — checking income thresholds, FOIR limits, bureau scores, fraud flags, and hundreds of other parameters — to make or recommend credit decisions.

A good BRE should be:

- Self-configurable — no-code rule creation

- Auditable — full logging of every decision and the rules applied

- Adaptive — able to learn from past approvals and rejections over time

Roopya’s Advantage: Roopya’s AI-Enhanced Business Rule Engine uses machine learning to suggest rule improvements, identify patterns in approvals and rejections, and adapt to market conditions automatically — while maintaining full human oversight.

3. Pre-integrated API Ecosystem

Loan origination involves dozens of third-party integrations: credit bureaus, bank statement analyzers, GST verification, Aadhaar eKYC, video KYC, e-stamp, e-sign, payment gateways, and more. Building these integrations in-house is expensive and time-consuming.

The best LOS comes with a pre-integrated library of APIs covering the full origination lifecycle — so you can go live quickly without months of integration work.

Roopya’s Advantage: Roopya offers 300+ pre-integrated APIs covering credit bureaus, KYC, document verification, payment gateways, and more. Everything is ready out of the box.

4. AI-Powered Document Verification

Manual document review is slow, error-prone, and expensive. Modern LOS platforms use Optical Character Recognition (OCR), Natural Language Processing (NLP), and AI to automatically extract data from documents, cross-verify them against submitted information, and flag anomalies.

This capability dramatically reduces processing time and fraud risk — especially for documents like salary slips, bank statements, Form 16, and ITR.

Roopya’s Advantage: Roopya’s AI-powered document analysis achieves 99%+ accuracy, processing documents in seconds with built-in fraud detection.

5. Configurable Credit Scorecards

Off-the-shelf credit bureau scores are a starting point — but the best lending decisions come from custom scorecards tailored to your borrower segment, loan product, and risk appetite. Your LOS should support the integration of proprietary scorecards and allow bureau data to be supplemented with alternative data sources.

Roopya’s Advantage: Roopya’s Intelligent Credit Decisioning analyzes thousands of data points beyond traditional credit scores, including alternative data and behavioral patterns, to provide accurate real-time risk assessments in milliseconds.

6. Multi-Channel Borrower Journeys

Borrowers today expect to apply for loans on their terms — via a web app, mobile app, WhatsApp, or through a DSA agent’s tablet. Your LOS should support omnichannel origination, maintaining a single application record regardless of which channel the borrower uses.

Roopya’s Advantage: Roopya supports automated customer loan journeys across channels, with pre-configured digital application flows for 20+ loan product types — from personal loans to business credit.

7. Speed of Deployment

One of the most overlooked factors when selecting an LOS is how long it takes to go live. Legacy enterprise platforms often require 6–18 months of implementation. In a competitive lending market, this delay is unacceptable.

Roopya’s Advantage: Roopya’s plug-and-play infrastructure enables you to go live in as little as 1 day — the fastest deployment time in the Indian market.

8. Regulatory Compliance

The RBI and SEBI continuously update their guidelines on digital lending, KYC norms, and data privacy. Your LOS must stay current with these changes — or you risk enforcement action, audits, or reputational damage.

Roopya’s Advantage: Roopya’s platform is continuously updated to ensure full compliance with the latest RBI regulations and digital lending guidelines.

9. Advanced Fraud Detection

Loan fraud — whether through identity theft, income fabrication, or collusion — is a growing problem in India’s lending ecosystem. Modern LOS platforms use AI to detect suspicious patterns at the application stage, before disbursal.

Roopya’s Advantage: Roopya’s advanced fraud detection module uses AI-powered algorithms to detect suspicious patterns across all applications, reducing fraud by up to 80%.

10. Integration with Loan Management System (LMS)

Origination does not happen in isolation. The best LOS platforms either include an integrated Loan Management System or connect seamlessly with one. This ensures that once a loan is disbursed, it flows directly into servicing, repayment tracking, collections, and reporting — without manual data entry.

Roopya’s Advantage: Roopya is a unified lending platform covering origination, management, collections, early warning systems, and lending analytics — all in one integrated suite.

Types of Loans That Benefit Most from a Modern LOS

Loan origination software is not just for large banks. Every lending institution — regardless of size or loan type — benefits from automation. Here is how different loan verticals gain from a modern LOS:

Personal Loans: High-volume, short-cycle loans where speed and automation are essential. A good LOS can take a personal loan from application to disbursal in under 30 minutes.

Business and SME Loans: More complex underwriting involving financial statements, GST data, and business vintage. A configurable BRE and document analysis engine become critical here.

Payday and Salary Advance Loans: Ultra-short-cycle products where bureau pulls, employment verification, and bank statement analysis must happen in real time.

Gold Loans: Require integration with valuation tools and physical collateral management — typically handled via branch-based origination workflows.

Home and Mortgage Loans: Longer origination cycles with complex documentation. OCR-powered document processing and legal verification integration are key.

Microfinance Loans: High volume, low ticket size, often with group lending models. The LOS must handle field agent workflows, offline data capture, and bulk processing.

Auto Loans: Require integration with vehicle valuation APIs, RTO data, and dealer management systems.

Roopya offers pre-configured solutions for each of these loan types, allowing lenders to launch any product type quickly with product-specific workflows and credit policies already built in.

Loan Origination Software vs. Loan Management System: Understanding the Difference

These two terms are often confused, but they serve distinct functions:

| Feature | Loan Origination Software (LOS) | Loan Management System (LMS) |

|---|---|---|

| Primary Function | Creating new loans | Managing active loans |

| Key Processes | Application, underwriting, disbursal | Repayment, collections, reporting |

| Data Focus | Applicant data, risk assessment | Account data, payment schedules |

| Users | Credit officers, underwriters, KYC teams | Operations, collections, finance teams |

| Integration Need | Credit bureaus, KYC, e-sign | Payment gateways, accounting systems |

While many lenders implement these as separate systems, the most efficient operations use a unified platform that integrates both — eliminating data silos and manual handoffs between origination and servicing.

Roopya provides exactly this: a fully integrated lending platform that covers both LOS and LMS within a single ecosystem, ensuring seamless data flow from the moment a borrower applies to the final repayment.

The True Cost of Not Using a Modern LOS

Many lending institutions — especially smaller NBFCs and MFIs — continue to rely on spreadsheets, legacy core banking systems, or semi-manual processes for loan origination. The hidden costs of this approach are enormous:

Processing Costs: Manual origination can cost ₹1,500–₹4,000 per application when you factor in staff time, document handling, and error correction. An automated LOS can reduce this to ₹200–₹500 per application.

Turnaround Time: Manual processes typically take 5–10 business days to reach a credit decision. Digital origination with a modern LOS can achieve same-day or even real-time decisions.

Fraud Losses: Without AI-powered fraud detection, fraudulent applications slip through more easily. Industry data suggests that digital fraud detection can reduce lending fraud by 60–80%.

Regulatory Risk: Manual compliance tracking is inherently error-prone. A single compliance failure with RBI guidelines can result in penalties, operational restrictions, or reputational damage.

Competitive Disadvantage: As more lenders adopt digital origination, institutions that remain manual will struggle to match the speed and convenience that borrowers increasingly demand.

The ROI of implementing a modern LOS is typically achieved within 3–6 months of deployment.

How to Evaluate and Select the Best Loan Origination Software

Choosing an LOS is a strategic decision. Here is a practical framework for evaluation:

Step 1 — Define Your Requirements Map your current origination workflow in detail. Identify the bottlenecks, manual steps, and compliance gaps that the LOS must address. Define your loan products, borrower segments, and channel strategy.

Step 2 — Assess No-Code Flexibility Determine whether your team can configure and modify the system without developer involvement. This is critical for long-term agility.

Step 3 — Evaluate the API Ecosystem List every third-party integration you need — credit bureaus, KYC providers, bank statement analyzers, e-sign, payment gateways. Verify that the LOS has pre-built, tested integrations for each.

Step 4 — Review Compliance Capabilities Confirm that the platform is updated for current RBI digital lending guidelines, data localization requirements, and KYC norms.

Step 5 — Test Deployment Speed Ask for a live sandbox environment. How quickly can you configure a loan product and test a complete origination workflow?

Step 6 — Understand the Pricing Model Avoid platforms with large upfront license fees. The best LOS platforms offer a pay-as-you-use or subscription model that scales with your loan volumes.

Step 7 — Evaluate Support and Onboarding Assess the vendor’s onboarding process, training resources, and ongoing support SLAs. A fast go-live is only valuable if you have strong support when issues arise.

Step 8 — Check the Lending Analytics Layer Post-origination analytics are essential for refining your credit policy and understanding portfolio performance. A strong LOS should include or integrate with a lending analytics module.

Why Roopya Is Among the Best Loan Origination Software Platforms in India

Roopya is built specifically for the Indian lending market — for NBFCs, banks, MFIs, and modern fintech lenders who need to move fast, stay compliant, and scale efficiently. Here is what sets Roopya apart:

Go Live in 1 Day: Roopya’s streamlined onboarding and plug-and-play infrastructure mean you can start processing loans almost immediately — not in months.

Zero Upfront Cost: Roopya’s pay-as-you-use pricing model eliminates the large capital expenditure that legacy LOS platforms require. You pay for what you use.

300+ Pre-integrated APIs: From CIBIL and Equifax to Aadhaar eKYC, video KYC, e-stamp, and UPI payment gateways — everything is pre-integrated and ready to go.

Truly No-Code Platform: Launch and manage your entire lending operation without writing a single line of code. Business users can configure loan products, credit policies, and workflows through an intuitive visual interface.

20+ Pre-configured Loan Products: Roopya comes with ready-to-use loan products and customer journeys — from personal loans to SME credit, gold loans, and microfinance products.

AI-Powered Credit Decisioning: Roopya’s ML-powered credit scoring delivers 40% better accuracy than traditional scoring methods, analyzing alternative data and behavioral patterns alongside bureau scores.

Advanced Fraud Detection: AI-powered fraud modules detect suspicious patterns instantly across all applications, reducing fraud by up to 80%.

Unified Lending Platform: Roopya covers the full lending lifecycle — origination, management, collections, early warning systems, and analytics — within a single integrated platform.

Always Compliant: Roopya’s platform is continuously updated to stay ahead of RBI regulatory changes, ensuring your institution is always operating within the latest guidelines.

Trusted by Leading Modern Lenders: Roopya is trusted by a growing network of NBFCs, fintech lenders, and modern lending institutions across India.

Roopya’s Loan Origination Platform: A Closer Look

Roopya’s Loan Origination Platform covers every stage of the origination lifecycle with purpose-built modules:

Digital Application Forms: Configurable, mobile-friendly application forms that capture all necessary borrower data across any channel.

Automated Customer Loan Journey: Pre-configured end-to-end borrower journeys that guide applicants from inquiry to disbursal with minimal manual intervention.

AI-Powered Document Analysis: Advanced OCR and NLP algorithms automatically extract, verify, and validate documents with 99%+ accuracy — detecting fraud and anomalies instantly.

No-Code Business Rule Engine: Configure complex credit policies, approval workflows, and decisioning rules through an intuitive visual interface. The BRE also learns from historical data to optimize rules continuously.

Intelligent Credit Decisioning: Automated credit scoring that combines bureau data, alternative data, behavioral analytics, and custom scorecards to deliver real-time, accurate credit decisions.

Seamless KYC and Identity Verification: Full support for Aadhaar eKYC, PAN validation, VKYC, and face match — all pre-integrated and compliance-ready.

e-Sign and e-Stamp Integration: Digital loan agreement execution via legally valid e-sign and e-stamp, eliminating the need for physical documentation.

Automated Disbursal: Direct integration with payment gateways for instant, automated fund transfer upon loan approval.

Real-Time Reporting and Analytics: Built-in dashboards and custom reports providing full visibility into origination performance, approval rates, turnaround times, and credit quality.

Lending Analytics: The Intelligence Layer Above Your LOS

The best loan origination software does not just process applications — it generates intelligence that makes every future decision smarter. Roopya’s Lending Analytics module goes beyond basic reporting to provide:

Credit Risk Analytics: Deep analysis of your portfolio’s risk profile, including probability of default (PD), loss given default (LGD), and exposure at default (EAD) modeling.

Application Scorecard Development: Build and deploy custom application scorecards calibrated to your borrower segment and product mix.

Expected Credit Loss (ECL) Calculation: IFRS 9-compliant ECL calculation for provisioning and financial reporting.

Loan Pricing Analytics: Data-driven loan pricing that balances risk-adjusted returns with market competitiveness.

Credit Risk Model Validation and Stress Testing: Ongoing validation and stress testing of your credit models to ensure they remain accurate and robust under different economic scenarios.

This analytics layer transforms your LOS from a processing tool into a strategic competitive advantage.

Invest in the Right Loan Origination Software Today

The Indian lending market is growing at a pace that rewards speed, accuracy, and compliance — and punishes inefficiency. Lenders who rely on manual, fragmented origination processes will find it increasingly difficult to compete with digitally native peers who can approve and disburse loans in minutes.

The right loan origination software is not just an operational upgrade — it is a strategic investment in your institution’s future. It reduces cost per loan, accelerates turnaround, improves credit quality, strengthens fraud protection, and gives your team the data-driven insight to make better decisions every day.

Roopya has been purpose-built to give Indian lenders exactly this kind of competitive advantage. With a no-code platform, 300+ pre-integrated APIs, AI-powered decisioning, and the ability to go live in a single day, Roopya empowers NBFCs, banks, and modern lenders to build scalable, compliant, and profitable lending operations.

Ready to transform your loan origination process? Request a demo at roopya.money and discover how Roopya can help your institution go live faster, lend smarter, and grow with confidence.