Loan Application Software: The Complete Guide for NBFCs, Banks & Modern Lenders

The lending landscape in India is undergoing a dramatic transformation. A decade ago, applying for a loan meant weeks of paperwork, multiple branch visits, and uncertain outcomes. Today, borrowers expect instant decisions, paperless journeys, and real-time disbursements. The engine behind this revolution is loan application software — a category of technology that has quietly become the backbone of every competitive lender in the country.

Whether you are a fast-growing NBFC, a microfinance institution scaling into new geographies, or a bank looking to modernise its retail lending stack, understanding what loan application software does, how it works, and what to look for when choosing one can make the difference between market leadership and obsolescence.

Start Free Trial

This guide covers everything — from the fundamentals of how loan application software functions, to the specific features that matter most, to a detailed look at how Roopya’s platform is helping modern lenders go live in a single day and grow without limits.

1. What Is Loan Application Software?

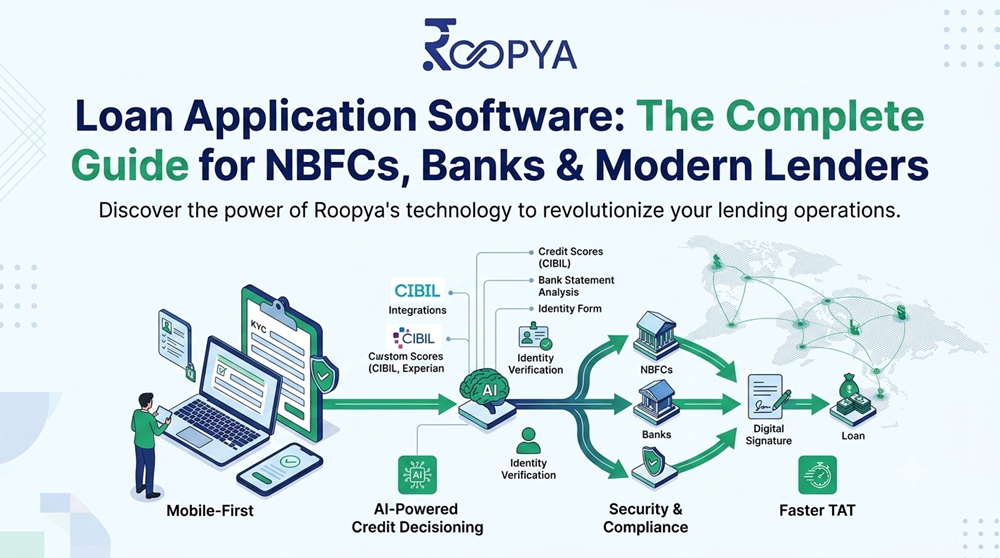

Loan application software is a digital platform that manages the end-to-end process of receiving, evaluating, and processing a borrower’s loan application. It replaces manual, paper-based workflows with automated, data-driven processes that are faster, more accurate, and dramatically cheaper to operate.

At its core, a loan application system acts as the front door of your lending business. It is where a prospective borrower first interacts with your organisation — entering personal information, uploading documents, consenting to credit bureau pulls, and receiving an initial eligibility decision. But modern loan application software goes far beyond a digital form. It orchestrates a complex web of integrations, credit checks, risk models, compliance rules, and operational workflows — all in real time and often without any human intervention.

The term is sometimes used interchangeably with Loan Origination System (LOS), though strictly speaking the loan application module is the first stage of the broader origination process. Leading platforms like Roopya unify both concepts under a single, no-code infrastructure layer.

2. Why Loan Application Software Has Become Non-Negotiable

The numbers speak for themselves. Digital lending disbursements in India crossed ₹1.5 lakh crore in FY 2024-25, and the segment is growing at over 30% annually. Borrowers — particularly in the young, mobile-first demographic — overwhelmingly prefer digital channels. A lender that still relies on manual, branch-based application processes is not merely inefficient; it is invisible to the fastest-growing segment of the credit market.

Beyond customer expectations, there are powerful operational and regulatory reasons to invest in modern loan application software:

- Speed is a competitive moat. When a borrower applies for a personal loan online, they may simultaneously apply with two or three competitors. The lender that responds first — with a personalised offer — wins the business. Automated loan application software can deliver a credit decision in seconds, not hours.

- Manual processes are error-prone and expensive. Human-led application processing introduces data entry errors, compliance gaps, and inconsistent credit decisions. A well-configured loan application platform eliminates these failure points systematically.

- RBI and regulatory compliance demands digital audit trails. Modern regulatory requirements around KYC, data localisation, and credit bureau reporting are far easier to meet with a dedicated software platform than with spreadsheets and paper files.

- Scalability without proportional cost growth. A manual process requires hiring more people as volume grows. Loan application software scales horizontally — handling ten applications or ten thousand with the same infrastructure.

3. Key Features of a World-Class Loan Application Platform

3.1 Digital Application Forms with Smart Validation

The borrower’s first interaction with your lending product is the application form. Modern loan application software offers configurable, mobile-responsive digital forms that guide applicants through the process step by step. Smart validation — checking PAN format, Aadhaar structure, IFSC codes, and pincode-level geography in real time — reduces incomplete applications and support calls dramatically. Roopya provides 20+ pre-configured loan product journeys, meaning you can launch a personal loan, business loan, or MSME credit line without building forms from scratch.

3.2 Automated KYC and Identity Verification

Know Your Customer compliance is mandatory, and manual KYC is one of the biggest bottlenecks in traditional lending. Leading loan application software integrates directly with Aadhaar eKYC, NSDL PAN verification, Digilocker, and video KYC (VKYC) providers. Borrowers can complete full KYC in under two minutes from their smartphone — without visiting a branch. Roopya’s platform comes pre-integrated with 300+ APIs including all major KYC service providers, so there is no custom development required.

3.3 Credit Bureau Integration and Automated Score Pulls

A complete loan application system automatically triggers credit bureau pulls — from CIBIL, Experian, CRIF, or Equifax — the moment an application is submitted and consent is recorded. The bureau report is parsed, scored, and fed into the credit decisioning engine without manual intervention. This not only speeds up the process but ensures every credit decision is based on the most current bureau data available.

3.4 AI-Powered Document Analysis and OCR

Borrowers upload income proof, bank statements, salary slips, GST returns, and ITR documents as part of their application. Manual document review is slow, inconsistent, and resource-intensive. AI-powered OCR and NLP within modern loan application software can extract key data fields from these documents in seconds — bank statement analysis, income computation, and anomaly detection — with accuracy levels exceeding 99%. Roopya’s intelligent document processing detects fraud signals and inconsistencies that human reviewers routinely miss.

3.5 No-Code Business Rule Engine (BRE)

Credit policy is the heart of any lending business. A Business Rule Engine (BRE) is the mechanism through which your credit policy is translated into automated decisioning. The best loan application software gives credit and risk teams the ability to configure complex, multi-variable decisioning rules — income thresholds, bureau score cutoffs, employment type filters, geographic restrictions, product-level eligibility criteria — through an intuitive visual interface, without writing a single line of code. Roopya’s no-code BRE even learns from historical data, suggesting rule improvements as your portfolio matures.

3.6 Real-Time Credit Decisioning

Once the application data is collected, documents are verified, and bureau scores are retrieved, the loan application platform synthesises all inputs through the BRE and credit scoring models to deliver an instant decision — approve, reject, or refer for manual review. Real-time decisioning is not just a convenience; it is a critical competitive advantage that directly impacts conversion rates and customer satisfaction scores.

3.7 Loan Offer Configuration and Communication

For approved applications, the software generates a personalised loan offer — including sanctioned amount, tenure, interest rate, and EMI schedule — and delivers it to the borrower via the application interface, SMS, WhatsApp, or email. Borrowers can accept digitally, triggering the next stage of the origination process automatically.

3.8 Digital Agreement Execution and eSign

Modern loan application software integrates with eSign providers to enable legally valid, paperless loan agreement execution. Borrowers sign from their device using Aadhaar OTP-based or Digilocker-based eSign. This eliminates courier costs, branch visits, and delays associated with physical documentation, while maintaining complete legal validity under the IT Act.

3.9 Multi-Channel Application Support

Borrowers come through multiple channels — direct website or app, DSA/agent networks, fintech partnerships, or embedded finance integrations. A robust loan application platform supports all these channels through a unified backend, with channel-specific application forms, pricing rules, and decisioning workflows. Roopya’s embedded finance capabilities let partner platforms originate loans directly through APIs, without redirecting the borrower to a separate lender portal.

3.10 Compliance and Regulatory Reporting

Every loan application processed must be accompanied by a comprehensive audit trail for regulatory compliance. Good loan application software automatically logs every action — who accessed the application, what data was pulled, what decision was made and why, and when each step occurred. Regulatory reports for RBI, credit bureau reporting, and CERSAI filings can be generated automatically, saving hours of compliance work each month.

4. Types of Loans That Loan Application Software Can Handle

A versatile loan application platform is not limited to a single product type. Modern software like Roopya is designed to support the full spectrum of lending products:

- Personal Loans: Salaried and self-employed, with income-based underwriting and bureau-led decisioning.

- Business and SME Loans: GST-based underwriting, banking surrogate analysis, and CIBIL MSME report integration.

- Microfinance Loans (MFI): Group lending models, JLG workflows, and rural connectivity accommodations.

- Gold Loans: Collateral valuation workflows, LTV configuration, and auction management integration.

- Home Loans and LAP: Long-tenor products with property valuation, legal check, and disbursement tranche management.

- Payday and Salary Advance Loans: Ultra-short tenors, employer verification, and high-frequency disbursement capabilities.

- Auto and Vehicle Loans: RC verification, insurance check, and hypothecation documentation workflows.

Roopya ships with 20+ pre-configured loan product journeys, letting lenders go live on any of these product types within a day.

5. Loan Application Software vs. Loan Origination System: The Difference

These terms are often confused. Loan application software specifically refers to the front-end and workflow layer that captures and processes a borrower’s application. A Loan Origination System (LOS) is a broader term covering the entire origination lifecycle — from application through underwriting, sanction, and disbursement.

In practice, most modern platforms offer both as a unified module. When you choose a loan application system from a provider like Roopya, you are getting the full LOS functionality — not just an application form, but the complete decisioning, documentation, and disbursement workflow — all in one platform.

6. How Roopya’s Loan Application Software Works

Roopya is a next-generation, no-code lending infrastructure platform built specifically for Indian NBFCs, banks, MFIs, and fintech lenders. Here is how a typical loan application journey looks on Roopya:

- Step 1 – Borrower Initiates Application: The borrower visits your branded digital interface and begins a pre-configured loan application form. Smart fields validate data in real time.

- Step 2 – Instant KYC & Bureau Check: On consent, Roopya auto-triggers Aadhaar eKYC, PAN verification, and credit bureau pulls simultaneously, with results returned in seconds.

- Step 3 – Document Upload & AI Analysis: The borrower uploads required documents. Roopya’s AI engine extracts, analyses, and verifies document data — flagging anomalies automatically.

- Step 4 – Automated Credit Decisioning: The BRE evaluates the application against your configured credit policy. A decision is generated instantly — approve, reject, or manual review.

- Step 5 – Offer Generation & eSign: An approved borrower receives a personalised loan offer and completes digital agreement signing — all within the same session.

- Step 6 – Disbursement Trigger: The completed application moves to the loan management system, triggering disbursement workflows automatically.

The entire journey — from application to sanction — can be completed in under 15 minutes for clean profiles, with zero human intervention.

7. Key Benefits of the Right Loan Application Software

Faster Time-to-Market

Traditional loan software implementations take six to twelve months. Roopya’s no-code platform lets lenders go live in a single day. Pre-built integrations, pre-configured product journeys, and a no-code setup interface eliminate the development bottleneck entirely.

Lower Operational Costs

Automated document processing, instant KYC, and AI-led credit decisioning dramatically reduce the cost per loan application. Lenders on Roopya report processing cost reductions of 40–60% compared to manual workflows.

Higher Conversion Rates

A frictionless digital application experience — fast, mobile-friendly, and instant in its feedback — converts more applicants into borrowers. Real-time decisions eliminate the anxiety of waiting, and instant loan offers capitalise on the borrower’s intent at the moment of peak motivation.

Improved Risk Management

AI-powered document analysis, bureau-led underwriting, and a configurable BRE together produce more consistent, data-driven credit decisions. Human bias and inconsistency are eliminated, and your credit policy is applied uniformly across every single application.

Regulatory Compliance by Design

Roopya’s platform is continuously updated for RBI compliance. Audit trails, digital consent management, bureau reporting, and CERSAI integration are built in — not bolted on. Your compliance burden is dramatically reduced.

Scalability Without Limits

Whether you process 100 applications a month or 100,000, Roopya’s cloud infrastructure scales automatically. There is no need to provision additional servers, hire more underwriters, or manage infrastructure — the platform handles it.

8. Choosing the Right Loan Application Software: Key Questions to Ask

- Can I go live quickly, or will implementation take months? Look for platforms with pre-built integrations and no-code configuration.

- Is the platform truly no-code, or will I need a technical team to make every change?

- How many third-party integrations are pre-built? Bureaus, KYC, eSign, and payment gateways should be available out of the box.

- Is pricing flexible? Avoid platforms with large upfront licence fees. Pay-as-you-use models align incentives with your growth.

- Is the platform RBI-compliant and regularly updated? Regulatory compliance is a moving target in India.

- Can it handle multiple loan products? A single platform managing all product types is far simpler than a patchwork of tools.

- What AI capabilities are built in? Document analysis, fraud detection, and predictive credit scoring should be native features.

9. The Future of Loan Application Software in India

The next frontier for loan application technology in India is the Account Aggregator (AA) ecosystem. AA-enabled loan applications allow borrowers to share their financial data — bank statements, investment portfolios, insurance policies — directly with lenders through a consent-based, RBI-regulated framework. This dramatically improves the quality and speed of underwriting, particularly for thin-file and new-to-credit borrowers.

Embedded finance is another major trend. As fintechs and non-financial platforms integrate lending products directly into their user journeys — buy-now-pay-later at checkout, working capital for gig workers inside a payroll app — loan application software must be deliverable via API, not just as a standalone portal. Roopya’s open API architecture is built for exactly this future.

Conversational AI — chatbot and voice-driven loan application journeys — is emerging as a powerful tool for reaching underserved, low-literacy populations in Tier 2 and Tier 3 markets. The direction is clear: loan application software will become faster, more intelligent, more embedded, and more accessible. Lenders who invest in the right platform today will be positioned to lead this next wave.

10. Why Roopya Is the Best Loan Application Software for Indian Lenders

Roopya was built from the ground up for the Indian lending market — its regulatory environment, its technology landscape, and its borrower demographics. It is not a global platform adapted for India; it is an Indian platform built with India’s complexity in mind.

- 1-Day Go-Live: Pre-built product journeys, plug-and-play integrations, and a no-code setup mean you can start processing loans in 24 hours.

- 300+ Pre-Integrated APIs: Every major bureau, KYC provider, eSign platform, payment gateway, and accounting tool is already connected.

- Truly No-Code: Business users configure credit policies, workflows, and product parameters — no developer required.

- Pay-As-You-Use Pricing: Zero upfront costs. You pay only for what you process.

- AI-Powered Throughout: From document analysis to fraud detection to credit scoring, AI is embedded at every stage.

- Full Compliance: Always updated for RBI requirements, with built-in audit trails, consent management, and regulatory reporting.

- Trusted by Modern Lenders: IndiaKaLoan, QuickFinShop, Recapita, Findoc, EazyCredit and others run their operations on Roopya.

If you are ready to move beyond manual processes and build a loan application operation that scales, Roopya offers a free demo and a no-obligation trial. Go live in a day. Grow without limits.