Legacy Loan Management Software vs Roopya: Complete Comparison for NBFCs, Banks & MFIs

Every lending institution in India is running some form of loan management software. The critical question is not whether you have a system — it is whether your system is holding you back. Across the country, thousands of NBFCs, banks, and microfinance institutions are still operating on legacy loan management software that was built for a different era of lending. These systems were designed when branch banking was the norm, when credit decisions took days, and when regulatory technology was a spreadsheet.

The world has changed. Borrowers are digital, competition is fierce, and regulators expect transparency and real-time reporting. Legacy loan management software — with its rigid architecture, costly customisations, and slow implementation timelines — is increasingly incompatible with this reality.

Start Free Trial

This is a definitive, head-to-head comparison of legacy loan management software against Roopya — a next-generation, no-code lending infrastructure platform built specifically for the modern Indian lending market. Whether you are evaluating your first loan management system or considering migrating away from a platform that has outgrown its usefulness, this guide will give you every data point you need to make the right decision.

1. Defining the Two Sides: What Is Legacy Loan Management Software?

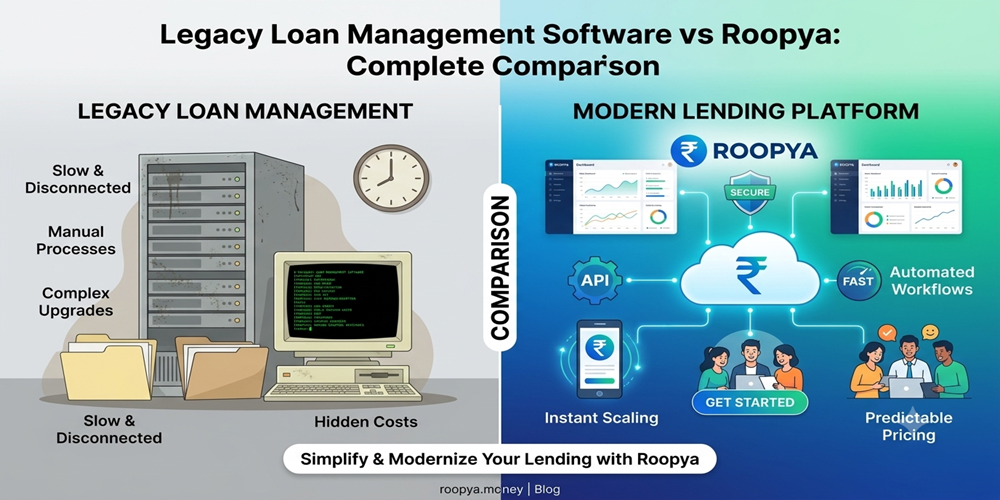

The term ‘legacy loan management software’ covers a wide range of older or traditional platforms that share certain defining characteristics. These are typically on-premise or partially hosted solutions that were developed before cloud computing, mobile-first design, and open API architectures became standard. They include both old-generation domestic platforms used by Indian NBFCs and banks, as well as older versions of global lending software localised for the Indian market.

Common examples of the legacy category include platforms built on Oracle or IBM databases, decade-old .NET or Java-based systems, systems that require dedicated IT infrastructure, and tools that depend on vendor teams for every configuration change. The defining characteristic is rigidity — these systems were not designed to change quickly, integrate broadly, or scale elastically.

Roopya, by contrast, is a modern, cloud-native, no-code lending infrastructure platform. It was built from the ground up for Indian lenders, with a specific design philosophy: any lending institution should be able to go live, configure, and scale without needing a large technical team, a long implementation project, or a significant capital investment. Roopya covers the full lending lifecycle — Loan Origination System (LOS), Loan Management System (LMS), Collections, Early Warning System, and Lending Analytics — through a single, unified platform.

2. The Core Problem with Legacy Loan Management Software

To understand why the comparison matters, it helps to look at the concrete ways legacy loan management software creates operational drag for lending institutions.

2.1 Implementation Takes Months — Sometimes Years

A typical legacy loan management software implementation for a mid-sized NBFC takes six to eighteen months. This timeline includes vendor selection, technical infrastructure procurement, data migration, customisation development, user acceptance testing, and go-live. During this period, the lender is either operating on manual processes or running parallel systems — both of which are expensive and error-prone. Every month of delayed go-live is a month of lost market opportunity.

Roopya goes live in one day. This is not marketing language — it is a structural feature of the platform. Pre-built product journeys, pre-integrated APIs, and a no-code configuration interface mean there is nothing to install, no infrastructure to provision, and no custom code to write. A lender that signs up with Roopya can begin processing live loan applications within 24 hours.

2.2 Every Change Requires IT Intervention

In legacy systems, changing a credit policy rule requires raising a ticket with the software vendor, waiting for a developer to make the change, testing the modification in a staging environment, and deploying it — a process that can take days or weeks. In a competitive lending environment where credit policy must respond to portfolio performance, market conditions, and regulatory updates, this lag is operationally debilitating.

Roopya’s no-code Business Rule Engine (BRE) allows credit and risk teams to modify decisioning rules, approval thresholds, product parameters, and workflow configurations through an intuitive visual interface — in minutes, without writing a single line of code. The same applies to application forms, customer journeys, document checklists, and reporting dashboards.

2.3 Integration is Painful and Expensive

Connecting legacy loan management software to external data sources — credit bureaus, KYC providers, payment gateways, accounting systems — typically requires custom API development. Each integration is a project: scoped, quoted, developed, tested, and maintained. A lender wanting to add a new bureau provider or a new eSign vendor is looking at weeks of development work and significant vendor fees.

Roopya ships with 300+ pre-integrated APIs. Every major credit bureau in India (CIBIL, Experian, Equifax, CRIF), all leading KYC providers (Aadhaar eKYC, PAN, Digilocker, video KYC), eSign platforms, payment gateways, GST data providers, and accounting tools are already connected. Activating a new integration is a configuration step, not a development project.

2.4 Pricing Models Front-Load the Cost

Legacy loan management software vendors typically charge significant upfront licence fees, separate implementation fees, annual maintenance fees, and per-user charges. The total cost of ownership for a mid-sized NBFC over three years can easily run into several crores — a significant financial commitment before a single loan is processed. This pricing model is particularly punishing for new or growing lenders whose volume and revenue are still being established.

Roopya uses a pay-as-you-use model with zero upfront cost. There are no licence fees, no implementation charges, and no minimum commitments. Lenders pay based on actual transaction volume, meaning the platform cost scales proportionally with the business. A lender processing 50 loans a month pays far less than one processing 5,000 — and can grow from one to the other without renegotiating contracts or upgrading licences.

2.5 Mobile and Digital Readiness Is an Afterthought

Legacy loan management systems were designed for desktop-based, branch-operated workflows. Mobile interfaces, if they exist at all, are retrofitted — clunky, limited in functionality, and poorly optimised for the borrower journeys that modern customers expect. Digital application forms, video KYC, real-time WhatsApp notifications, and instant in-app credit decisions are capabilities that legacy systems struggle to deliver without extensive customisation.

Roopya was designed mobile-first, from the borrower experience to the lender interface. Every borrower touchpoint — application, KYC, document upload, eSign, repayment — is designed for smartphone interaction. Every lender workflow — application review, credit decisioning, collections, reporting — works seamlessly on desktop and mobile. This is not a feature add-on; it is the foundational design assumption of the platform.

3. Feature-by-Feature Comparison: Legacy Loan Management Software vs Roopya

The table below provides a direct, feature-level comparison across the most important dimensions of a loan management system:

| Feature / Dimension | Legacy Loan Management Software | Roopya |

| Go-Live Timeline | 6–18 months | 1 Day |

| Deployment Model | On-premise or hybrid | Cloud-native, fully hosted |

| Implementation Cost | ₹20L–₹2Cr+ upfront | Zero upfront cost |

| Pricing Model | Licence + maintenance fees | Pay-as-you-use |

| No-Code Configuration | Not available — requires IT/vendor | Fully no-code for business users |

| API Integrations | Custom dev per integration | 300+ pre-integrated out of the box |

| Credit Bureau Integration | Manual or expensive add-on | CIBIL, Experian, CRIF, Equifax built-in |

| KYC Automation | Manual or partial | Full Aadhaar eKYC, PAN, VKYC, Digilocker |

| AI / ML Capabilities | Limited or absent | AI OCR, ML scoring, fraud detection, NLP |

| Business Rule Engine | Rigid, vendor-configured | No-code, self-learning BRE |

| Mobile-First Design | Retrofitted or unavailable | Native mobile for borrowers and lenders |

| eSign Integration | Separate vendor required | Built-in, legally valid Aadhaar eSign |

| Loan Products Supported | Limited, product-specific licences | 20+ products on one platform |

| Multi-Channel Origination | Branch or single channel | Web, mobile, DSA, API/embedded |

| Real-Time Decisioning | Rare; mostly batch processing | Instant automated decisioning |

| RBI Compliance Updates | Slow; manual updates required | Continuous, automatic updates |

| Audit Trail & Reporting | Basic; often manual exports | Automated, real-time, regulatory-ready |

| Collections Management | Separate system required | Integrated collections module |

| Early Warning System | Not available | Built-in predictive EWS |

| Scalability | Requires infrastructure upgrades | Auto-scales on cloud infrastructure |

| Customer Support | Ticket-based; slow resolution | Dedicated onboarding and support |

4. Deep Dive: Roopya’s Advantages in Each Critical Area

4.1 Speed to Market

In lending, time is money in the most literal sense. Every day a lender is not processing applications is a day of interest income foregone and market share surrendered to faster competitors. Legacy loan management software’s multi-month implementation timeline is simply incompatible with the pace of modern lending markets.

Roopya’s one-day go-live is made possible by three architectural decisions: pre-configured loan product templates that require only minor customisation; a unified, cloud-hosted infrastructure that eliminates server provisioning; and a no-code configuration layer that business users can operate independently. The result is that a newly licensed NBFC or an established lender entering a new product segment can be live and processing applications within 24 hours of signing up.

4.2 Total Cost of Ownership

When lenders calculate the true cost of legacy loan management software, the upfront licence fee is only the beginning. Implementation services, annual maintenance contracts, customisation fees for every new feature, infrastructure costs, and the internal IT headcount required to manage the system all add up. Over five years, a legacy LMS for a mid-sized NBFC can cost upwards of ₹3–5 crore — before a single business outcome is produced.

Roopya’s pay-as-you-use model fundamentally changes this equation. There is no upfront investment, no infrastructure cost, and no maintenance fee. The only cost is a per-transaction or per-loan fee that scales directly with your business volume. This means Roopya is as affordable for a 50-loan-per-month startup as it is for a 5,000-loan-per-month established lender — and the pricing grows only as the business grows.

4.3 Credit Decisioning Quality and Speed

Legacy loan management software typically handles credit decisioning through batch processing — applications are collected, and decisions are made in bulk at scheduled intervals. This introduces delays of hours or even overnight wait times between application and decision. In a world where a borrower may apply to three lenders simultaneously and accept the first offer they receive, batch processing is a structural competitive disadvantage.

Roopya’s credit decisioning is real-time and AI-powered. The moment a borrower completes their application, Roopya simultaneously triggers bureau pulls, document analysis, and BRE evaluation. A complete credit decision — based on bureau data, document-extracted income, alternative data signals, and your configured credit policy — is produced in seconds. For clean-profile borrowers, the entire journey from application submission to loan offer acceptance can be completed in under 15 minutes.

4.4 Compliance and Regulatory Agility

The RBI’s regulatory environment for digital lending is one of the most dynamic in the world. New guidelines on digital lending, KYC norms, interest rate disclosure, recovery practices, and data localisation emerge regularly. For lenders on legacy systems, each regulatory change triggers an IT project — analyse the impact, raise a change request with the vendor, wait for development, test, deploy. This process can take months, leaving lenders exposed to compliance risk in the interim.

Roopya’s platform is continuously updated to reflect the latest RBI guidelines and regulatory requirements. Compliance changes are implemented at the platform level and rolled out to all lenders simultaneously — no change requests, no development cycles, no compliance lag. Lenders on Roopya are always running on a compliant platform, without doing anything.

4.5 Data and Analytics

Legacy loan management software typically stores data in relational databases that are difficult to query for business intelligence. Generating portfolio analytics, credit performance reports, or collections efficiency dashboards requires either a separate BI tool (adding cost and complexity) or manual data exports to spreadsheets (adding time and error risk).

Roopya’s Lending Analytics module is built into the platform. Real-time dashboards show portfolio health, application funnel metrics, bureau score distributions, collection efficiency, and NPA trends — all updated live as transactions occur. The platform’s AI-driven analytics can generate natural language insights from complex data, identifying trends and anomalies automatically. Regulatory reports required by RBI can be generated and exported in the correct format with a single click.

5. Migration from Legacy Loan Management Software to Roopya

One of the most common concerns raised by lenders considering migration from a legacy system is the risk and complexity of data migration. This is a legitimate concern — poorly executed migrations can result in data loss, system downtime, and operational disruption. Roopya has addressed this concern through a structured migration approach:

- Data Assessment: Roopya’s implementation team conducts a detailed assessment of the existing system’s data structure, identifying loan records, customer profiles, repayment histories, and document archives to be migrated.

- Parallel Running: During migration, Roopya runs in parallel with the legacy system, ensuring continuity of operations. New applications are processed on Roopya while existing portfolio data is migrated in batches.

- Validation and Reconciliation: Every migrated record is validated against the source system. Discrepancies are flagged and resolved before the legacy system is decommissioned.

- Zero Downtime Cutover: The final cutover from legacy to Roopya is designed to be zero-downtime. Lenders experience no operational disruption during the transition.

- Post-Migration Support: Dedicated support is provided for the period immediately following migration to address any edge cases or user queries.

Lenders who have completed migration from legacy systems to Roopya consistently report that the process was faster and lower-risk than they expected. The structured approach, combined with Roopya’s experienced implementation team, makes migration a manageable project rather than a high-stakes gamble.

6. Who Should Switch from Legacy Loan Management Software to Roopya?

Not every legacy system user is experiencing the same pain points at the same intensity. Here is a framework for assessing whether migration to Roopya is the right move:

- You are losing deals to faster competitors. If borrowers are getting approvals from competitors before your system has even processed the application, speed is your critical constraint. Roopya’s real-time decisioning directly addresses this.

- Your IT team spends more time maintaining the LMS than building the business. Legacy systems are maintenance-heavy. If your technology resources are consumed by keeping the existing system running rather than building new capabilities, it is time to switch to a platform that runs itself.

- You are launching a new loan product and the vendor says it will take six months. Roopya’s 20+ pre-configured product journeys mean new products go live in days, not months.

- Your compliance team is constantly firefighting regulatory changes. On Roopya, compliance updates are applied automatically. Your team can focus on business, not regulatory catch-up.

- Your bureau integration or KYC costs are significant line items in your P&L. Roopya’s 300+ pre-integrated APIs eliminate the per-integration development cost entirely.

- You want to expand into digital channels but your current system is branch-centric. Roopya’s mobile-first, API-first architecture makes digital channel expansion a configuration exercise, not a development project.

7. Real-World Impact: What Lenders Experience After Switching to Roopya

The operational improvements that lenders experience after migrating from legacy loan management software to Roopya are consistent and measurable:

- 10x Faster Processing: Loan application processing time drops from hours or days to seconds. Roopya’s intelligent document processing and real-time decisioning dramatically compress the application-to-decision timeline.

- 40–60% Lower Operational Costs: The elimination of manual processing, automated KYC, and AI-powered document review directly reduce the cost per loan originated.

- 80% Reduction in Fraud: Roopya’s built-in AI fraud modules detect suspicious patterns — fake documents, identity mismatches, synthetic identity fraud — that manual processes routinely miss.

- 60% Better Collection Efficiency: The integrated collections module, with automated reminders and AI-driven collection strategies, significantly improves recovery rates compared to manual collection processes.

- 95% Borrower Satisfaction: Roopya’s conversational AI and smooth digital journey deliver borrower satisfaction scores that legacy branch-based processes cannot match.

- Zero Compliance Incidents: Automatic regulatory updates and built-in audit trails mean lenders on Roopya have a clean compliance record — no RBI observations, no audit findings related to system deficiencies.

8. Roopya’s Full Platform: Beyond Just Loan Management

One of the significant advantages of Roopya over legacy loan management software is the breadth of its platform. Many legacy systems cover only one stage of the lending lifecycle, requiring lenders to integrate multiple systems — a separate LOS, a separate LMS, a separate collections tool, and a separate analytics platform. Each integration point is a potential failure mode, a data reconciliation burden, and an additional vendor relationship to manage.

Roopya unifies the entire lending lifecycle on a single platform:

- Loan Origination System (LOS): Digital application forms, automated KYC, credit bureau integration, AI document analysis, real-time decisioning, eSign, and loan offer generation.

- Loan Management System (LMS): Portfolio management, amortisation schedules, payment processing, customer portal, prepayment and restructuring workflows.

- Collections System: Automated payment reminders via SMS, WhatsApp, and email; collection workflow management; agent management; payment plan configuration.

- Early Warning System (EWS): Predictive risk models that identify potential defaults before they occur, with behavioural analytics and proactive intervention workflows.

- Lending Analytics: Real-time portfolio dashboards, credit performance analytics, risk assessment reports, and AI-generated insights.

Having all of these on a single platform, with a single data model and a single vendor relationship, eliminates the integration burden entirely. Data flows seamlessly from origination through servicing through collections through analytics — with no reconciliation required and no data silos.

9. Making the Decision: A Framework for Lenders

If you are a lender currently evaluating legacy loan management software versus Roopya, here is a practical decision framework:

- Assess your current cost of ownership: Add up licence fees, maintenance, IT headcount, integration costs, and customisation fees over the past three years. Compare this to Roopya’s pay-as-you-use pricing at your current volume.

- Quantify your speed gap: How long does it currently take from application receipt to credit decision? How does this compare to your fastest-moving competitor? What is the cost of this gap in lost conversions?

- Identify your compliance risk exposure: When was the last time your system was updated for a regulatory change? How long did it take? What compliance risks are you currently carrying?

- Evaluate your product launch capability: If you wanted to launch a new loan product next month, could your current system support it? How long would it take and at what cost?

- Consider your growth trajectory: Where do you expect to be in three years in terms of loan volume? Will your current system scale to that volume without significant additional investment?

If the answers to these questions reveal gaps — as they do for the vast majority of lenders on legacy systems — the case for migrating to Roopya is compelling.

10. Conclusion: The Choice Is Clear

Legacy loan management software was built for a world that no longer exists. It reflects the assumptions of branch-based lending, manual underwriting, and slow regulatory cycles — assumptions that are increasingly out of step with the realities of Indian lending in 2026. The cost of staying on legacy systems is not just the licence fee; it is the market share lost to faster competitors, the compliance risk of slow regulatory updates, the operational cost of manual processes, and the strategic cost of being unable to launch new products quickly.

Roopya represents a fundamentally different approach: a cloud-native, no-code, AI-powered lending infrastructure platform that is designed to help lenders go live fast, operate efficiently, stay compliant automatically, and scale without limits. The comparison in this guide is not close — on every meaningful dimension, from speed to cost to capability to compliance, Roopya outperforms legacy loan management software.

The question is not whether to make the switch. The question is how soon you can do it. With Roopya’s one-day go-live and structured migration support, the answer might be: sooner than you think. Request a free demo today and see what modern loan management looks like.