NBFC Software and Lending Solution

Digital Lending Solution For NBFC

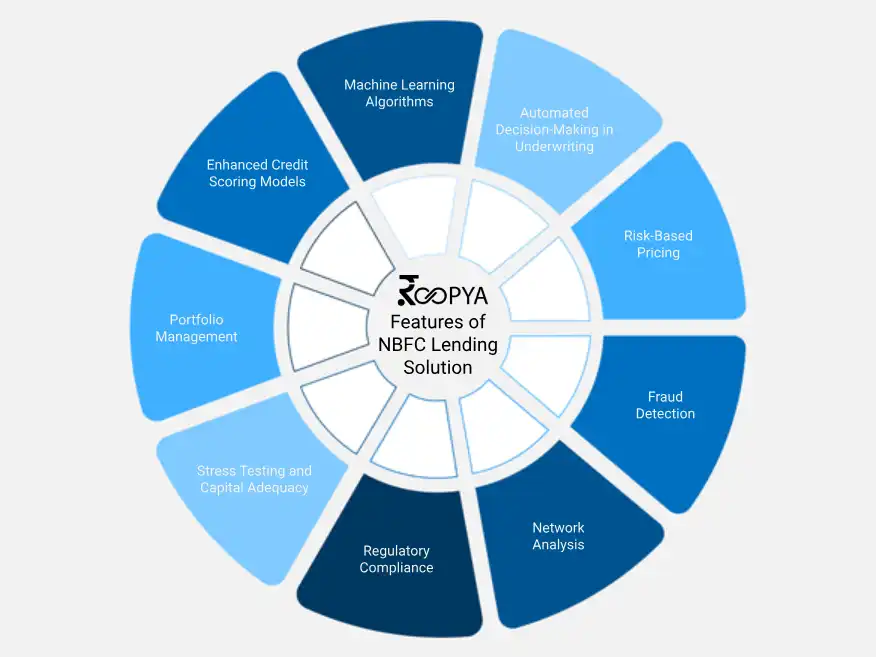

Roopya digital lending solution for a Non-Banking Financial Company (NBFC) is a software tailored to enhance the operational efficiency of NBFCs by automating and optimizing the entire loan process, from application through to disbursement. It excels in loan origination by offering an intuitive online interface where borrowers can apply for loans, upload necessary documents, and get pre-qualified in real-time, significantly reducing the loan origination cycle. The platform’s advanced underwriting capabilities stand out by employing artificial intelligence (AI) and machine learning (ML) algorithms to assess credit risk more accurately. These technologies analyse traditional financial data along with alternative data sources—such as transaction history, social media activity, and utility payments—to offer a comprehensive view of the borrower’s creditworthiness. This approach not only expands financial inclusion by catering to those with thin credit files but also minimizes default risks. Moreover, the solution ensures compliance with regulatory standards, incorporates digital wallets and payment gateways for seamless transactions, and utilizes data analytics for insightful portfolio management, thereby streamlining NBFC operations and offering a superior borrower experience.

Start Free Trial