| Primary Activity |

Financing of physical assets supporting productive/economic activity (e.g., automobiles, tractors, lathe machines). |

Dealing in investments (shares, stocks, bonds) without accepting public deposits. |

Providing finance for any activity other than its own (excluding AFCs and ICs). |

Providing credit facilities or loans to companies engaged in the development of infrastructure. |

Providing small loans to the underserved or low-income population. |

Providing finance for housing. |

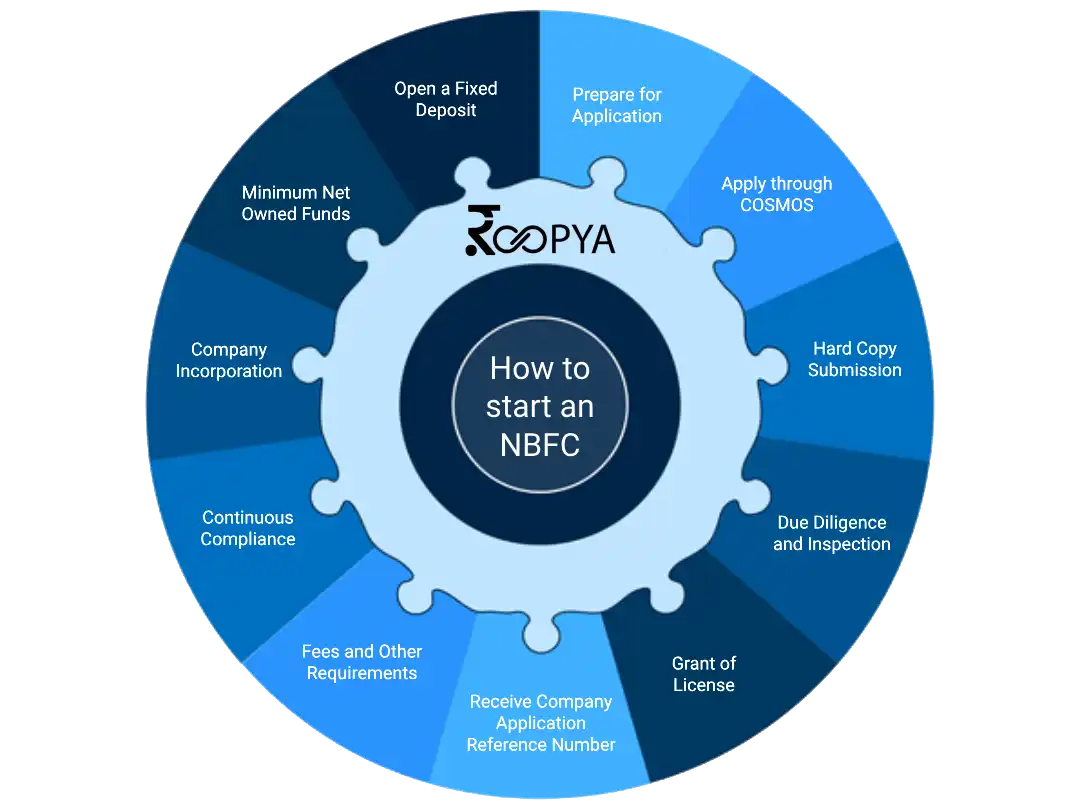

| Minimum Net Owned Funds (NOF) |

₹2 crore |

₹2 crore |

₹2 crore |

₹300 crore |

₹5 crore for MFIs wanting to qualify for NBFC-MFI status (₹2 crore otherwise). |

The National Housing Bank (NHB) specifies NOF requirements, generally ₹10 crore. |

| Regulatory Body |

Reserve Bank of India (RBI) |

Reserve Bank of India (RBI) |

Reserve Bank of India (RBI) |

Reserve Bank of India (RBI) |

Reserve Bank of India (RBI) |

Primarily regulated by the National Housing Bank (NHB), though it must also follow certain RBI guidelines. |

| Deposit Acceptance |

Cannot accept public deposits unless registered and specifically allowed by the RBI. |

Cannot accept public deposits. |

Cannot accept public deposits unless registered and specifically allowed by the RBI. |

Cannot accept public deposits. |

Cannot accept public deposits. |

Can accept public deposits subject to regulations by the NHB. |

| Liquidity Ratio Requirements |

Subject to RBI guidelines. |

Subject to RBI guidelines. |

Subject to RBI guidelines. |

Must maintain a minimum of 15% of its net demand and time liabilities in liquid assets. |

Subject to RBI guidelines, including maintaining a percentage of net assets in liquid form. |

Must adhere to liquidity ratio requirements as prescribed by the NHB. |

| Credit Rating Requirement |

Not mandatory, but beneficial for raising funds. |

Not mandatory, but beneficial for raising funds. |

Not mandatory, but beneficial for raising funds. |

Must have a minimum credit rating of ‘A’ or equivalent. |

Not mandatory, but beneficial for raising funds and regulatory compliance. |

Credit rating may be required for public deposit acceptance and is regulated by the NHB. |

| Capital Adequacy Ratio |

As prescribed by the RBI, typically around 15%. |

As prescribed by the RBI. |

As prescribed by the RBI, typically around 15%. |

Required to maintain a minimum capital adequacy ratio of 15% of its risk-weighted assets. |

Required to maintain a capital to risk-weighted assets ratio (CRAR) of 15%. |

NHB prescribes the capital adequacy requirements, usually around 12-15%. |

| Focus Sector |

Industrial, commercial, or consumer activities. |

Investment in securities and other financial assets. |

Broad, including personal loans, business loans, etc. |

Infrastructure projects like highways, power, telecom, railways, etc. |

Small-scale, unbanked, and underprivileged segments of society. |

Primarily residential housing finance, but may also include commercial housing. |

| Special Regulatory Provisions |

Must adhere to RBI guidelines specific to asset financing. |

Must adhere to RBI guidelines for investment companies. |

Subject to RBI guidelines specific to loan companies. |

Subject to higher scrutiny and specific regulations due to the strategic importance of infrastructure financing. |

Stringent regulations regarding loan recovery practices, interest rates, and operational methodology. |

Regulated by the NHB with specific guidelines on funding practices, loan disbursement, and recovery processes. |